5 Key Financial Life Skills Millennials Need to Learn

melaniedj • 10 December 2018

The millennial generation is known for being diverse and highly-educated (probably OVER-educated), yet they seem to be clueless when it comes to basic financial knowledge.

How is it possible that will all that prestigious schooling they don’t know the first thing about paying off debt, investing, or balancing a checkbook?!

Actually, research has shown that the answer might be because millennials think they are going to inherit wealth and therefore they don’t need good financial skills.

Umm…. what?

I’ll be the first to say...

- That is the worst financial plan in history

- Learn how to freaking manage money

In my opinion, I think that a key reason most millennials lack basic financial skills is because of their inability to see the big picture. Saving money for retirement and living on a budget isn’t of interest to a generation that likes to live “in the moment” than plan for their financial future.

BASIC FINANCIAL LIFE SKILLS MILLENNIALS LACK

Skill #1: How to Balance a Checkbook / Track Your Spending

Even though technological progression has made it easier than ever before to track our finances, the millennial generation sadly has no idea how to track their finances.

They think that checking their bank balance and making sure there is still money in their account is good financial tracking, and most have absolutely no idea how to balance a checkbook.

You older generations might laugh, but it’s 100% true. I can’t tell you how many people tell me that they already track their finances. When I press for how they do so, I frequently get an answer similar to “well I check my bank balance often and make sure I have enough money until the next payday to pay my bills.”

This means you’re living in a financial rut of living paycheck to paycheck, it is in fact not even close to good financial tracking.

While it is true that most of us don’t use checks that often, I think we miss out on a key concept by swiping a card instead of writing a check. When you swipe card, a transaction instantly takes place. You can go online and check your account balance and see the transaction that just took place.

The bank does all the recordkeeping for you.

However, when you write a check, the person whom the check is written to may not deposit it right away. Therefore, a transaction does not immediately take place. When you check your bank balance, you have to make a mental note that you have an outstanding check that has not come out of your account yet. Consequently, your account balance is not your true balance.

This forces YOU to do the recordkeeping, and that is one thing many millennials lack today. The ability to keep track of their finances.

Keeping Track of Your Finances

In order to be financially successful, you have to live BELOW your means. If you want to be very financially successful, you have to live WELL below your means.

In order to do this, you have to have a financial plan (discussed later).

At the least, make sure that you have a system in place where you are able to track what comes in every month and what goes out every month in order to make sure that you are spending less than you make.

Skill #2: When to Tell Yourself No

How do you define affordability?

Do you think how much down and how much per month? Or, rather, do you think how much in total and can I pay that today?

I’m guessing you probably understand that if you make $50k a year you can’t afford a ferrari. However, our culture will have you believe that you can afford just about everything else! Too often we look to others to set our standard for affordability.

We might think “well so-and-so next door can afford a brand new tahoe and she is a stay-at-home mom, so since both my husband and I work we can AT LEAST afford a brand new Tahoe.” Instead of taking a true look at your finances, you base your financial decisions off of other people.

Then we use debt to get that brand new Tahoe. Why? Because we have been taught that we deserve it, and we can “AFFORD” the item if we can afford the monthly payment.

The truth is, you can ONLY afford what you can pay cash for RIGHT NOW .

Yes, I know they don’t teach that in school.

If we’re being honest, how well has what you were taught in school about money done for you thus far? Are you thousands of dollars in debt? Do you have an emergency fund? Are you aware of how much money you need to save now to sustain your lifestyle in retirement? Do you even know how much money you need for retirement?

Debt is not a Factor in Defining Affordability

If you have defined your ability to afford something in the terms of monthly payments, you need to throw that idea out the window and cling to a new idea.

Repeat after me: I can afford whatever I can pay CASH for.

Yes, that includes vehicles, furniture, vacations, and anything else you’re trying to justify financing (besides a house).

Debt is a product, not a tool.

If you have bought into the lie that debt is a tool, it is time to debunk that myth right now and break the habit of using debt.

Skill #3: A Financial Plan

Millennials know they need to save for retirement, but they see it as some far off future goal that doesn’t require action until twenty years down the road.

In high school we learn what the pythagorean theorem is, but we don’t learn how much money we need to save per month in order to retire with dignity.

No freaking wonder most millennials can’t balance a checkbook.

Now, I don’t think that not learning these things in school is a cop-out for not actually doing them. Your life is up to you . If you want to manage money better, save more, invest more, you have the tools available to you to do so.

