The 50 30 20 Budget Method + Does it Work?

Melanie DJ • 3 January 2023

Using the 50/30/20 budget rule, you create a personal budget by dropping your income into three buckets- needs, wants, and savings.

This method is a great option for those who like a specific formula to follow and find budgeting overwhelming. This budgeting method does not focus on detailed budgeting and precise spending amounts, but rather a loose framework.

How the 50/30/20 Budget Works

50% Needs

Needs refer to expenses that you require to live, or necessities. Typically, this includes food, housing, utilities, and transportation.

- Mortgage or rent payments

- Internet, water, sewer, garbage, electricity

- Gas/fuel/public transport/parking

- Childcare/daycare

- Healthcare

- Groceries

According to the 50/30/20 budget rule, needs should account for no more than 50% of your monthly take-home pay.

30% Wants

Wants in your budget refer to discretionary expenses, or non-necessities.

- Personal spending

- Hobbies

- Subscriptions

- Entertainment

- Recreation

- Restaurants

- Vacations

- Nonessential services

Be very careful when putting expenses in this budget category. It’s easy to mistake our wants for our needs! For example, we often think of our subscriptions as needs when we could live without them. It might even be uncomfortable to live without certain wants, but that doesn’t make them a need.

20% Savings

The savings bucket is reserved for financial goals. Such goals might include (but are not limited to):

- Home down payment

- Investing for retirement

- Building emergency fund

- Saving for a car replacement

- College tuition savings

- Paying off debt

Finance goals should always be a line item in your monthly budget, and this budgeting method ensures they are covered. If you don’t put them in the budget, they won’t happen.

However, 20% doesn’t go very far when it must cover retirement savings, emergency fund savings, college saving, paying off debt, and other savings!

If you want to start the 50/30/20 budget, or any other budgeting method, you can get my free google sheets budget template below!

What’s Best?

Because of the plethora of options available when it comes to budgeting, it can be hard to pick what method will be best for you.

Benefits of the 50/30/20 Budget

The 50/30/20 budgeting rule has some major perks:

- The 50/30/20 budget offers a simple formula to follow. This is a welcome relief if numbers aren’t your strong suite and budgeting makes your head spin! Simply allocate your take-home pay to the three buckets and you’re done!

- One bucket is devoted to savings goals, rather than simply saving what’s left over. Putting your goals as a line item in the budget is necessary to achieve them!

- Offers an easy way for beginner budgeters to get started. Budgeting can seem overwhelming, especially when you are just starting. Using this method requires dropping every expense into 3 different buckets, which is simple enough that beginner budgeters won't get discouraged!

Overcomplicating the budgeting process can lead to discouragement. One of the biggest benefits of this budgeting method is the simplicity it offers.

Disadvantages of the 50/30/20 Budget

No two budgets should look the same, because no two people are in the same stages of life or have the same life. A budget should be a unique, personal plan tailored to your individual needs.

- One-size-fits-all framework. A major drawback to this budget method is there is no consideration for your age, current retirement savings, debt, or your unique financial goals.

- Savings bucket is only 20% of take-home pay. If you follow the recommended 15% investing rule, that leaves only 5% of your income to split between paying off debt and other savings goals!

- Doesn’t work well for very low-income earners or very high-income earners. Someone making minimum wage will probably need to allocate more to necessities, and a high-income earner might not need to allocate so much to discretionary spending.

Using this budgeting equation, someone who has $100k in debt would still be allocating 30% of their income to wants! In my opinion, that is not wise. One of the reasons we were able to dig ourselves out of $20k in student loan debt in 12 months (living on one income) is because we cut our wants down to almost nothing for a short period of time. If we had used this budgeting method, it would’ve taken at least double the amount of time to get out of debt, and we likely would’ve lost motivation along the way.

A 70-year-old retiree’s budget will and should look different than a 25-year-old with little kids trying to get out of debt. The latter should have a greater portion of their income, if possible, going to paying off debt. The former might have more of their income allocated to wants and less to savings goals (because they’ve already hit them).

Ultimately, your budget needs to be a unique, custom plan tailored to your individual needs.

Follow along below for how I recommend budgeting in a way that reflects your needs, priorities, and keeps you engaged in the budgeting process.

How to Make an Effective Budget Plan

For detailed instructions for setting up a monthly budget, click here.

