How We Paid Off $20k of Student Loan Debt in 12 Months!

melaniedj • 17 September 2017

Unfortunately, they don't do Black Friday deals on student loans. Or accept tears as a form of payment.

If you're anything like me, the high of graduation and the sense of self-accomplishment that comes with getting a college degree wore off pretty fast when I opened my first bill saying 'Your grace period has ended. See payment due inside.'

There it was- the debt sentence.

When you're in college, you kind of push the thoughts of student loan debt to the back of your mind and tell yourself to not worry about it, you'll have no trouble paying it off after you graduate.

The reality of the situation is that most students on average have about $37,000 of debt when they graduate college.

But wait-there's more. Approximately 60% of millennials have no idea when their loans will be paid off!

I guess ignorance is bliss?

I came out of college with approximately $25,000 in student loan debt (My husband Joe didn't have any), and with A LOT of hard work and perseverance, we were able to pay off over $20k (including interest) of student loan debt in 12 months.

We decided early on that debt is a poor master and that we didn't want to live the American dream on credit.

Below I have listed what I've found to be the most important things that have fueled us in our journey out of debt.

How We Paid Off $20K of Student Loan Debt in 12 Months (Living on One Income Part of the Time)

1. We Live Below Our Means

Seems pretty straightforward, right?

Apparently not, because nearly half of American households spend more than they take in every month and are using debt to fill in the gap between income and expenses.

According to Nerd Wallet's recent study, Americans are now on track to surpass the amount of household debt owed at the beginning of the Great Recession!

We don't spend more than we take in every month.

It's a pretty simple rule, but harder than you think to follow!

Get in a habit of not living paycheck to paycheck. We had to learn this when we only lived off of my income while Joe was in school, because we still wanted to be able to make extra payments on my student loans every month. Consequently, we had to live well below our means.

We live on less than half of our income.

This has left us with enough money to pay off debt, save, and invest. That will change when we have kids of course, but that is what we do right now.

If you are living on more than your income, you either need to cut expenses or make more money.

2. We Don't Care What Other People Think

HINT: If people are making fun of you, you know you're on the right track.

It has taken me a LONG time to get to this point.

Truth is, what you drive doesn't define you. Where you live doesn't define you. The stores you shop at don't define you.

Sure, someone else might have a brand new car on payments, a brand new house with a monthly payment that is more than they can afford, or a brand new whatever else on payments. Or, maybe they paid cash for it! Either way, you don't know (unless they have personally told you), so who cares?

I drive a 2004 Ford Escape I paid $4,000 for that I've had for 5 years with 205,000 miles on it. It's not the fanciest, but it gets me from point A to point B and I don't have a car payment!

According to statistics released by Experian Automotive, the average car payment is $493/month in America.

If you invest $490 per month in a good mutual fund that averages 12% over the course of 10 years, you will have more than $110,000.

Hope you like that car.

3. We Made Payments During the Grace Period

We didn't get married until the December after I graduated college, so during that time we were saving for our honeymoon, my wedding dress, and our trip out to Washington (We paid about $4,000 out of pocket for travel and my dress).

It was tough because Joe was in school and only working after school, and even though I was full-time, we planned a trip out to Washington during the summer in addition to the wedding so that took some saving as well.

I made cash envelopes for all these expenses, and every pay period I would take out cash (what was left over after my student loan payment), and allocate it to each envelope.

If you need to curb your impulse spending habits, I designed the beautiful floral watercolor cash envelopes pictured below!

Start saving money by using cash for certain expenses!

Another tip- I kept the envelopes outside of my purse so that I wasn't tempted to use them for other things.

Additionally, I made a tight (and I mean TIGHT) budget so that I could still pay around $700/month on my loans, which was all principal! It would have been easy to not pay anything during the grace period (the 6 months after you graduate), but I knew it was smart to do so!