Everything I know about personal finance I learned from someone else, not from sitting in a classroom eight hours a day.

According to a Bankrate survey, 61 percent of Americans don’t know how much money they’ll need to save for retirement, including nearly three-fifths of every adult generation over age 37. What is even worse? A Federal Reserve Report on Economic Well-Being of Households indicates that fewer than 2 in 5 non-retirees feel as if their retirement savings is on track.

For millennials specifically, 69% do not know how much money they will need in retirement to live.

Part of this is because retirement is some distant dream to most, so it’s hard to be self-disciplined right now in order to save and plan for something that won’t be a reality for 40 years.

However, not saving NOW is one of the most detrimental things you can do to your financial situation. If you think that it doesn’t matter right now and that you can save later, you don’t understand the power of compound interest.

We NEED to learn how to plan for our future.

Putting a Financial Plan in Place

Developing a personal financial plan does not have to be complicated.

Our outline of our financial plan is as follows (we follow Dave Ramsey’s baby steps, except we modified them to fit our financial goals):

-

Develop a Small Emergency Fund -

Pay off All Debt -

Save 3-6 Months of Expenses in an Emergency Fund - Invest 15% of Your Gross Pay *** WE ARE HERE ***

- Pay Off Your House Early

- Build Wealth & GIVE

Even though y’all might thing I know a thing or two about personal finance, I know that there are other people out there who know it BETTER than I do. For this reason, we have a financial advisor.

I don’t have the time to figure out what mutual funds are the best to invest in and manage our portfolio. So, I hired someone else to do it. Someone who we trust, and someone who takes the time to listen to our goals and ensure that we will be able to reach them or at least give us a path to reach them.

My job is to know how MUCH we can invest per month, and to make sure that the money is AVAILABLE to do so.

How do I make sure the money is there at the end of the month?

