9 Important Sinking Funds You Need in Your Budget

melaniedj • 17 August 2019

Do you get stressed because you always seem to forget about a bill or expense and then it hits your checkbook like a brick?

I'd like to share 9 important sinking funds you need in your budget to properly plan for all your expenses.

A sinking fund is a strategic way to save for an expense or multiple expenses over time by setting aside money every month.

Although this is a simple concept, not many Americans seem to be practicing it considering the average American saves less than five percent of their income!

A sinking fund is a tool you need in your budgeting toolbox!

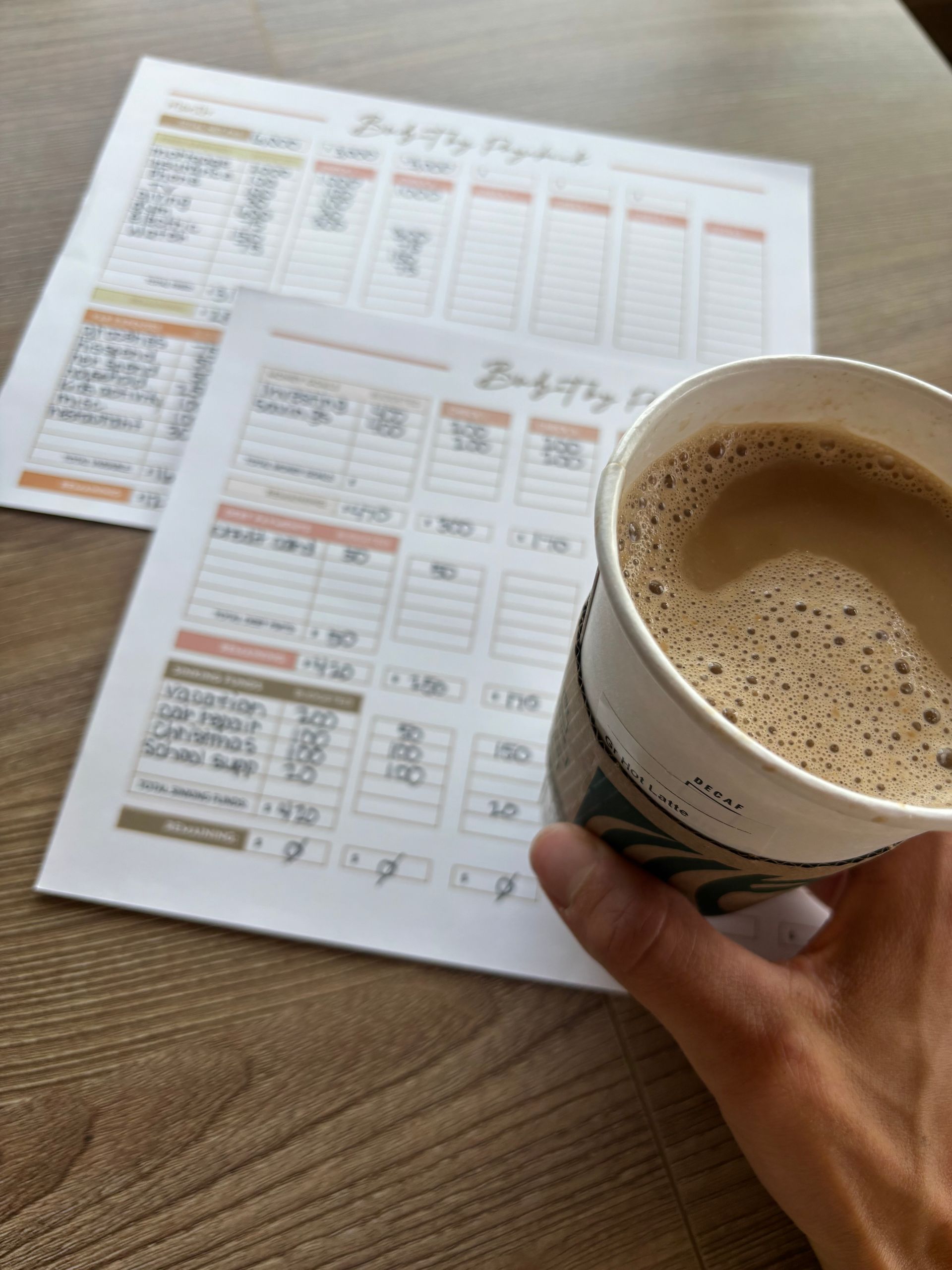

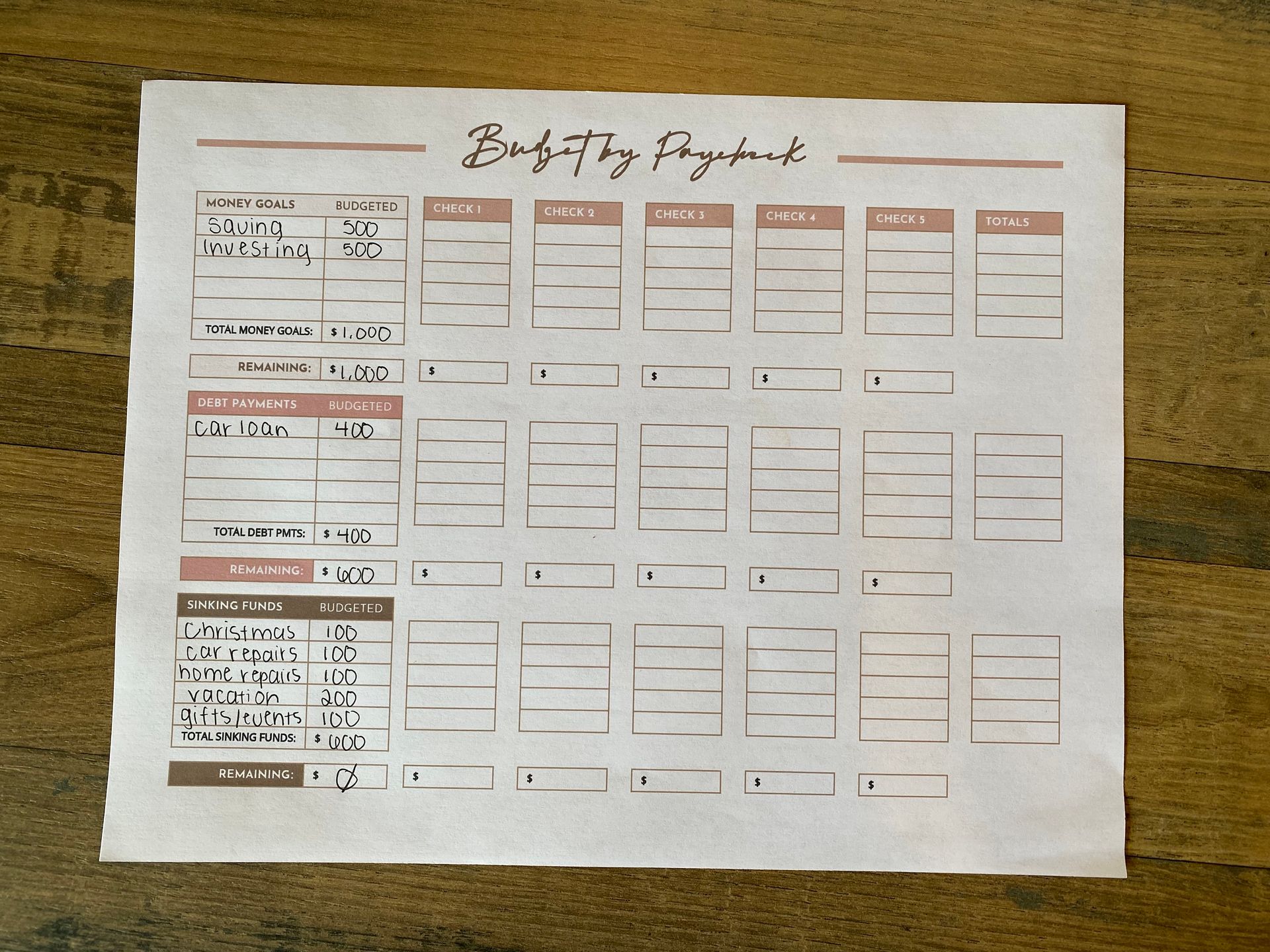

A SINKING FUND IS AN INPUT TO YOUR BUDGET

It's pointless to set aside money every month if you're not tracking where it's going, how much you have left, and making a plan for your hard earned cash.

Before you start setting up sinking funds,

you need to be on a budget.

Sinking funds are just a TOOL for your budget , not a replacement.

To get started on a monthly budget,

subscribe and get access to my

free monthly budget template!

Because budgeting is my bread and butter, I want to share with you my plethora of knowledge and help YOU succeed financially and have PEACE.

Don't miss out on these free tools, they are designed for you!

HOW TO SET UP YOUR SINKING FUND

WHEN YOU KNOW THE AMOUNT YOU NEED

Often times you know exactly how much money you need to save by a certain date. This makes setting up your sinking fund very simple.

For expenses that I know what the exact amount due will be (or can approximate), the formula looks like this:

Total amount needed/months to budget = monthly budget amount

For example, I know that I need an oil change every three months or so, and it typically costs around $60, so if I get my oil changed 4 times a year for $60, it costs $240 total.

If I take $240/12 months, that's $20 a month I need to save in order to be able to pay for my oil change when the time comes!

