How to Budget a 3 Paycheck Month on One Income

melaniedj • 26 May 2020

If you're paid biweekly, you might notice that there are a few months every year where it seems like there is an extra influx of cash-flow. This happens when you have a 3 paycheck month.

No big deal, right? Just extra spending money. Well, if you are a one income family like us, that third paycheck can either be wisely stewarded to be a major blessing, or frivolously spent without thought. The latter is often the temptation we are faced with.

The temptation to reward ourselves for all our hard work as mothers and homemakers and all that we manage is real.

However, if we are to be wise keepers of our home as Proverbs 31 calls us to, then faithfully managing our finances includes thoughtfully making a decision about what to do with a third paycheck.

What is a 3 Paycheck Month?

A 3 paycheck month happens when you’re paid biweekly and receive three paychecks within the same calendar month instead of the usual two. Because biweekly pay results in 26 paychecks per year, two months each year will include an “extra” third paycheck. Budgeting a 3 paycheck month intentionally can help you build savings, pay down debt, or get ahead on future bills instead of letting that additional paycheck disappear.

Why Biweekly Pay Creates 3 Paycheck Months

What I mean by a month with an extra check refers to the fact that some months have four weeks and some months have five weeks. If you are paid bi-weekly, this means you will have two months where you have an additional paycheck.

Why a 3 Paycheck Month Feels Like “Extra” Money

If you aren't living on a monthly budget, you likely have some gaps in your finances. You can afford certain things one month, but not the next. You basically play a game of spend until there isn't more, then cool the spending until the next paycheck comes. While this can "work" for a while, you'll likely find yourself frustrated if there's no intentionality. Or, if you're a one-income family, you'll likely find that it creates financial stress.

When a 3 paycheck month comes along, it can feel like you suddenly either managed your finances much better that month, or got a little raise. However, neither is true. It is just simply one of two months per year that are 3 paycheck months.

Why It Disappears Without a Plan

Have you ever heard the maxim 'failing to plan is planning to fail?' While it sounds cheesy, it holds true. When we fail to plan things that we can, in wisdom, we can trust the Lord with the outcome. We will make mistakes. But it is often in those mistakes we learn invaluable lessons the Lord graciously teaches us.

Failing to plan a third paycheck can lead to temptations like:

- Small upgrades - being in the paycheck to paycheck living rock tumbler finally gets to you and you decide to treat yourself for surviving in it so long. The irony is you'll be back in the rock tumbler of paycheck to paycheck living the next month if you use it for upgrades instead of creating margin.

- Catch-up spending - spending more in a margin month because you felt restricted in previous months. Suddenly the thing you couldn't afford before is within reach. This can look like bigger grocery trips with more extras, more eating out than usual, or letting budget categories grow because it "feels safe."

- Lifestyle creep - an extra paycheck month can make you feel like you suddenly got a raise, so you raise your expenses to match.

Here's how to create a simple plan for your third paycheck.

How to Budget a 3 Paycheck Month (Simple Plan)

First things first, it's important to actually budget your extra paycheck. Productive Christian households carefully plan for the future.

As a homemaker, I’ve learned that a lot of peace comes from preparing ahead of time. Just like meal planning or laying out books for homeschool the night before — it’s not flashy, but it changes the whole feel of the day.

Practically, when thinking about how to budget a 3 paycheck month, we want to consider a few things before making a decision (with our husbands) on what would be the most fruitful for our family.

1. Cover Regular Bills First

Before you decide what to do with the third paycheck, look at your first two paychecks for the month.

Have your normal monthly expenses already been assigned?

- Mortgage or rent

- Utilities

- Groceries

- Insurance

- Subscriptions

- Childcare

- Minimum debt payments

If those are already covered by your usual two paychecks, then your third paycheck is not needed for survival.

It can be tempting to treat a third paycheck like bonus money without first checking the foundation. Make sure the basics are covered first.

2. Choose One Wise Priority

What would make the most difference right now? Don't try to do a million different things with a third paycheck.

Scattered money rarely creates progress.

Assign your third paycheck to a clear purpose based on your priorities. This might include:

- Build your emergency fund

- Pay down debt

- Fund sinking funds

- Get ahead on next month’s bills

Small, focused progress is key.