- List your total expected monthly income.

- Calculate and list your fixed and variable monthly expenses.

- Brainstorm and put non-monthly expenses in the budget by converting them to monthly amounts.

- Include finance goals in the budget.

- Budget for discretionary spending.

- Subtract total income and expenses.

- Track your spending!

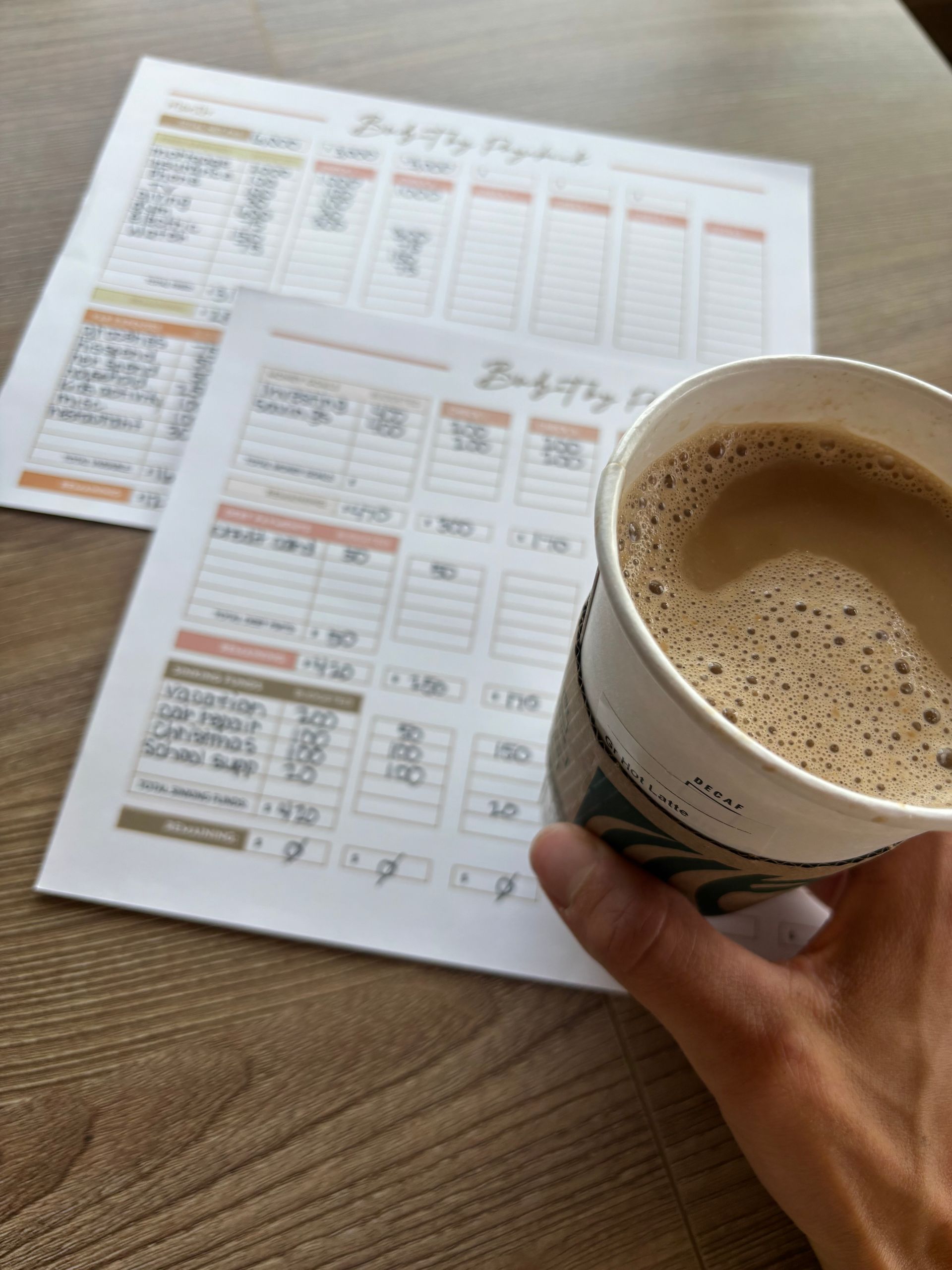

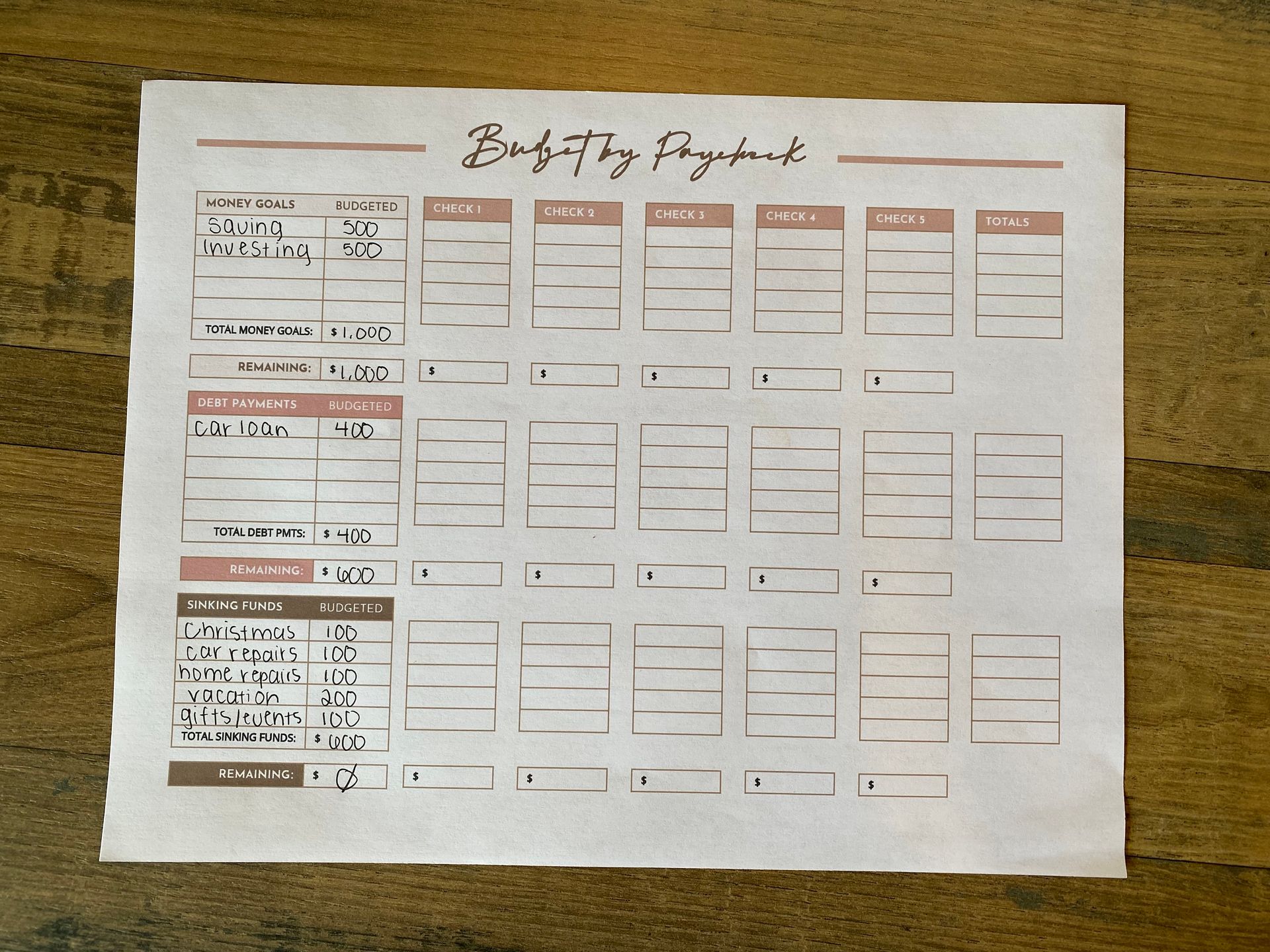

Take your budget a step further and use the paycheck budget method, allocating every single budget line item to one or multiple pay periods. Essentially, you create a budget for every pay period based on your total monthly budget.

Follow this YouTube video as I walk you step by step through the paycheck budgeting process!

You can use the paycheck budget method for the 50/30/20 budget, or any other budgeting method you choose!

I've found that breaking my budget down into smaller, more manageable chunks by pay period helps me stick to my budget. Give it a try and let me know how it goes!

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.