How We Budget on One Income as a Family of 6+ Our Exact Budget Template

Melanie DeJong • 26 June 2026

Whenever I mention that our family of six lives on a single income, people sometimes react with, "Wow! It must be such a blessing to have that option!"

While having this option is an incredible blessing, it isn’t one that comes without real sacrifice. Most people automatically assume we must just have an abundance of money and never have to give it a second thought.

This couldn’t be further from the truth! In fact, it’s something we have to regularly, intentionally think about in order to make it work.

It requires careful thought, prayer, and sacrifice. Every single month. Every single year.

If we’re actually looking from a birdseye view, our real income has decreased as we’ve added more kids, due to inflation.

So we’ve added more kids to our family since we started living on one income, and our real (inflation-adjusted) income has gone down.

So how are we able to do it?

How to Live On One Income With a Family

You Have to Know Where Things Are

Living on one-income requires working with actual data. Not “estimates” or running totals I keep in my head. I might think I have “an idea” of what we spend on groceries, but that doesn’t cut it.

Every single time my “idea” of what we are spending on any given expense category in a month is way off from the actual.

As a general rule, you’re almost always spending more than you think you are. At least that’s been our experience. There have been seasons (more on this later) of financial abundance where we could “get away with’ loosely knowing what we were spending.

Now, we’ve never utilized that framework for our finances because in those seasons we try to be extra-intentional to plan for seasons of less abundance.

Ignorance is Not Bliss

While it’s tempting to have an

“ignorance is bliss”

mindset, this is not wise for one-income families.

I get it – most of us one-income families are busy with lots of little kids at our feet all day and a never-ending list of responsibilities. Tackling the finances on top of it all seems like trying to climb Everest.

It IS hard to think about your financial situation, especially if it’s less than desirable.

But, I promise it brings freedom. Even if you’re looking at your finances and they are a complete mess, at least you know.

Now you can come up with a plan.

Getting out of Debt

One season that I look back on with no regrets is our getting out of debt season. While it was hard, I can see now how worthwhile it was. If we hadn’t paid off my student loan debt before getting pregnant 9 months into married life, life would have looked a lot different.

Having made the sacrifice early on to become debt-free (besides our mortgage), enabled us to take the risk of me

quitting my job to be a stay at home mom.

If, right now, at 32 with four kids, we had not paid that debt off and still had the monthly student loan payment, it would hurt a lot more now than it did back then. We simply don’t have as much margin as we did when we were double-income no-kids… although it was a brief time in our lives, as we had kids right away.

At the time, it barely penciled out for me to come home. But saying yes to that risk would have been a lot harder if we still had student loan debt lingering around.

We followed Dave Ramsey’s

debt snowball plan to pay off debt rapidly, and I do highly recommend his plan (although I’ve changed my mind on some of his advice).

Taking Prayerful Financial Risks

In general, women thrive on security. We want to know there’s going to be a steady paycheck coming in, preferably at the same time every single month.

This is part of the good design that our Lord and Creator gave us women in order to be a suitable helper to our husbands.

However, we also have to be willing to take a step of faith and trust the Lord in certain situations– including our finances. This takes thoughtful prayer and seeking the Lord for discernment with our money.

It was “risky” to quit my job as a CPA to become a stay-at-home mom. Dave Ramsey probably would’ve advised against it.

But we prayerfully considered our options and took a step out in faith that the Lord would provide and that my main priority and focus should be the home, not the workplace.

Understand the Seasonal Nature of Family Finances

In the past, I thought that if every season of life wasn’t a saving season, we were failing.

I’ve come to realize that certain seasons– like adding more children, unexpected financial hardship, etc.-- require more faith and cause us to stretch, grow and trust the Lord more than others. I call these “shrinking” seasons, because often there is little margin and a lot of faith required. You’re not in super-saving mode.

On the other hand, certain seasons– like when you’re newly married and maybe experiencing the double income no kids situation– are often seasons of abundance, or stretching. You’re able to spread your money more broadly, and can “get away with” being a little less strict or intentional with your money. Although, a wise person in a season of abundance will still be super intentional with their money!

With four kids, one-income, and having recently moved to one of the most expensive states to live in, we are in a shrinking season– financially, time-wise, and energy wise for mom ;)

That doesn’t mean we're failing. It has required me to trust the Lord with our finances more than ever, and let go of my controlling and fear-driven mindset when it comes to our family finances.

