How to Budget by Paycheck (Step-by-Step Paycheck Budget Method for One-Income Families)

melaniedj • 24 February 2026

You have a monthly budget, but it isn’t working the way you hoped. You’re still feeling stretched between paydays and trying to make a calendar-based plan fit the way your income actually comes in.

That was me before I started budgeting by paycheck.

I had a monthly budget. I tracked it carefully. I thought I was being responsible.

But every time our weekly paycheck hit, I found myself asking, “Wait… what is this supposed to cover?”

The monthly plan looked fine on paper. It just didn’t match the rhythm of our paychecks.

And that mismatch created stress- especially for a family living on one-income.

That’s when I started using a paycheck budget - a simple, repeatable system that breaks our monthly budget down even further into smaller, more manageable steps.

Instead of spending countless hours trying to reconcile a monthly budget at the end of every month, I broke every budget line from our monthly budget down into paychecks. I gave every single paycheck a job before we spent it.

This simple shift completely changed how we handled money.

Managing our finances whilst keeping a home became achievable -- not a daunting task I dreaded every month because I knew we'd be over budget and I'd end up feeling overwhelmed and discouraged.

In this guide, I’m going to show you exactly how to budget by paycheck step-by-step, so you can stop feeling stressed between paydays and learn how to use a simple, repeatable system in a way that’s manageable alongside your home, your kids, and all else you carry as a wife, mother, and homemaker.

Let's get right to it!

What is a Paycheck Budget?

A paycheck budget is a method of budgeting where you plan your spending based on each

individual paycheck instead of creating one monthly budget. Essentially, you are taking your monthly budget one step further by breaking it down into individual pay periods.

This approach works especially well for one-income families or anyone living paycheck to paycheck because it aligns bills and expenses directly with pay dates.

By assigning every dollar from each paycheck a specific job before you spend it, you control cash flow between paydays.

How to Budget by Paycheck in 5 Steps:

- Download a budget template

- Create a monthly budget

- List all pay dates

- Write down bills by due date

- Assign bills/expenses to each paycheck

- Budget variable spending

- Plan savings first

Budgeting by paycheck means you take your monthly budget and split it into smaller budgets based on your paydays. The monthly budget is your overall outline, and each paycheck budget is the action plan for that specific paycheck.

By doing this, you can better organize what bills are budgeted at what point during the month and with what paycheck.

Why Monthly Budgets Don’t Work on One Income

If you have ever tried to put together a monthly budget for your family and found yourself frustrated because you never seem to be able to plan well enough and accurately predict for what life throws your way, it's not because budgets never work. Rather, your frustration lies in the fact that you're using the wrong system.

A monthly budget works great until you consider:

- Irregular bills

- Paycheck timing (most U.S. employees are not paid once per month)

- Cash flow gaps

Take this scenario:

Say your family brings home $5,000 per month. Your mortgage is $2,000 and groceries average around $1,000.

On paper, that works.

But now let’s look at the rhythm of it.

If you’re paid biweekly, you’re bringing home $2,500 at a time.

If the mortgage is due on the 1st and you pay that full $2,000 from one paycheck, that leaves you with $500 to stretch until the next payday.

Out of that $500, you still need groceries, gas, and anything else that comes up.

Suddenly, even though your monthly numbers technically work, the cash flow feels tight.

That’s the part a monthly budget doesn’t show you.

This is where the paycheck budget alleviates the stress of managing cash-flow throughout the month. Here's a quick comparison of the two budgeting methods:

| Category | Paycheck Budget | Monthly Budget |

|---|---|---|

| Best for | All pay schedules other than once per month and one-income families or families living paycheck to paycheck | Once per month pay schedule |

| Cash flow | High - aligns with paydays | Moderate - may be gaps |

| Flexibility | More flexible | Less flexible |

| Planning method | Each paycheck separately | Budget entire month at once |

As a mom managing the day-to-day flow of the household, the paycheck budget method has brought more peace and clarity to our finances.