UNCERTAIN AMOUNT NEEDED

If you don't know exactly how much or exactly when you'll need money for a certain category (think medical, travel, gifts, etc), use the same formula above but evaluate often.

I do a rough estimate of the amount needed, and then I adjust my monthly budgeted amount as needs arise.

For example, I have no idea when medical costs will arise (most of the time) or how much they'll end up being.

Basically, I just know it'll be expensive... am I right?!

So if I estimate we will spend $2,000 on medical expenses every year, I should budget around $150 per month for medical costs.

This year, we got a bill for my son for $1,000 and I only had $600 in my medical savings fund. Once we got the bill, we took as much extra out of the next paycheck as we could (without sacrificing our investing), and paid for the rest using our emergency fund.

Then, we replenished our emergency fund to get it back to where it was.

The key is that we did not sacrifice our monthly investing amount.

We cut costs elsewhere, used our emergency fund, and then replenished the emergency fund the next month!

1. TRAVEL

We just returned from a week long trip to the Oregon coast, and we take several vacations like this a year while living on one income!

When you are strategic with your money and treat it well, it will treat you well.

I set aside a little bit of money every single month for our travel fund whether we have a trip planned or not.

We don't go anywhere until we have the trip fully funded and paid for in cash, this allows us to take stress free vacations that don't follow us home (on a credit card).

2. CAR MAINTENANCE/REPAIR

It's a good idea to have a sinking fund for car repairs, maintenance, and/or a car replacement if you will need a new vehicle in the foreseeable future.

We having a car sinking fund set aside for registration, regularly scheduled maintenance, and repairs.

It's a great feeling when you find out your car needs a $500 repair and you have the money set aside already!

3. HOME REPAIRS

Every home owner should have money set aside for home repairs, because it's not a matter of if something will break/need replacing, it's a matter of when.

Anyone who has bought a home knows that Murphy comes to visit when you least want him to.

Whether it's the A.C. that breaks down, roof that needs replacing, or basement that floods, it's best to be prepared instead of scratching your head wondering how you're going to pay for it.

We have money set aside for home repairs and a remodel that we are currently working on!

4. CHRISTMAS

PSA: Christmas comes at the same time every year!

Duh, right? Well research shows that Americans on average racked up $1,000 of holiday debt and and had no plans to pay it off right away.

Don't rack up a holiday hangover that will follow you until July when you finally pay off your credit card.

Instead, save money for Christmas every single month.

5. MEDICAL

Medical costs are inevitable, so be prepared for them .

Rather than being depressed when your $2k bill for a physical comes (kidding.. kinda), set aside money every month so that you have a good head start.

This is probably the biggest sinking fund expense we've had the last few years.

We pay $200-$300 every single time we go to the doctor, and we paid thousands of dollars to have our son.

While it's a tough pill to swallow paying the bill, I can be thankful that we budget and were able to write a check for birth expenses.

6. MEMBERSHIP DUES

Gym dues, magazine subscriptions, and any other membership dues should be tracked and paid for in a sinking fund.

Dues and fees are easy expenses to forget and have sneak up on you!

Make a list of all dues, fees and registrations you have due during the year and divide by 12 to figure out how much you need to save monthly for each.

It's too cumbersome to have a sinking fund for EVERY due/fee, so I'd recommend just having one fund.

7. SCHOOL FEES/REG/SUPPLIES

I don't have to budget for school expenses quite yet, but I know they add up fast and it seems like there always a field trip, extracurricular, or other expense for school related activities!

While I wasn't very aware of it at the time, I think about all the expenses my parents paid for me over the course of my school years (on top of the tuition expense for a private school), and it's got to be a good chunk of money!

Especially parents who have kids that are involved in a lot of sports, my advice is to BUDGET. BUDGET. BUDGET.

Also, if you have to sacrifice retirement savings, house savings, etc. to pay for your kids club or AAU sports, it's ok to say no. Really, it's fine.

It's important to let your kids know that if something isn't in the budget, it's not happening.

8. PET

Pets can get really expensive really fast, put them in the budget!

I've heard that a dog surgery can cost just as much as a human surgery! If that's the case, you might be out a few grand unexpectedly if your pet has health issues.

Just like you put food and medical expenses for yourself and your family in the budget, put the pets in the budget, they're part of the fam!

9. GIFTS

Another highly used sinking fund category in our budget is gifts.

Baby showers, weddings, bridal showers, birthday parties, family birthdays, anniversaries, etc. happen almost every single month!

In any given month, it's almost guaranteed we will have some sort of gift to buy.

If I budget for it, it's a lot more fun to shop for the gift, and that's the beauty of a budget.

A budget gives you PERMISSION to spend WITHOUT guilt. It sounds restricting, but really it sets you free financially.

There you have it- the 9 sinking funds you need to have financial success! Don't discount the power of sinking funds in your budget.

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.