How to Budget On One Income as a Family

Why a Monthly Budget Wasn’t Enough for Our One-Income Family

When I first started budgeting, I simply tried to create a monthly budget and follow it. I quickly became frustrated as I struggled to reconcile our monthly budget to our paychecks, which were weekly for my husband and (at the time) biweekly for myself.

So we had six paychecks. As money came in, I tried to spend and look at our monthly budget and see how much we had left for each budget category. I quickly realized this wasn’t detailed enough, making it harder for me to follow and stick to.

I needed our budget broken down into smaller, more manageable chunks.

That was the key.

Paycheck budgeting

aligned our spending with the exact rhythm of our income.

Our One-Income Budgeting Method in 7 Steps

This is our current simple, repeatable paycheck budgeting system:

- Close out prior months budget.

- Glance at next months calendar.

- Update google sheets budget for month.

- Assign each expense/line item to a paycheck.

- Update EveryDollar.

- Adjust sinking fund balances.

- Reconcile budget balance to bank account balance.

It's a simple process, which is exactly what busy moms like myself need. It has to be realistic, otherwise you won't stick to the system.

Close Out Prior Months Budget

Before I budget for a new month, I go to my EveryDollar app and reconcile the balances of our budget “items” (essentially all the balances of every expense line) and reconcile it to our checking account balance. This way I know exactly where things are ending up for the month before I begin a new month.

Glance at Next Month's Calendar.

I look at our calendar for the upcoming month I am budgeting for. Once you get into a rhythm and determine what your actual budget needs are, you really won’t need to update your budget template much. You’ll be budgeting the exact same amounts month to month with little variance, with the exception of a major change of season for your family. Examples of this might be adding a new baby, moving to a new area, taking a new job, etc.

