The Payday Reset: How to Budget Two Paychecks Without the Overwhelm

Melanie DeJong • 9 April 2026

If you’re paid biweekly, a traditional monthly budget can feel frustrating. It gives you a helpful big-picture view of your finances, but it doesn’t always line up with how your money actually comes in. Because you’re not paid just once a month, a monthly budget can fall short when it comes to the day-to-day logistics of paying bills and managing cash flow.

The

paycheck budgeting method is a simple, repeatable budget rhythm that changed everything for our family finances.

This method is very simple, but effective. You can use this system every single month to ensure you’re staying on track financially as a family.

By allocating your income out before the month begins, you remove a decision when payday comes. The less decisions we make, and the more habits we train, the less stress we feel!

How to Budget Two Paychecks a Month: Step-by-Step

You don’t need the latest budgeting spreadsheet with a fancy dashboard that has all different kinds of formulas giving you all kinds of information. This will just overcomplicate things and cause you to over-analyze.

It’s very simple: your total income less your total expenses every month should be positive. Ideally, it will equal zero– meaning you’ve planned every single dollar of income before the month has begun.

It doesn’t take financial expertise to run a household budget. It just takes a willing mind and committed spirit.

Step 1: Create a Zero-Dollar Budget

This means exactly as it sounds – you take every single dollar of your income and allocate it to a budgeted expense until income less expenses is equal to zero.

Before you break down your budget into two paychecks, it’s necessary to create your total monthly budget as the framework from which to work.

Here’s a detailed guide for creating your zero-based budget.

No spam—just simple budgeting help for your home.

Step 2: Assign Every Expense to a Paycheck

Simply take your total monthly budget, and line by line split each budgeted expense into your two pay periods.

The expense can be split equally or not, you’ll just want to consider cash flow.

Consider Cash Flow

Think of your bank account like your fridge. You wouldn’t eat all your groceries on day one just because you planned your meals for the week…You’d spread them out so you have food every day.

Your paychecks work the same way—you need to spread your money so it lasts until the next one comes in.

Example:

Paycheck #1: $1,500

Rent: $1,200

That leaves $300 for 2 weeks of food, gas, and life…Even if paycheck #2 looks fine on paper, you’ll feel stressed in real life.

Use the Half-Payment Hack

Larger expenses such as your mortgage or rent might need to be assigned to more than one paycheck.

Right now, we are renting from my parents. Instead of setting aside the entire month's rent from one paycheck (we are paid weekly), I spread it across two.

Though I budget $900-$1000 per month for groceries, I set aside $450-$500 from two monthly paychecks rather than one paycheck.

By doing this, cash flow is stable (though we always have a one-month of expenses buffer in our account), and it helps me to actually stick to the budget by breaking the larger budgeted amounts into smaller, more manageable chunks.

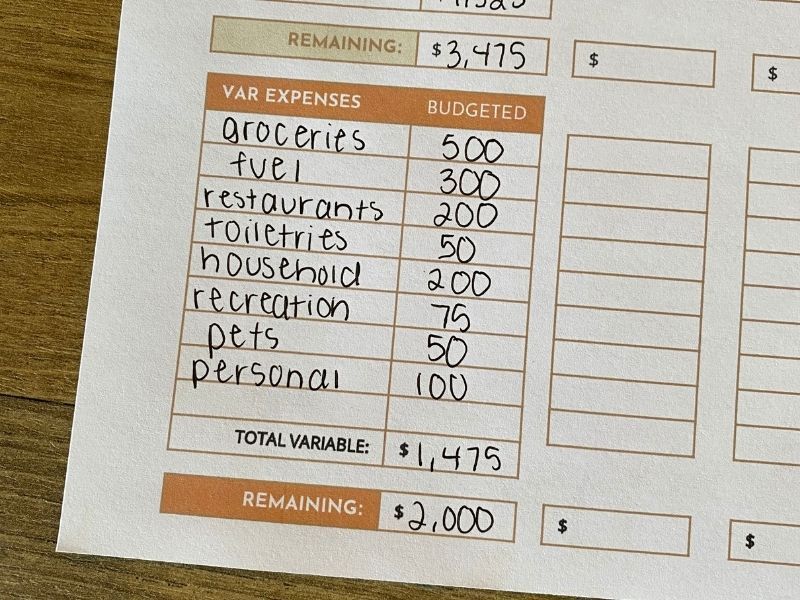

Step 3: Plan Variable Spending

Variable expenses are costs that change from month to month, expenses that you have more control over. For example, groceries are considered a variable expense because you can easily adjust the line item in your budget from $800 to $725 if needed.