Instead of hoping a monthly plan stretches far enough, you’re working with money that’s actually in your account and assigning it with intention. That reduces mid-month stress, eliminates constant mental math, and makes it easier to manage your finances alongside your home.

How to Budget by Paycheck (Step-by-step)

1. Get a budget template

Before we divide everything by paycheck, we need a clear picture of the month as a whole. Think of this step as gathering the pieces for our puzzle. Think of this as clearing off the kitchen counter before you start cooking. Everything works better when you have a clear space.

If it feels overwhelming to start from scratch, I have a simple free monthly budget template PDF download that walks you through this exact first step (or sign up for the Google Sheets version below).

2. Make your monthly budget

Grab your budget template or a blank sheet of paper and list:

- Your total expected income for the month

- All fixed bills (rent/mortgage, utilities, insurance, subscriptions)

- Your variable categories (groceries, gas, household, kids)

- Any debt payments

- Any savings goals

- Budget every dollar down to zero (called a zero-based budget)

Before you assign each paycheck to a budget expense or goal, every dollar of expected income for the month needs to be given a purpose. This is your broad monthly budget. Don't leave any money remaining! Each dollar of income needs a job.

- More budgeting resources:

3. Split budget into paychecks

Now that you can see the whole month clearly, we’re going to gently break it down into smaller, manageable pieces.

Look at your pay dates for the month.

If you’re paid:

- Biweekly → you’ll likely have two paychecks (sometimes three)

- Twice a month → two set pay dates

- Weekly → four (sometimes five)