3. Assign Every Dollar

Even though it feels like “extra,” it still needs a job.

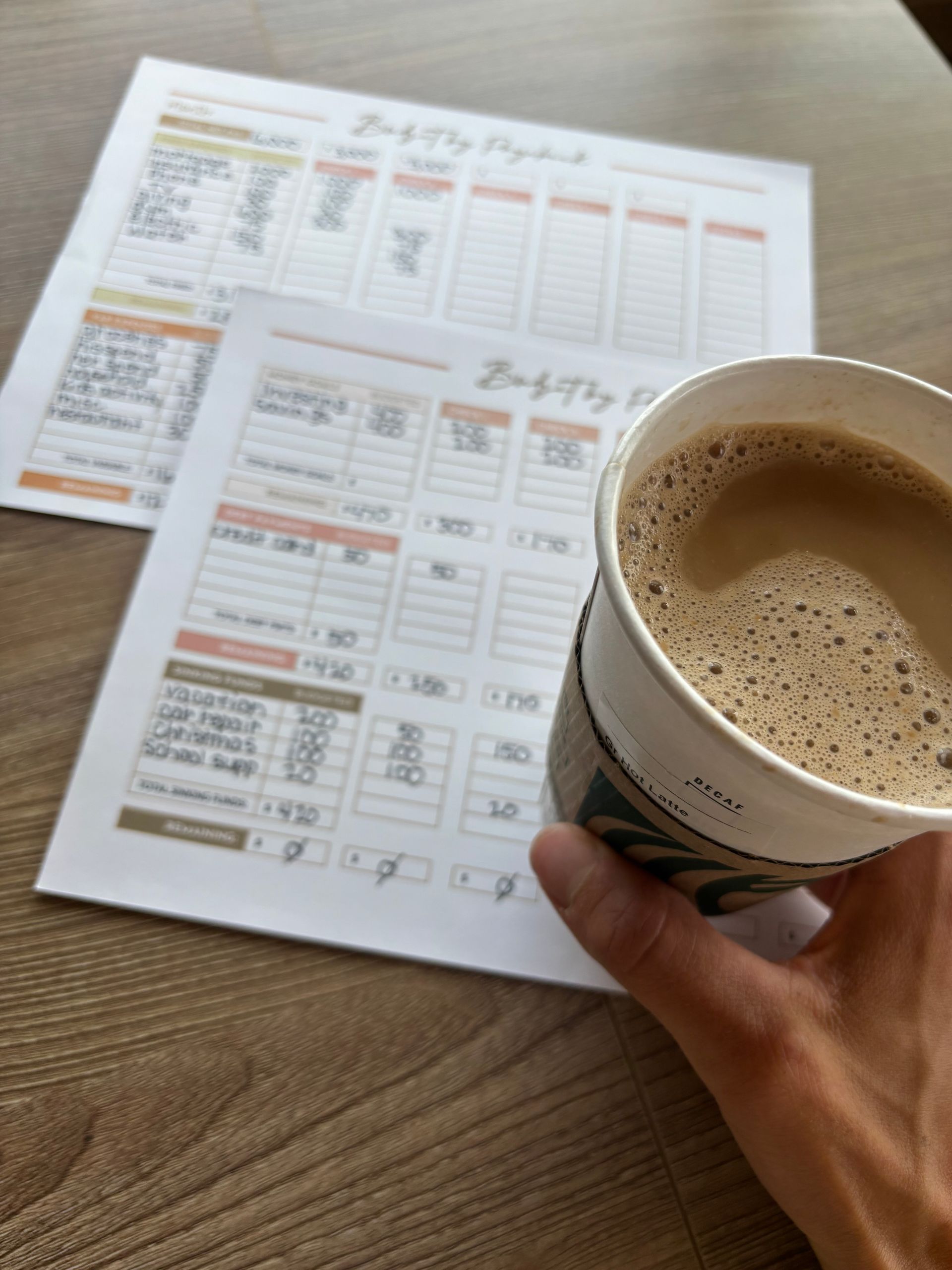

Write it down. Use my free paycheck budget template to help you assign your income to your expenses.

