100 Envelope Challenge to Save Money Quickly

Melanie DJ • 5 January 2023

The 100 envelope savings challenge is a daily money saving challenge that helps you develop positive money management habits while saving over $5,000!

While completing money saving challenges won't make you wealthy, a savings challenge can help you develop positive money management skills and overcome impulsive spending habits. Additionally, completing a savings challenge is a great way to save up for a large, future expense little by little.

If you look at what you need to save, it can seem like an impossible feat. However, anytime you break your end goal down into smaller, "mini-goals", it will seem more do-able!

A visual that tracks your progress is a helpful and motivational tool, so be sure to get my free printable savings tracker before you start!

100 Envelope Money Saving Challenge

This savings challenge will help you develop self-discipline with your money, so you can stop impulsive spending habits and train yourself to save.

How it Works

After completing the 100 envelope money saving challenge, you'll have saved over $5,000 in just 100 days! Completing the challenge is very simple, just follow these steps:

- Start with 100 envelopes and label them 1-100.

- Put the envelopes in a basket, bin or other storage container.

- Everyday for 100 days, randomly pick an envelope and put the amount of cash that is on the label inside the envelope.

- Put the envelope somewhere safe and repeat the process for 100 days.

- Deposit your $5,050 dollars and decide what you will do with your cash! You can save it, invest it, pay off debt, or spend it.

For example, if you randomly select an envelope and it is number 40, seal and put $40 in that envelope.

Tips for Success

- Keep a visual reminder to track your progress. It's helpful to keep a visual progress tracker somewhere you see it everyday, like your planner or on your refrigerator. Fill in the visual as you get closer to your savings goal to help you stay focused and motivated.

- On days you draw a large number, revisit your finance goals. I'm sure you've heard it said that keeping your "why" in mind is important. This challenge is no different! Make a collage, tape pictures to your desk, etc. Do whatever it takes to stay on track.

- Complete the challenge digitally instead of with paper envelopes. An alternative option to the physical challenge is completing the challenge digitally. To do this, open a separate bank account to deposit your funds into. You can either 1) Label physical envelopes and draw everyday, but instead of putting money in the envelope make a deposit into the bank account 2) Use an online generator to randomly pick a number from 1-100 for you and deposit that amount into the separate bank account.

- If you miss one day, don't miss two! The hardest part of sticking with a savings challenge is doing it daily. If you do miss a day, don't miss two. Once you develop a habit of inconsistency, it can be hard to get on track and finish the challenge. Don't beat yourself up over missing a day, but don't let it become a habit!