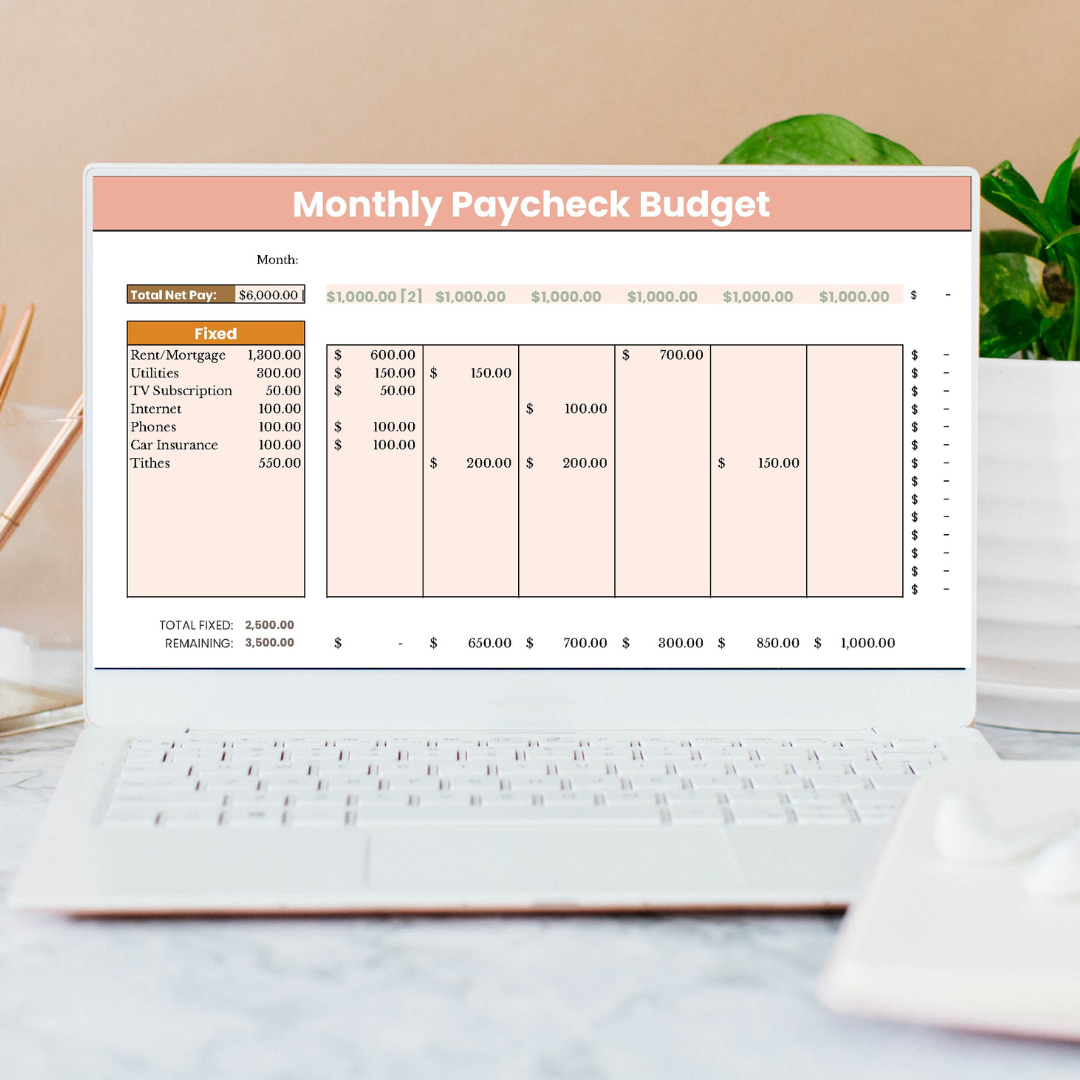

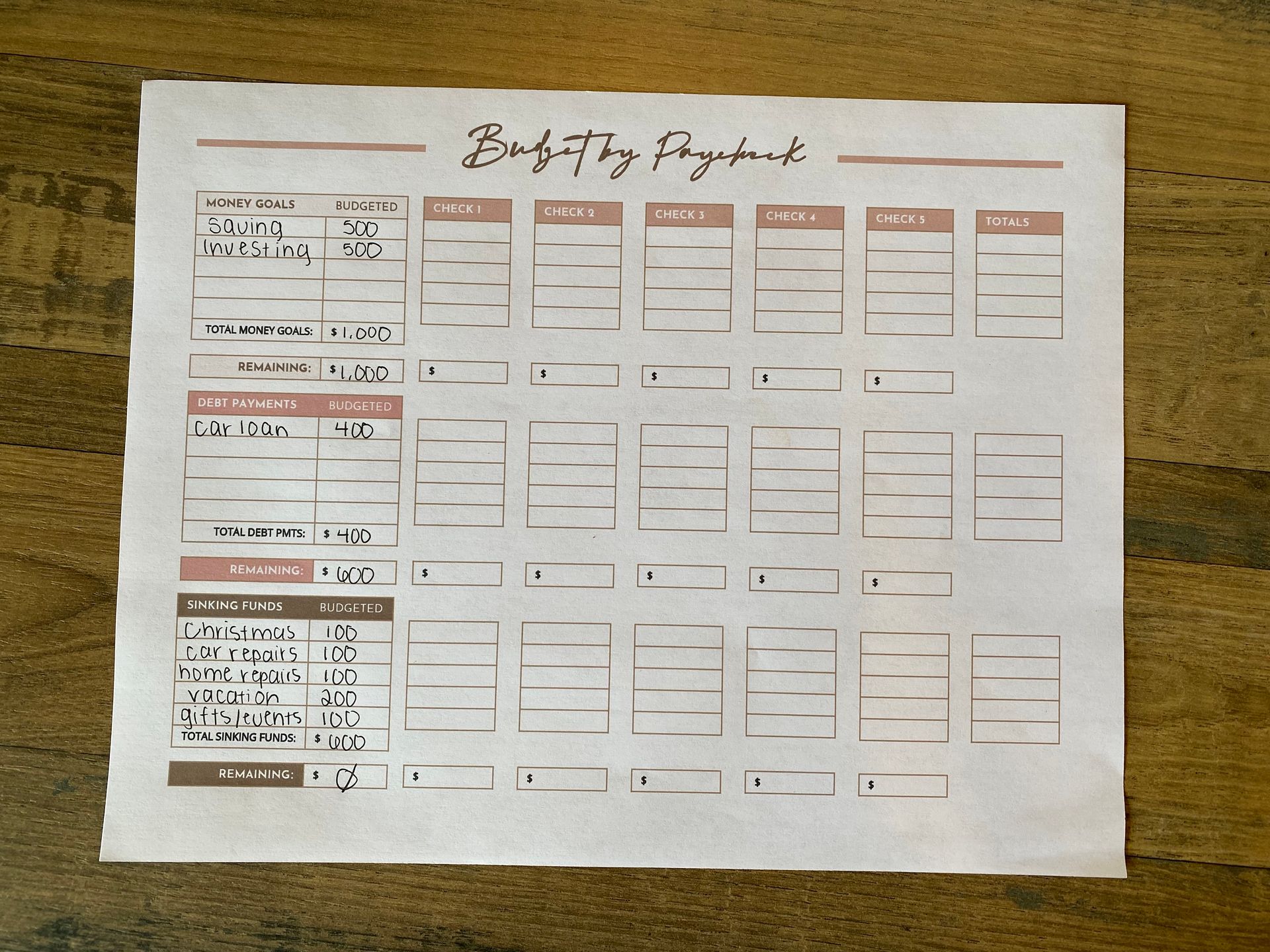

Update Google Sheets Budget for Month.