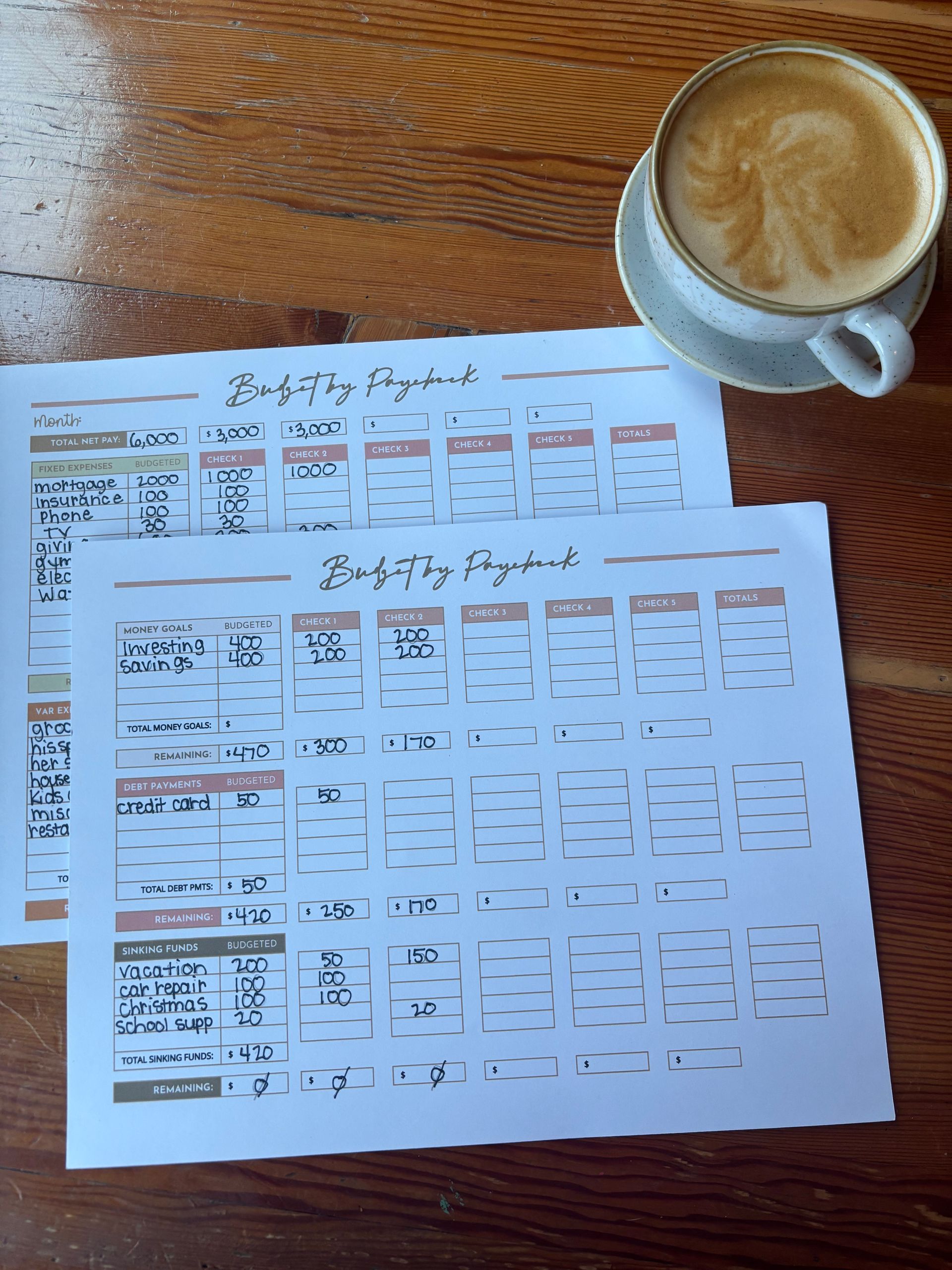

Write the dates across the top of your page. Here's an example using my one of my templates:

Under each paycheck date, draw a simple line down the page. Each section will represent what that paycheck needs to cover.