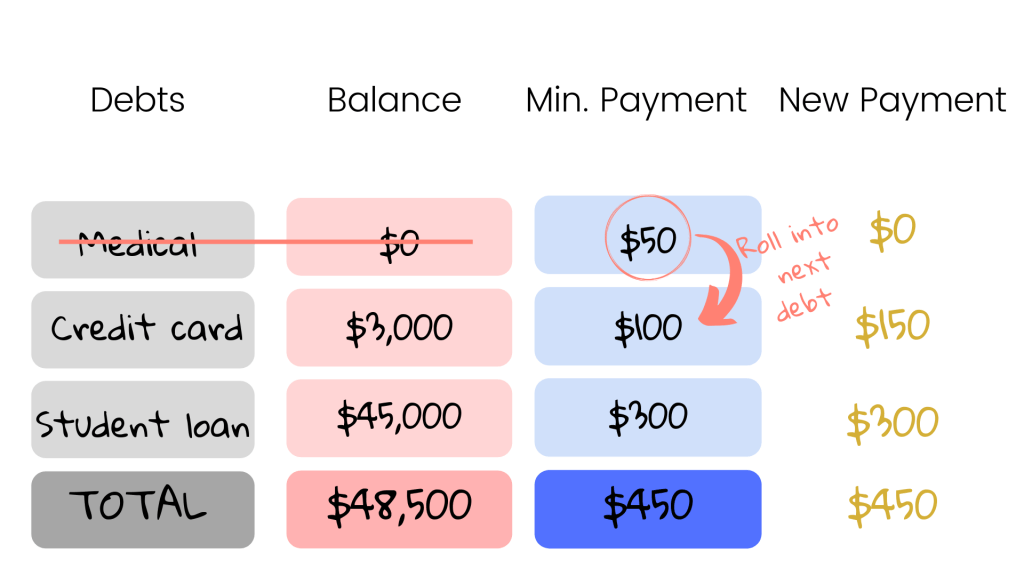

4. We Tackled the Smaller Loans First

I know that this sounds backwards, but I tackled the smaller loans first. This way, you get an easy win and it will fuel you to continue and be encouraged to stay on track!

When you make a regular payment on your student loans, it is distributed across all the loans. When you make an extra payment, you can choose which loans you would like to apply the payment to.

I started off paying all the $1,000 to $2,000 loans first, and then worked my way up. I also think that this way paying off your loans early doesn't seem so out of reach.

DEBT SNOWBALL EXPLAINED

If you focus on one at a time and knocking off the small ones first you will gain momentum. This is why it is called the debt snowball method.

Here's an example:

You can see from the example how the snowball builds as you pay off your debts.

The goal is to gain momentum and be as aggressive as possible!

If you'd like to use the debt snowball worksheets that we used during our debt payoff journey, they are available in my Etsy shop!

These are editable PDF's, meaning you can type directly into them & print!

Create a visual for yourself to keep you motivated and take pride as you fill in your amounts paid off!