Rent or mortgage payments would be considered a fixed expense, because it does not change month to month and can't be easily manipulated.

To plan variable spending in your biweekly budget, you can either divide it equally into your two pay periods, or budget for it out of one paycheck.

Personally, I like to plan for expenses like groceries on a weekly basis. This helps me keep our spending in check. We are paid weekly, so I divide our total grocery budget by 4, and allow myself to spend that much on groceries per week. I could budget for groceries out of the first paycheck of the month, but I find that I tend to overspend when I do it that way.

Step 4: Include Savings Goals and Sinking Fund Expenses

To be intentional about reaching your family financial goals, set up your budget in this order:

- Necessities

- Savings and investing goals

- Discretionary spending

Apart from not having a household budget at all, the mistake many families make is waiting to see what's "left over" after the month is done and setting that money aside for financial goals like saving and investing.

The problem with operating this way, particularly if you're living on one-income, is the money you think will be left over always seems to disappear before the month is over.

Your financial goals must become a part of your monthly budget. To do this, they need to be on paper. Specifically, they need a line in your monthly budget, prioritized before discretionary expenses such as vacations, entertainment, etc.

Step 5: Print Budget & Track

I know- a printed budget doesn't sound like an efficient use of your time. However, I'd urge you—especially if you're new to budgeting— to fill out a paycheck budget every month before switching to a digital paycheck budget.