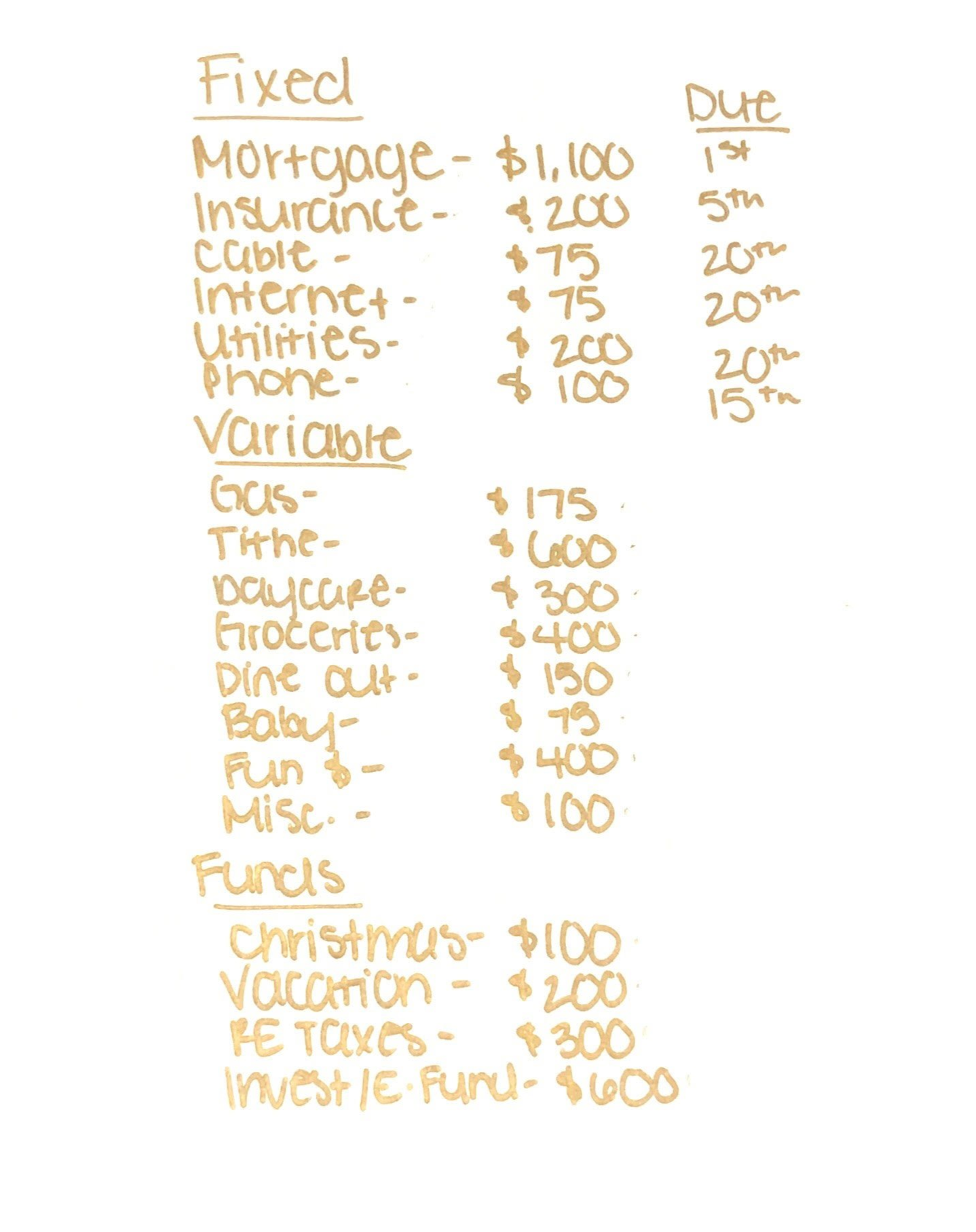

4. Write/List all Bills & Due Dates

List all your monthly expenses on the left side of the page. This includes both fixed and variable monthly expenses as well as any amounts being sent to savings, investing, or other sinking funds (vacation, new car, medical, etc).

Write the due dates next to any bills.

5. Assign Bills/Expenses to Paychecks

Now go back to your list of bills and look at the due dates.

Ask yourself:

“What bills are due before the next paycheck comes?”

Those bills get assigned to one or multiple paychecks. Divide any bills that can't come out of one paycheck by two or three, and start arranging your budget.

Instead of hoping money stretches across the month, you’re giving each paycheck a clear responsibility. When each paycheck knows its job, you don’t have to keep re-deciding what the money is for.