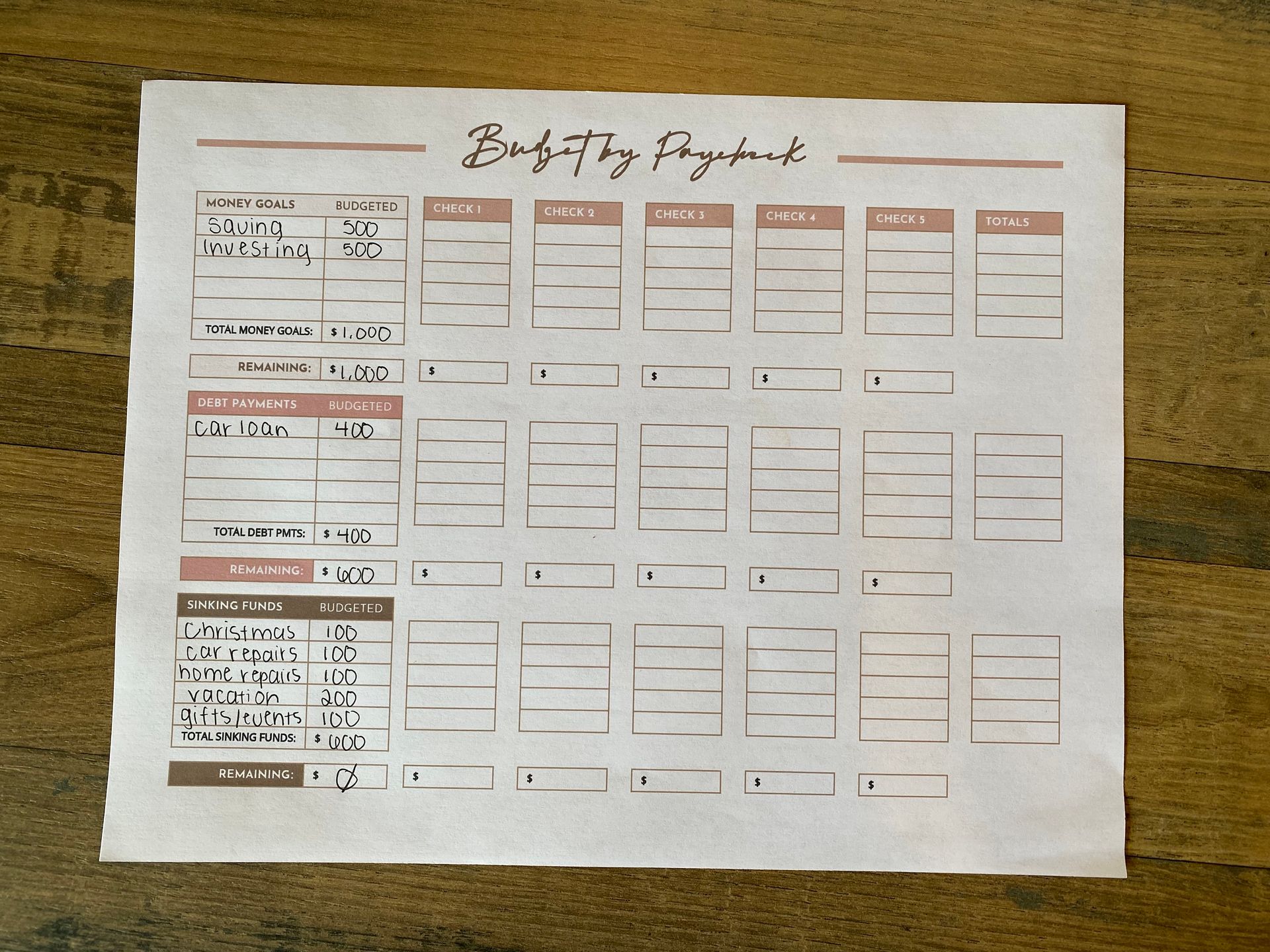

I plan every single dollar of our estimated income for the upcoming month on paper BEFORE the month begins, and then I use that piece of paper as a guide during the month.

In other words, I BUDGET.

BUDGETING

Building wealth and reaching financial goals is difficult if you don't know where your money is going every month. While a budget sounds restricting, it actually gives you freedom to spend your money without guilt!

We feel guilty when we spend money and we aren't really sure whether we should be or not, because we don't really have a good grip on our finances. But when we have a budget (a plan), and we know exactly how much is coming in and going out, we feel peace!

Get my free google sheets budget template by subscribing to my email list and getting exclusive content!

If you've never created a budget before, don't worry! You can make a monthly budget in 7 simple steps.

Skill #4: Accumulating Savings

Millennials are twice as likely to rack up debt than to accumulate savings.

Yes, you read that right. We are 2x as likely to go into debt rather than accumulate savings.

The sad truth is about half of millennials spend more on restaurant food in a year than they save for retirement.

Having a savings (this is separate from your investing) is your best protection against a financial disaster.

Developing an Emergency Fund

I call our savings account our emergency fund. I do this because that is exactly what it is for- an emergency. Otherwise, this account is not to be touched!

A savings account should only be used for things such as a period of unemployment, or financial hardships such as large unexpected medical bills, a car breakdown, etc. It should be used for necessities ONLY.

This is a financial cushion.

Skill #5: Delaying Gratification

It’s super trendy right now to spend a shit ton of money that you don’t have.

Millennials are buying their dream home as their first home. 53% of millennials would go into credit card debt to attend a wedding. Millennials are spending over $3,000 on an engagement ring.

The reason many millennials are broke is because they are making their financial choices out of order because they don’t understand or like the concept of delaying their gratification.

If you think you don’t fall into the broke category, because that’s for people who are going couch to couch, struggling to buy food, you have the wrong definition of broke. If your household debt is more than the cash and assets you have on hand, you are by definition, broke.

Statistics show that millennials spend more money than any other generation on conveniences like coffee, transportation, food services, and dining out.

The millennial generation is more likely to spend money on travel, dining, and fitness than to save for retirement.

Sacrifice Now

Pay the price today so that you can pay any price tomorrow.

I understand the desire to live while you’re young, travel, and “find yourself.” However, to what extent and for what price? The price of your financial future?

If you find a purpose in your job and enjoy it, then it’s easier to delay your gratification and save your travel plans for the future when you can ACTUALLY afford it.

On a final note

The lack of basic financial knowledge amongst the younger generations is concerning.

Considering you can graduate high school without knowing how to balance a checkbook, create a simple budget, or understand the power of compound interest, it really should not come as a surprise.

However, now more than ever before there are resources available to anyone who wishes to better their financial situation (including my blog for starters)!

The five key financial life skills I’ve discussed above are vital to your financial success.

Don’t let your children grow up without learning them, and don’t skate through life without knowing them.

Until next time!

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.