We have a google sheets template with a tab for each month of the year. On the left side of the spreadsheet all our monthly budget categories and expenses are listed out with their total monthly budgeted amount. Each of these expenses is then broken down into paychecks, with each paycheck having a column.

You can see the example below (this is an example,

not our personal budget numbers):

Assign Each Expense/Line Item to a Paycheck.

When we are paid (Fridays) I update the column for the actual paycheck number (which doesn’t usually change from budgeted since my husband is paid salary), and the actual expenses (or savings allotments) that will be made with that paycheck.

This is for cash-flow purposes, in addition to making the budget easier for me to stick to. I find that if I break our total grocery budget of $1,200 down into $600 out of 2 paychecks, I’m more likely to stick to it.

Update EveryDollar.

I put my Everydollar app and google sheets budget side by side, and carefully update each budget category to reflect my paycheck budget. For example, if my google sheets budget template has $500 from one paycheck to be allocated to groceries, I update the “groceries” balance in Everydollar to $500.

Adjust Sinking Fund Balances.

This refers to money that is “set aside” but that doesn’t actually physically leave our bank account at the time.

For example, we budget i.e. ‘set aside' money for vacation every month, but we don’t go on vacation every month. The money we set aside for vacation sits in our bank account.

Because of this, I keep and update the balances of these funds (properly called

sinking funds).

Reconcile Budget Balance to Bank Balance.

Back in the day, you would reconcile your check ledger to your bank statements. While I’m glad we can login and instantly see our checking account balances, this lost skill generally encourages us to be lazy with our finances.

Instead of budgeting, we simply check our bank balance, do a little estimating, and figure we can spend money on xyz purchase. The thoughtful planning and mechanics of reconciling and seeing what actually went out of our bank account removes us from our finances in a way.

I still reconcile our budget balance to our bank balance. In theory, the sum of what I have “left” for each budget category for the month or pay period + sinking fund balances (if kept in our checking account) should equal our bank balance. So I try to tie these numbers together to ensure I’m not missing any pieces. Obviously, since I have an app that automatically pulls in transactions, nothing should be missed!

One Income Family Budget Template

I made a simple paycheck budget template because I needed something that matched real life: one income, kids, groceries, bills, sinking funds, and those little expenses that always seem to pop up.

You can grab this one-page pdf budget template and start budgeting your next paycheck before it hits your bank account.

Our One-Income Family Budget Categories

To give you a better look into our household, here are the specific budget categories we utilize as a one-income family of six.

When we talk about fixed expenses, we are referring to those baseline costs that remain consistent every single month.

Variable expenses, on the other hand, are the items that fluctuate based on our usage or other seasonal factors.

It is important to remember that while variable costs naturally shift, I actually choose to treat them as fixed. By setting a strict maximum ceiling for these categories, I ensure our spending never exceeds the limit I have established for the month.

Sinking funds are current, but they do change based on the season our family is in. If I identify a (larger) future expense that we need to save for, I add a sinking fund. Some past examples of sinking funds include: a new car fund, furnishing our rental, new bunks for the kids, etc.

Our investing is an automatic paycheck deduction. We currently are not doing any additional saving every month for our emergency fund, but anytime we use funds from our emergency fund I pause our investing to get our savings back up to what it was before.