A Simple Example

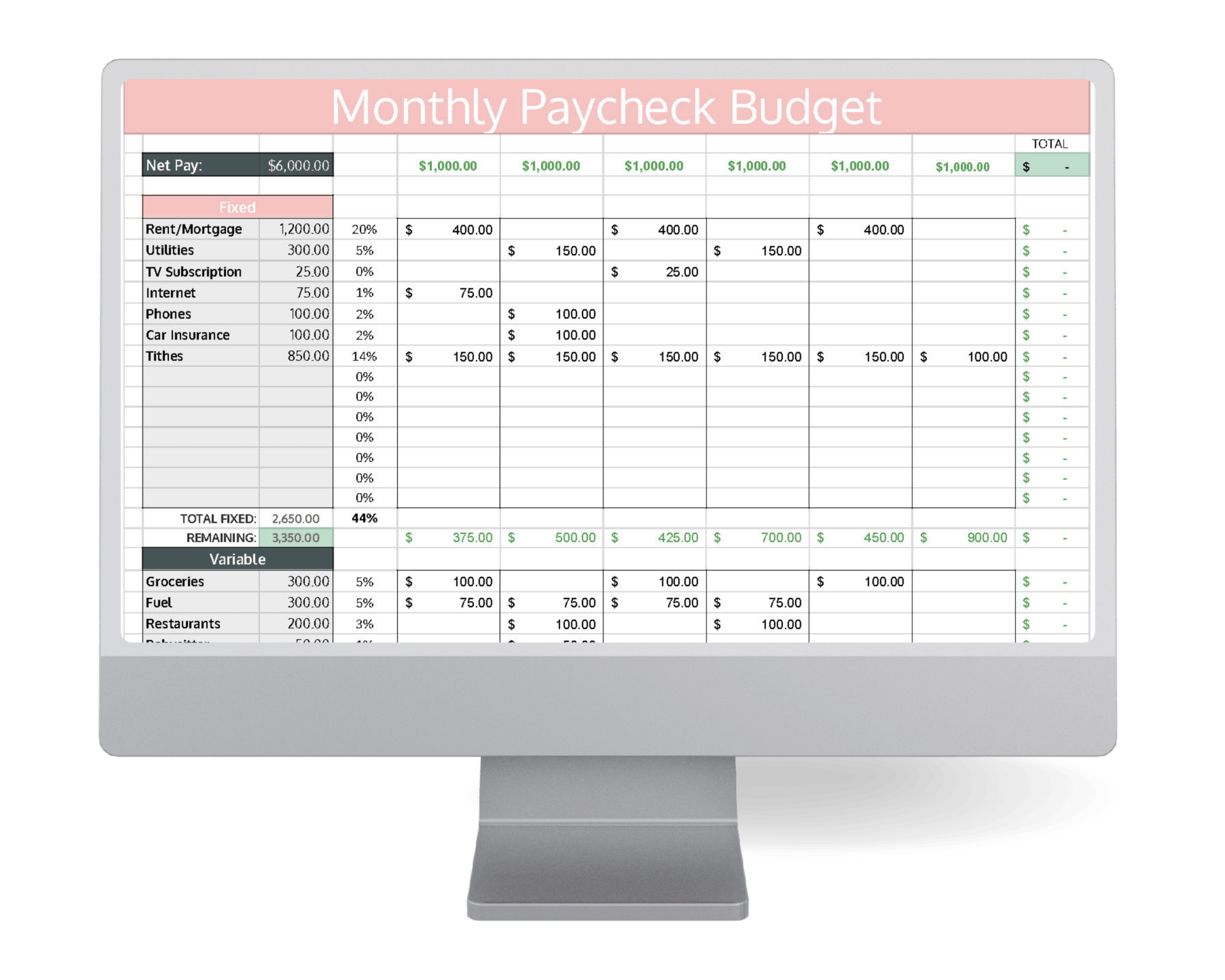

Let’s say you bring home $1,000 per weekly paycheck.

For the first paycheck of the month, you might assign:

- Mortgage: $400

- Utilities: $75

- Giving: $150

- Groceries: $100

- Gas: $75

- Minimum debt payment: $200

- Small savings transfer: $100

- Household/misc: $200

Find a schedule that works for you and the situation you are in.

6. Budget Variable Spending

Variable expenses are where a lot of moms get stuck.

You might be wondering, “How am I supposed to budget for something that changes every month? Groceries aren’t the same. Gas isn’t the same.”

And that’s true — they do fluctuate.

But even though the exact number changes, you still need a clear limit.

Instead of trying to guess the perfect amount each month, choose a realistic number your family can work within. That becomes your monthly target.

It doesn’t have to be perfect. It just needs to be intentional.

That’s the number you’ll plug into your budget and divide between paychecks.

Now that paycheck has a purpose. When it hits your account, you already know where it’s going. No guessing.

No reacting. Just following the plan you already made.

Reminder

If writing this out for the first time feels daunting, that's ok. This is a new rhythm that doesn't have to be perfect.

And if you’d like a printable version that walks you through dividing your month into pay periods step by step, you can get my free printable budget templates, which includes a layout in the exact format I use at home.

You can follow it word-for-word or simply use it as a guide while creating your own system.

7. Plan Savings First

When piecing your budget together, prioritizing expenses is key.

As we made our family budget, we first budgeted for expenses that were priorities. Expenses like bills, groceries, giving, and saving came first. Everything else (entertainment, eating out, personal spending, vacations) was split between what was leftover AFTER accounting for the priorities.

This requires a trade-off. You may not be able to spend as much on eating out as you would like or hope after budgeting for your savings goals. You and your spouse have to decide what is most important for your family.

How to Budget Biweekly

Biweekly pay doesn’t line up neatly with monthly bills. Most bills are due on the same date each month, but your paychecks shift slightly every month.