Other Ways to Save Money

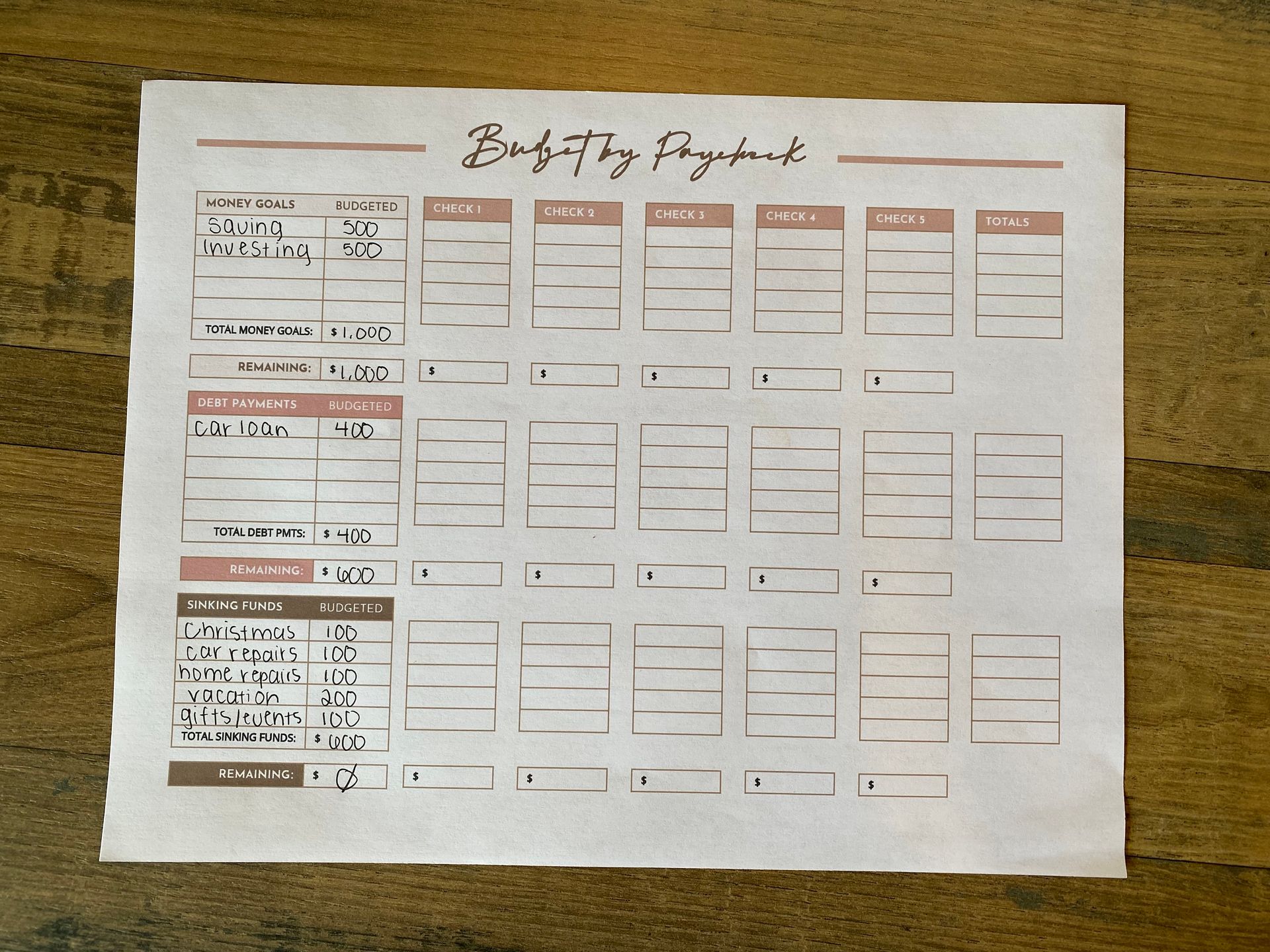

1. A Monthly Budget

Ultimately, it's difficult to save money if you don't have a routine plan for how you'll do it. A monthly budget is one of your biggest tools to save money because you know exactly where your money is going.

Create your first monthly budget using my detailed instructions.

Get my free printable monthly budget template, or my google sheets budget template if you prefer to track your budget digitally!

2. Pay off Debt

Saving money is hard when your income is tied up in monthly debt payments. Upon completing this challenge, consider using the funds to pay down your debt.

For a strategic plan for paying off debt, follow the debt snowball method. Once you're out of debt, it will suddenly feel like you got a raise! This will free up disposable income to put towards your financial goals.

3. Cancel Subscriptions

One of the best ways to quickly cut spending is to review your subscriptions. Cancel any monthly subscriptions you don't use regularly, and turn off the "auto-renew" feature. This will force you to evaluate every renewal period whether you're using the subscription enough to warrant renewal.

4. Use Cash Envelopes

Cash envelopes are a budgeting tool used to deter impulsive spending habits. The idea is to force yourself to stick to your budget by keeping certain budget categories/expenses tucked away in your cash envelope. Studies have shown that when we use cash instead of a card, we spend less because cash affects our brains differently!

Brainstorm budget categories that you tend to overspend on, then when you are paid, put the amount of cash you've budgeted for the month into that envelope. alternatively, you can take the cash out weekly, or bi-weekly, whatever works best for you! For example, if you budget $600/month for groceries and you are paid weekly, you can take withdraw $150 per week. The key is once the cash in the envelope is gone, that's it! You're done.

Give the envelope method a try! It works great for budget categories like groceries, personal spending, beauty, clothing, etc.

5. Don't Save Card Info Online Shopping

Click. Click. Buy! Online shopping has become SO easy that it's persuading us to make impulsive decisions. When your shipping address, card info, and contact info is already filled in on your favorite website, it makes it that much easier to justify our purchases. If you want to save money, don't save any of your card information on any websites. Force yourself to take the extra step to get your card and fill in all the information. It will give you a little more time to think about your purchase.

6. Unsubscribe from Store Emails

Our inboxes are another source of persuasion for impulsive purchases. Have you ever given a site your email to get a coupon code, only to be bombarded by emails everyday after the fact? While this can be helpful for things like being informed about sales, it can also encourage impulsive spending.

7. Ditch Credit Cards

When you don't have any credit cards, you can only buy what you can afford. This forces you to evaluate every single purchases, carefully weighing the costs and benefits. Personally, we don't have a single credit card, and I've never thought twice about it. Not because I didn't think it would be nice to have more disposable income, but because it's not even an option. We took that option off the table, and now we don't ever think about it! It forces us to decide what is really worth our hard-earned money.

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.