| Fixed | Variable | Sinking Funds | Savings |

|---|---|---|---|

| Giving/Tithes | Groceries | Annual car insurance | Emergency fund |

| Phone | Gas | Annual life insurance | Investing |

| Kids supplies | Restaurants | Kids activities | |

| Subscriptions | Household | Kids supplies | |

| Miscellaneous | Gifts (birthdays, weddings, etc) | ||

| Kids supplies | Car repairs | ||

| Personal spending | Christmas / holidays | ||

| Homeschool curriculum | |||

| Vacation | |||

| Vehicle registrations |

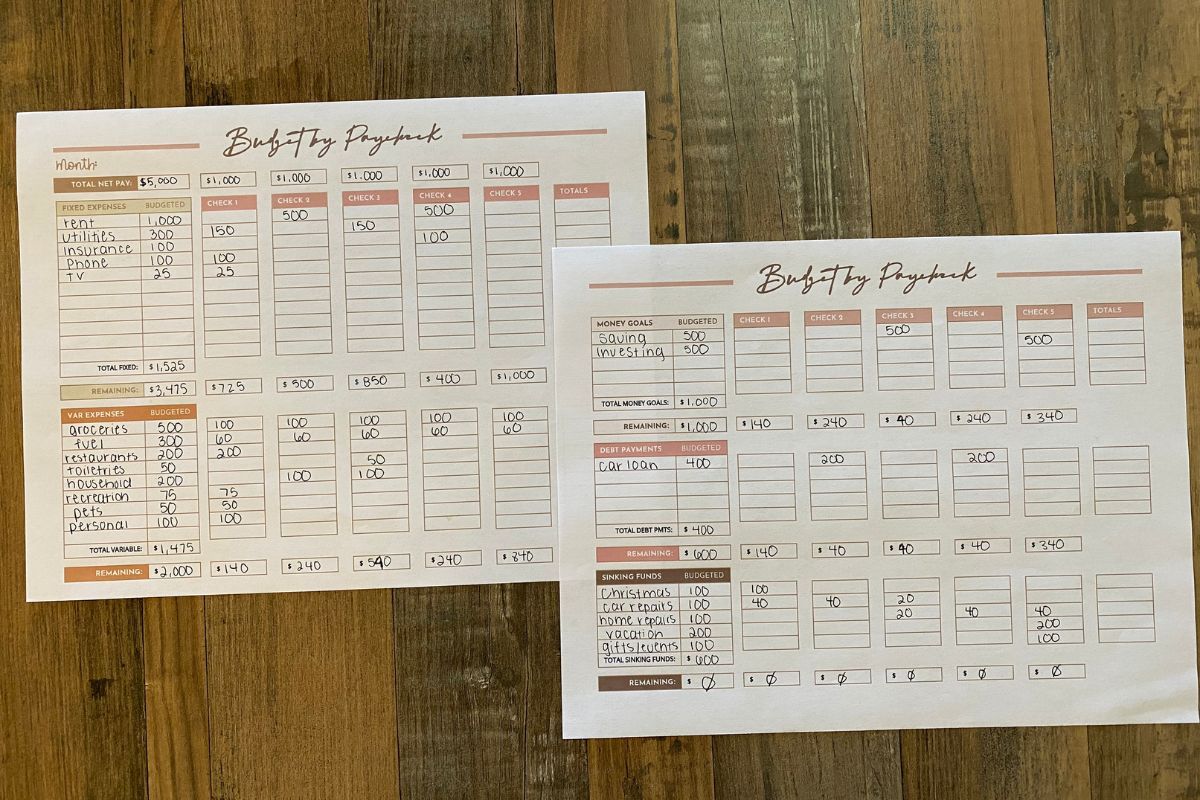

Example Paycheck Budget for a One-Income Family

This is paragraph text. Click it or hit the Manage Text button to change the font, color, size, format, and more. To set up site-wide paragraph and title styles, go to Site Theme.

How We Handle Sinking Funds So We Don’t Go Back Into Debt

One budgeting pitfall is the temptation to think that it doesn’t work because there are always unexpected, unplanned expenses that come up and blow the budget.

The temptation then is to throw budgeting out the window and say that it doesn’t work and there’s no point.

Instead of being frustrated by these expenses, which seem to come in large waves when you have a big family, plan for them using sinking funds.

A sinking fund is simply a strategic way to plan for future, known or unknown expenses by setting aside a little bit of money every month.

By putting these various funds in your budget, you’re playing offense rather than defense. I’ve been there– constantly feeling like we’re playing defense with our money. Once you set up sinking funds, you start playing offense instead.

Read in detail how to set up sinking funds in your family budget here.

Here is a list of our (current)

sinking funds:

- Vacation

- Christmas / Holidays

- Medical expenses (HSA)

- Annual dues/fees (insurance premiums)

- Gifts

- Car repairs

- Kids clothing / supplies

- Kids activities

- Homeschool curriculum

It brings so much peace to know when Christmas comes I don’t have to figure out what we have to “give up” to pay for gifts.

The money is already there. This makes it more enjoyable to shop for gifts, because you’re not stressed about the funds needed to purchase them. You’ve done the work, now you can spend without guilt.