If $1,500 is going toward savings and $1,000 toward debt, be specific.

When we don’t assign our money, it quietly slips away in small decisions — extra grocery runs, small conveniences, little upgrades that don’t feel significant in the moment.

But when every dollar has direction, we protect the margin God has provided.

4. Think Long-Term Stability, not Short-Term Relief

A third paycheck month can feel exciting.

But for a one-income home, stability is more valuable than excitement.

Using that paycheck to strengthen your foundation — instead of increasing your lifestyle — creates something much better than a temporary boost!

What to Do With a Third Paycheck on One Income

During an extra paycheck month, start with your priorities. We always want our spending and managing of our financial resources, entrusted to us by the Lord, to reflect our priorities.

This doesn't mean we don't enjoy our money. The Lord gives us good gifts to enjoy. Rather, we must consider how we can be most faithful.

Each family must decide, prayerfully, what that looks like, but here you'll find some ideas.

1. Get Ahead on Bills

Getting a month ahead on your bills simply means using last month's income to pay this month's expenses. This creates a healthy cash flow. You can pay an expense knowing there is money in the account to cover it, because you have specifically assigned those dollars from the prior month to that expense.

In order to do this, simply calculate what your monthly obligations are (you don't need to include expenses that are NOT obligations like investing). After you've done your calculation, take that portion of your check and put it into your checking account as a buffer.

This way, you constantly have a one month of expenses buffer in your checking account!

Alternatively, you could keep this designated amount in your savings account if having it in your checking account tempts you to spend it.

2. Boost Sinking Funds

A sinking fund is a strategic way to save for an expense or multiple expenses over time by setting aside money every month.

The goal of sinking funds is to have the cash to pay for larger, seasonal/irregular expenses instead of finding yourself overwhelmed when they hit because you didn't plan for them.

Before spending your extra cash, consider boosting your sinking funds! I know it's tempting to spend it on something you've been wanting for a while, but remember your priorities.

Is it important to you that your family takes a vacation every year and spends quality time together? Put some of your paycheck (after you've covered necessities) towards your vacation fund.

Some

common sinking funds include:

- Car repairs

- Christmas

- Vacation

- School expenses

- Annual insurance dues

- Gifts (birthdays, anniversaries, weddings, baby showers, etc)

A good way to keep track of your sinking funds and their balances is to use a worksheet every month. This way, if you keep the money you have earmarked for certain sinking funds in your checking account (or all sinking funds in a savings account), you can easily track the balances and reconcile to your checking or savings.

3. Fully Fund Emergency Fund

An emergency fund is simply your savings set aside for unexpected, large expenses. Wisdom says that it's not if a financial need will arise unexpectedly, but rather when. Therefore, we would be wise to plan for it, as Proverbs exhorts us:

“The prudent sees danger and hides himself, but the simple go on and suffer for it.” — Proverbs 22:3

Without savings, every unexpected expense pushes you backward.

It can lead to credit cards, shifting bills around, and that constant thought of “What are we going to do?”

When you have an emergency fund in place, large, unexpected cash outlays become an inconvenience rather than a financial crisis.

Sinking Fund vs. Emergency Fund Expenses

Because emergency fund and

sinking fund expenses can get muddled, it necessitates a discussion about the differences between the two.

Both are funds set aside for unexpected expenses.

To differentiate, a sinking fund is money you save ahead of time for expenses you know are coming — even if they don’t happen every month. An emergency fund is money you set aside for expenses you cannot reasonably plan the timing for — it's your safety net.

For example, I would classify car maintenance and repairs as a sinking fund expense. Although you don't need maintenance or repairs every month, you know that it's likely at some point during the year your vehicle will require it. A major vehicle repair (let's say thousands of dollars worth of repairs), would likely classify as an emergency fund expense.

4. Pay Off Debt

If you have consumer debt, consider putting using this extra paycheck month as an opportunity to increase momentum towards your debt snowball.

In short, the debt snowball method is a way to pay off debt by focusing on your smallest balance first, regardless of interest rate. You make minimum payments on all debts but put any extra money toward the smallest one until it’s paid off, then roll that payment into the next smallest debt. As each debt disappears, your payment “snowballs” into larger amounts, helping you gain momentum and motivation.