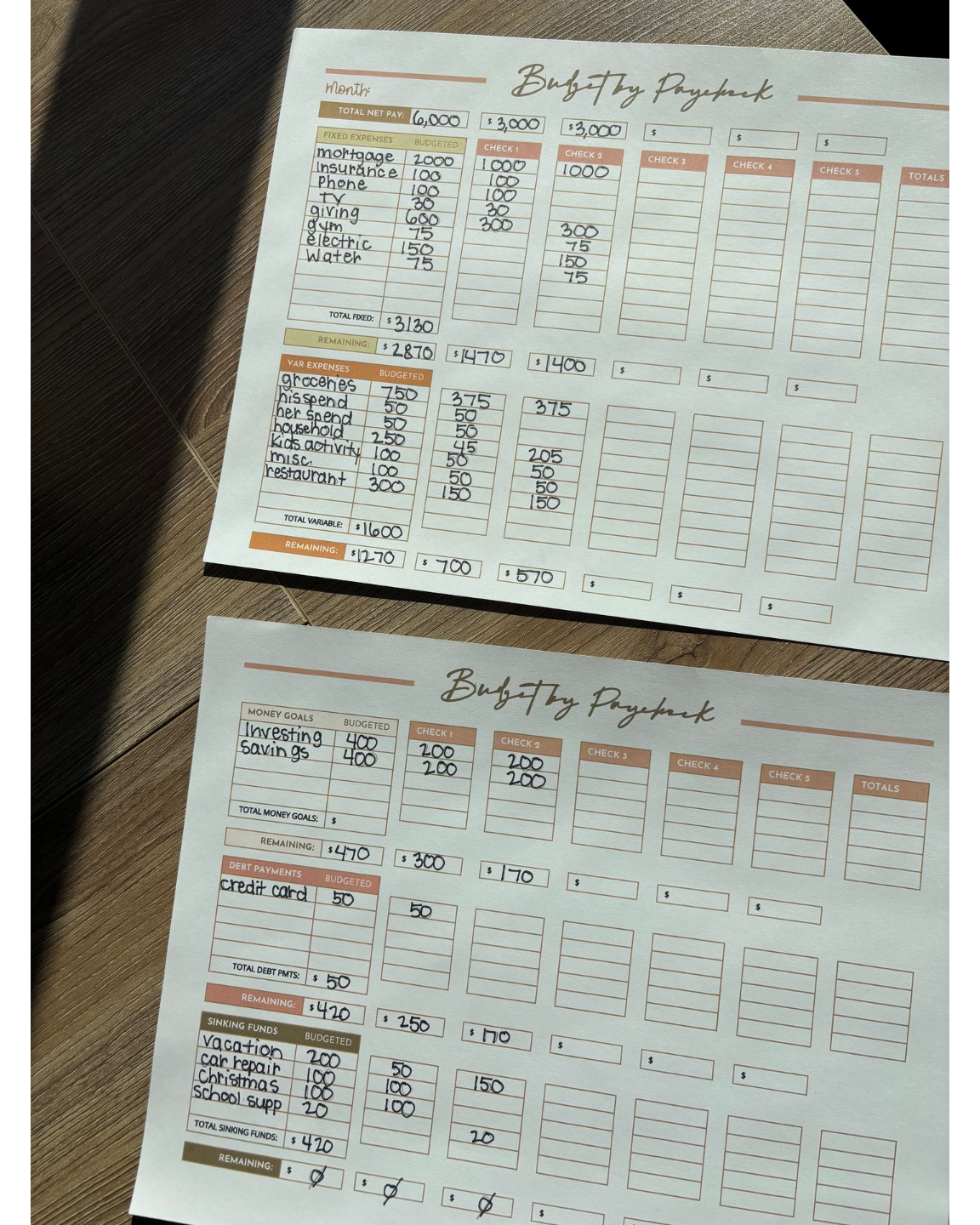

Example Bi-Weekly Budget for a One-Income Family

You can see on this biweekly budget example there are two columns filled out, one for each paycheck. Total monthly expenses are listed on far left column, along with budgeted amounts for each expense.

Notice that all expenses are planned for, including non-monthly expenses like vacation, car repairs, Christmas, and school supplies.

Though there may not be any cash out for these expenses this month, it's important that we set aside money for them. This way, when December comes, there is $1,200 ready to be spent on Christmas gifts and celebrations.

There's no credit card guilt following you into January!

What if You're Living Paycheck to Paycheck?

Determine True Expenses

If you’re living paycheck to paycheck, the very first thing you need to do is total up your monthly income and all your true monthly expenses.

You must pinpoint what is causing the cycle to continue.

Are there more expenses than income every month? Is there a single expense or category that takes up a significant portion of your income? Do you actually really know what you’re spending?

To calculate your true expenses, look over your last 3-6 months of bank statements. Group all expenses into categories, and calculate an average amount spent based on the past few months.

Here’s the key: include every single expense. You must get a true picture, not a vague,“here’s what I think we spend in my head” picture.

If you’re relying on mental estimation to determine your expenses, chances are you’re under-calculating.

You need real data to work with, not the estimate in your head. This might be the most overwhelming step for some. Stick with me here.

Make a Plan

Now that you know what your true expenses are, determine if your expenses are greater than your monthly income.

If so, you have two options-- either cut expenses or increase income.

This can be difficult if you're a one-income family who prioritizes having mom at home, because you're already probably cutting costs wherever you can, and increasing income would potentially require you to neglect your primary responsibility-- the home.

Your husband is probably already working hard just to make ends meet as it is, bearing the financial load for the whole family.

So what to do? Where do you go from here?

While I can't tell you exactly what to do, I can share from experience what's worked for us when faced with the same situation.

How We Have Cut Costs When Funds are Tight

When I first quit my job as a CPA to stay home with our kids, our budget barely penciled out. We knew there were budget items we COULD cut, like tithing, but we were convicted to continue to tithe despite the perceived "financial strain" it was putting on our budget. So that was out.

So what could we cut? How would we make it work? We could make it by, but it was going to be a razor-thin margin every month.

First, pray. Ask the Lord for His wisdom, and that He might reveal to you how to be better managers of your finances and bless your efforts to honor Him.

Second,

act. Here are some things we have done to increase our margins:

- Cut out everything but necessities for a period of time.

- Used cheap protein for all our meals - chicken, pork, and beef.

- Got creative about entertainment. Found as many free or extremely cheap things to do with the kids as possible. Instead of taking them out for treats, we'd go to the library. I had to remind myself often they don't know the difference if we go to get ice cream or the library, they just like to go places.

- Bought in MAJOR bulk - more upfront cost but cheaper in the long-run. I still buy in major bulk from Costco, Sams Club, Azure Standard, and Thrive Market.

Remember, this isn't forever. Seek the Lord and His infinite wisdom. He promises to give it to those who ask.

What if my bills are due before I get paid?

This is one of the biggest challenges with biweekly pay. You have a few options:

- Use the previous paycheck to cover early-month bills

- Build a small buffer (even $500–$1,000 helps)

- Adjust due dates if possible

Over time, your goal is to get ahead so your money is waiting before bills hit.

Should I still create a monthly budget?

Yes—but think of it as your big-picture plan, not your day-to-day system.

Your monthly budget shows:

- Total income

- Total expenses

- Overall financial goals

But your paycheck budget is what actually makes it work week to week.

What’s the best budgeting method for biweekly pay?

For most families (especially on one income), the paycheck budgeting method works best.

It allows you to:

Plan each dollar as it comes in

Avoid overdrafting between paychecks

Stay organized even when timing feels off

How can I make a 2 paycheck month feel easier?

Focus on creating a little margin over time:

- Build a small emergency fund

- Use sinking funds for irregular expenses

- Plan ahead during 3 paycheck months

Even small steps make a big difference in reducing stress.

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!