Trust me, this makes it a lot more fun!

What to Do When the Paycheck Isn’t Enough (Or You're Just Frustrated)

Before I begin this section, I want to point out that many one-income families don’t even realize they are in a deficit every month, because of the use of credit cards.

The danger of credit cards and the ability to pay later is you can end up using credit cards to bridge the gap between income and expenses every month without even realizing it.

So, first, one-income families must have a budget plan in place to determine whether they are in the positive or negative every month. Remember, don’t rely on estimation for these numbers. Use real data. Look at your bank statements from the past few months, make broad expense categories, and compute the average monthly amount for each category.

Then, put a budget together to determine if you’re in the green or red.

1. Cover Necessities.

Food, utilities, housing, and transportation need to be prioritized and covered with any income that comes in, before anything else.

2. Cut all extras.

Temporarily cut all extras from the budget. This is a very un-American way to live, but if you are truly spending more than you make this is a must! Cut subscriptions (hello Amazon Prime), dining out, entertainment, extra-curricular activities, non-essential clothing, extra trips that use gas, etc.

3. Start building a cushion.

The goal after covering necessities and cutting all non-necessities is to build a cushion. Give yourself breathing room. The next step will help you accomplish this.

4. Make a bare bones budget.

A bare bones budget will ensure you execute the plan instead of just thinking about the plan. Put it on paper, and hang it somewhere. You can keep it in google sheets as well for easy reference. The bare bones budget is your income - necessities. What’s leftover gets completely allocated to your emergency fund/savings account. It’s time to build a cushion!

5. Get rid of credit cards.

If you are using credit cards, get rid of them (at least temporarily). You have to break the habit of relying on them as a crutch to hobble along on until the next month comes. Once you’re free from credit cards, you will feel a heavy weight lifted off your shoulders knowing you can make it to the next paycheck/month without going into debt just to cover monthly expenses.

6. Start DIY'ing and cooking from scratch (if possible).

If you aren’t already, start making as much as you can at home. Obviously, your time and energy limitations need to be considered. There are certain seasons for creativity and resourcefulness in the kitchen (stretching every dollar), and other seasons that require paying more to get more time back (like when you have a newborn, a busy homeschool season, etc).

We’re currently in the middle of a DIY build. My husband goes straight from work to the building site, working until 10pm or later, while I have 4 kids (7 & under) at home with me all day, every day. I’m not doing as much from scratch. I’m in more of a “paying for convenience” season. Don’t stretch yourself beyond your ability.

7. Seek the Lord and his wisdom.

Seek the Lord for wisdom in taking control of your finances. This is the most important step, more important than anything I could ever advise. Stay in constant prayer, asking the Lord to give you wisdom in how to get hold of your finances and bless your decision to be a one-income family, faithfully raising your children at home. Look for the opportunities and blessings He provides!

Key Encouragements for One-Income Families

You will feel freedom once your simple, repeatable system is set up.

It doesn’t mean you won’t have any bumps in the road or tough financial seasons, but you can be as prepared as possible for them knowing that you’ve wisely planned your steps, in prayer, trusting the Lord with the outcome.

A season won't last forever.

You can do everything right, and still end up in a season of incredible tough financial hardship. In these times, it’s tempting to say “what’s even the point of budgeting and all the financial planning”, but remember, it won’t last forever. It might last a long time, but not forever.

This season could actually be a testing point of your faith, or chastisement for poor decision-making, which then teaches us (if we are trained by it) and makes us wiser for next time.

To give you a glimpse into our reality, our family faced a three-year stretch where we reached our $10,000 medical deductible every single year. It felt like an uphill battle that would never cease. We had so many other intentions for that $30,000, but each of those dreams had to be surrendered or put on the back burner for a later season.

Stick with it.

If you’ve never budgeted before, it may feel daunting, and you may be tempted to give it up completely after a few weeks (or days!). Trust the process. The growing pains you’re experiencing are

good, and they are part of learning a new skill. I know that budgeting is a skill that will bless your family in the long run if you stick with it.

Write your budget on paper.

There’s nothing better than paper and pencil. We have so many tools and resources at our fingertips, but when we physically write things down, on paper, we are more likely to stay committed. Before making your paycheck budget in google sheets, make your monthly budget on paper.

Share this post!

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.

Get my free financial goals worksheet to set and effortlessly track all your savings goals! Financial goals examples including short-term goals and long-term goals to create a well-rounded financial plan that works for you!