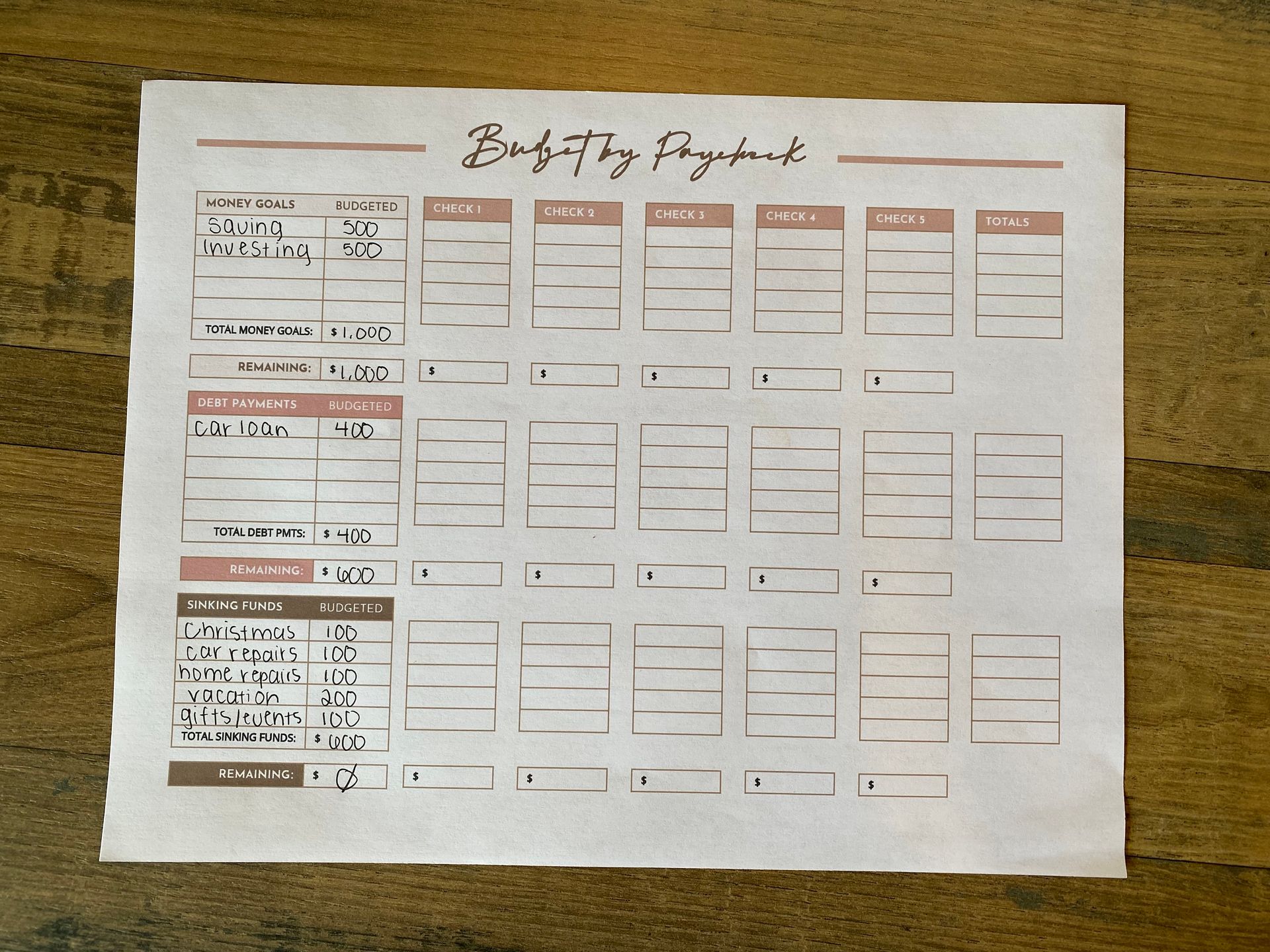

5. We Have a Monthly Budget & Found What We Can Cut Out

First and foremost, if you haven't already, keep good track of what you make and what you are spending every month (keep track by category).

At the end of the month, evaluate the results (and try not to faint). If you don't know how to start a budget or have never used one, read this post .

YOU NEED A BUDGET

If you don't know where your money is going, it's going to be hard to find money to put towards your debt. If you adopt the mentality that you'll use whatever is "left over" at the end of the month to pay down debt, you'll find there's never any money left to put towards it. It has to be in the budget as a line item.

Above you can get my exact budget template I use every month for FREE. I created this spreadsheet after going through much trial and error trying to find a budgeting method that works for us.

BREAK IT DOWN TO THE ESSENTIALS

When we first got married, Joe and I had a habit of going out every weekend with friends- whether it be to an wedding, a party, a bar, etc.

I thought I had a good idea what we were spending on eating out and entertainment every month, but when I actually tracked every dollar I was blown away!