You continue this process until all your debt is paid off- hence the term debt snowball!

We paid off over $20k of student loan debt in 12 months while living on one-income. This is one decision I will never regret. It made it that much easier to have me come home full-time with the kids, leaving my well-paying job as a CPA.

5. Increase Investing

One income families should strive to make investing a top priority. Don't be discouraged or lose heart if you can't set aside much right now. Finances are seasonal. You may be in a growing season or a shrinking season.

Often, when a young family has all littles and mom is at home it's a shrinking season. That's OK. Because you're not hitting all the goals Dave Ramsey says you should be doesn't mean you're failing.

Act wisely and trust the Lord for His provision!

Simply set aside what you can every month, and consider using your extra paycheck as a little boost, especially if you aren't regularly contributing to an investment account.

What if You're Living Paycheck to Paycheck

The paycheck to paycheck living cycle is exhausting.

It leaves you wondering in the back of your mind if you'll be able to afford the lunch date your friend suggested, because you know in the back of your mind you need the money to go elsewhere. So you feel guilty.

Living this way increases the decisions we have to make on a daily basis, which in turn increases our stress levels. Like a domino effect, the increased stress can cause us to make poor decisions, or give up altogether.

How a 3 Paycheck Month Can Help You Break the Cycle

If you're living paycheck to paycheck, choose one of these options to budget your third paycheck:

- Create your first $1,000 buffer

- Catch up on overdue bills

- Cover next month’s largest expense early

You'll be so glad you did this when the next month comes around and you have more breathing room, even if just a little.

Common Mistakes in a 3 Paycheck Month

Without a clear plan, a 3 paycheck month can slip through your hands quickly. We want to be intentional about the use of the paycheck, not haphazard. Here are some common mistakes that are easy to make with a third paycheck.

Treating It Like Bonus Income

A third paycheck is not a bonus, but it can feel like it. It is part of your yearly income, and we are wise to manage it as such!

Spreading It Too Thin

It’s tempting to divide that third paycheck into five different goals:

- A little to savings

- A little to debt

- A little to home projects

- A little to fun

- A little to catch up

But scattered money rarely creates noticeable progress.

When everything gets a little, nothing really changes.

Choosing one focused priority creates momentum you can feel.

Increasing Lifestyle Expenses

If a 3 paycheck month increases your monthly lifestyle instead of strengthening your foundation, next month may feel just as tight as before. It can feel like you suddenly got a raise, but this is just one month of two that there will be an extra paycheck!

Catch-up Spending

After feeling restricted for a while, it can be tempting to think you can finally let loose and actually enjoy some of your money. But if you don't have clear plan for the paycheck or if you don't operate on a monthly budget, the next month will be just as hard.

Not Deciding Before it Arrives

If you wait until the third paycheck hits the bank account to decide where it's going to go, emotions can take over quickly. Simply making a decision about what you're going to do with the money before it arrives makes it much more likely you'll stick to your plan, not letting emotional impulse spending take over.

Frequently Asked Questions About a 3 Paycheck Month

How often does a 3 paycheck month happen?

If you're paid biweekly, you receive 26 paychecks per year. Because there are only 12 months in a year, two of those months will include three paychecks instead of two.

Is a third paycheck really extra money?

Technically, no. A third paycheck doesn’t mean you earned extra income — it simply means your 26 biweekly paychecks lined up differently with the calendar that month.

But practically speaking, it can feel like extra money if your regular monthly bills are already covered by your first two paychecks.

That’s why many families choose to use a third paycheck to strengthen their financial foundation — by building savings, paying down debt, or getting ahead on upcoming expenses.

Should I split my mortgage across three paychecks?

In most cases, no.

Your regular monthly bills — including your mortgage — should still be assigned to the first two paychecks of the month, just like usual.

The goal of a 3 paycheck month is not to spread your normal bills across all three paychecks. Instead, it’s an opportunity to use that third paycheck for progress.

What if I already spent my third paycheck?

If you already spent your third paycheck, figure out when your next three paycheck month will be. Make a plan for how you'll spend it. If you're not already on a monthly budget, start there.

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.