Without a plan, that mismatch creates stress.

The good news is this: budgeting biweekly is actually one of the simplest ways to create consistency on one income — once you understand the rhythm.

Twice per year, biweekly pay creates a 3 paycheck month. If you’re wondering how to handle that extra paycheck, I walk through it here.

What Does Biweekly Pay Actually Mean?

When you’re paid every two weeks, you receive 26 paychecks per year. Most months you'll receive two paychecks, but twice a year you'll receive three.

The issue is that your bills are centered around a monthly cycle, which means your income and your expenses are operating on two different cycles.

Without a plan, it can feel like some months are stretched and others are easy — even though your income hasn’t changed at all.

The paycheck budget method fixes this by organizing your money around pay dates instead of calendar months.

What About a Three-Paycheck Month?

Twice a year, you’ll receive three paychecks in one month. Instead of treating that third paycheck as bonus spending money, think of it as margin.

You can use it to:

- Build your emergency fund

- Fund sinking funds

- Pay down debt

- Get ahead on next month’s bills

Those third paychecks are create breathing room.

For more ideas and a detailed explanation of how to handle three-paycheck months, read this post.

Biweekly Pay Example

For example:

If you budget $800 per month for groceries and you’re paid twice per month, you might assign $400 to each paycheck.

If you’re paid biweekly and some months have three paychecks, you can choose to:

- Keep groceries consistent

- Or use the third paycheck to get ahead

There isn’t one perfect way-the goal is consistency.

When each paycheck carries its portion of groceries, gas, and household needs, you remove the constant question of:

“Do we have enough left?”

What if You're Living Paycheck to Paycheck?

You can be doing everything “right” — cooking from scratch, skipping extras, stretching groceries — and still feel behind if there’s no system guiding the flow of each paycheck.

Living paycheck to paycheck isn’t sustainable because it keeps you reacting instead of planning. As a mom, when I'm reacting instead of being pro-active, I feel overwhelmed, stressed, and the constant decision-making fatigue can put me into a downward spiral of emotions that do not bear the fruit of the spirit.

Just like with parenting, when we reduce the number of reactive decisions we have to make, everything feels calmer. We may not have reached all of our financial goals yet, but we can still be steadfast.

Break the Paycheck Cycle

There isn't a fancy way to break the paycheck to paycheck cycle. Sure, there are things you can do to speed up the process (make extra money, cut expenses), but sometimes either option isn't possible.

Contrary to Dave Ramsey's advice, I wouldn't recommend a stay-at-home mom go out and get a job to help play catch-up on bills. That responsibility should primarily (and ideally) fall on the husband.

Don't send your kids to daycare so you can stop living paycheck to paycheck. Seek the Lord in prayer, and be faithful in your financial decision-making. Here's where to start:

- Start with essentials and make a bare bones budget

- Build a small buffer

Step 1: Start simple. With your next paycheck, assign money to the essentials: housing. utilities, groceries, rent/mortgage, minimum debt payments, etc.

Step 2: Create a tiny buffer. If there is anything left-- even $25 -- assign it to your "buffer" category. Your goal is to quickly build this category to create breathing room and break the paycheck to paycheck living cycle.

That's it. Don't try to overhaul everything at once. When money is tight and everything feels overwhelming, clarity beats complexity.

Common Paycheck Budget Mistakes (And How to Avoid Them)

When I first started budgeting by paycheck, I thought once I understood the method, everything would just click. It didn’t.

Not because the system didn’t work — but because I was still learning how to use it well.

Here are a few common mistakes I see (and have personally made).

- Forgetting sinking funds - Expenses that don't show up every month are easy to leave out. Budget for the irregular expenses that come up like school supplies/clothes, oil changes, Christmas, birthdays, special events, etc. Read this post for a more in-depth explanation of setting up sinking funds. Just setting aside a small amount out of every paycheck for these expenses can make them seem manageable instead of overwhelmed.