We were spending $500-600/month on entertainment!

That Raspberry Margarita that cost $10 suddenly didn't taste so good.

Now, we go out to eat once every two weeks.

Yes, you read that right. Over the past year, we took the extra $400/month that we were spending and put it towards my student loans!

I'm not saying you shouldn't ever see your friends. I am saying that it's okay to suggest other things (that don't cost as much or any money) to do with friends. Buy your own drinks and play cards!

We also managed to cut $100 out of our grocery budget every month by meal planning!

For two people, our grocery budget is $300/month and we waste way less food than we did before.

What about you, what can you cut out?

6. We Make Our Extra Payments First, and Spend What is Left Over

When I did the student loan counseling, the quickest payment plan was 10 years. As a result, in order for us to pay it off we would have to make more than the minimum payment, and you will have to as well if you are determined to be debt-free!

Just like with our church giving, every time we are paid I immediately write a check for our tithes and I would immediately make the extra student loan payment.

This way, we can only spend what is left over and not vice versa .

I do the same with money we get for gifts. For instance, for our wedding I made a $1,000 payment right away and then what was left over we used for living expenses.

When we would go to Washington to visit family, if we had any money left over from our vacation budget (usually $100-200), that went right to my student loans before we even had the chance to spend it on anything else.

7. We Pay Cash (Physical or Debit Card) For Everything

Cash is KING.

We do not have any credit cards, nor do we plan to get any (click here to read why).

We both have a debit card and that it all we use and all we have ever used. If we don't have the money in our bank account to pay for something, we don't buy it. It's that simple.

When you pay with a credit card or even a debit card for that matter, it is less painful than if you pay with cash. You do not see the money actually leaving your hand.

Joe and I have certain things that we only use physical cash for like groceries and our personal spending money or our 'fun money'!

Otherwise, we use our debit card or checks (for tithing).

8. We Cut Out Small Expenses That Add Up

We watch our small expenses too. I'm not saying you have to be a slave driver when it comes to budgeting, but beware of the small things that add up like latte's (my guilty pleasure), fast food, gas station snacks, etc.

We agreed to budget $60 per week for each of us to spend on whatever we would like and the other person can't complain about what they spend it on.

This way, you can have some guilt-free spending every month! Once the $60 budget is out, that's it- no more until the next pay period!

Early in our marriage, we didn't keep very good track of personal spending and that led to quite a few arguments.

This is a win-win, we argue a lot less (we still have those days we argue about money, it is HUMAN) and we save a lot more!

If you can't think of any small expenses to cut out of your budget, read 8 expenses that you are probably spending too much on.

9. We Make Sure We Prepare for A Rainy Day

We always set aside money in your budget for a rainy day.

It was hard to discipline myself to set aside this money, because what I really wanted to do was add it to our extra student loan payment.

Trust me, the second you get passionate and focused on paying off your debt, the rainy day will come and boom there goes the extra payment!

So even while paying debt, make room for rainy day expenses.

In our monthly budget, I usually set aside at least $100 for repairs in a sinking fund.

That way, when the car breaks down and it's going to cost $500 to fix (my husbands most recent fix was $4,100) we already have the money, or at least a good start.

Additionally, we don't have to dip into savings and can still make the extra payment on debt!

10. We Make Sacrifices

I want to be completely transparent with you guys about our journey out of debt- it is not easy. In fact, it's really hard, and it WILL require sacrifice.

I started making the sacrifices necessary to pay off my debt in college. I always worked during school, and I started making payments on my student loans before I was even out of school.

Further, I didn't 'reward' myself with anything for graduating college. I already had a big 'reward' - $25k in student loans!

These are the principles that have worked for us to pay off $20k of student loan debt.

Hopefully this post has given you some ideas and encouragement!

Be sure to follow me on Pinterest for more money saving tips and debt payoff tips!

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.