- Ignoring irregular/annual expenses - Expenses that don't show up every month are easy to leave out. Budget for irregular and annual expenses that come up like school supplies/clothes, oil changes, Christmas, birthdays, special events, etc. The key to is to budget for these expenses monthly. Read an in-depth tutorial on how I do that here.

- Neglecting to budget for variable expenses - avoid the temptation to budget for the fixed expenses/bills and leave the rest out. If you don't tell those dollars where to go, your income will quietly disappear and you'll be frustrated that the budget isn't working.

- Not adjusting when life happens - remember your budget is a guide, not a contract. Life happening doesn't mean your plan isn't working. It just means you need to adjust, tweak, and move forward. Don't use life happening as an excuse to de-rail the budget completely and abandon ship.

- Expecting immediate perfection - the first month or two might feel clunky. Don't give up! You might overspend in one area and have to adjust. It will take time.

- Treating extra paycheck month money as "extra" - months that have an extra paycheck can and should be used to build stability, not spent frivolously and treated like a bonus. Give the extra paycheck a clear purpose -- emergency funds, sinking funds, or building a buffer.

- Not tracking - personally, I like to log our expenses every other day. This way, I know exactly how much we've spent so far on each budget category, and how much I have left to spend. I use the EveryDollar premium budgeting app for easy tracking.

Frequently Asked Questions

Is the paycheck budget method better than a monthly budget?

Budgeting by paycheck works better than a traditional monthly budget for many one-income families because it aligns expenses directly with pay dates. Instead of planning your spending around the first of the month, you assign bills and categories to each individual paycheck. This prevents cash flow gaps and reduces the stress of wondering whether there will be enough money left before the next payday. While monthly budgets work well for stable, salaried income, the paycheck budget method offers more flexibility and control for families managing tighter margins.

Can I use this if I'm paid weekly?

Yes, the paycheck budget method works especially well for biweekly income. When you’re paid every two weeks, your pay dates often don’t line up evenly with monthly bills. Budgeting each paycheck separately allows you to assign bills based on due dates instead of trying to stretch money across the entire month. Many families find this method eliminates overdrafts and makes it easier to plan for months that include three paychecks.

How do I budget by paycheck if I'm living paycheck to paycheck?

If you’re living paycheck to paycheck, start by covering only essential categories with each paycheck: housing, utilities, food, transportation, and minimum debt payments. Once those are assigned, any remaining amount can go toward building a small buffer fund. Even setting aside $50–$100 per paycheck creates breathing room over time. The paycheck budget method helps you see exactly where your money is going, which is often the first step toward breaking the cycle of living paycheck to paycheck.

What if I have irregular income?

If your income is irregular, you can still use the paycheck budget method by creating a “bare minimum” budget. Start by listing your essential expenses and covering those first with each paycheck. When income is higher, assign extra money toward savings, sinking funds, or future bills. This flexible approach makes paycheck budgeting ideal for commission-based jobs, self-employment, or variable schedules because you’re planning based on money actually received — not projected income.

How do I handle sinking funds?

Sinking funds are planned savings categories for future expenses, such as car repairs, holidays, or annual insurance premiums. With a paycheck budget, you assign a small amount from each paycheck into these categories instead of waiting for the expense to arrive. This prevents large, unexpected financial stress and keeps you from relying on credit cards. Including sinking funds in your paycheck budget helps create stability, even on one income.

How do I budget if I'm self-employed?

Describe the item or answer the question so that site visitors who are interested get more information. You can emphasize this text with bullets, italics or bold, and add links.Does paycheck budgeting actually help you save money?

Yes, budgeting by paycheck can help you save money because it reduces overspending between paydays and creates intentional planning. When you give each paycheck a clear purpose, you avoid the “extra money” mindset that often leads to impulse spending. Many families find they naturally increase savings once they see their cash flow clearly organized around pay dates.

ON A FINAL NOTE

Budgeting by paycheck is the perfect budgeting method for anyone who is not paid once a month.

This method works especially well for those who are self-employed or have irregular income.

This method allows you to look big picture at your finances with a monthly budget, while also staying organized and consistent day to day!

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!