Budgeting for a Baby: Essential Financial Planning Tips

melaniedj • 6 September 2019

Expecting and raising children is one of life's greatest joys, as well as one of life's most humbling and rewarding experiences. Becoming new parents stretches us in ways we can't understand prior to having a new baby, allowing seemingly endless opportunities for sanctification, as well as endless opportunities for thanksgiving and praise to the Lord!

In many ways, we can't prepare for this tremendous blessing in our life. However, there are a few things we can do to prepare, not excluding having a proper baby budget.

According to to the U.S. Department of Agriculture , the average total cost of raising a child from birth to age 17 is $233,610 for the average income couple with two children.

That number will fluctuate a little depending on where you live, how much gov. assistance you get, etc., but one thing is clear- it will cost you!

While many people will ask you if you've got your nursery together, how many diapers you have, etc., one of the most important ways new moms can plan is to get their personal finances in good order.

HOW TO PROPERLY FINANCIALLY PLAN FOR A BABY

A baby is a blessing no matter your financial situation, and raising children gives us a unique opportunity to trust the Lord for His provision-- financially, physically, mentally, emotionally. He gives us what we need; when we need it.

If you find yourself unable to do any of the following steps, don't give way to fear! Pray, seeking wisdom with your finances, asking the Lord to reveal to you ways you can improve your financial situation and have more stability.

Let's go through the process of financial planning for a baby so you are prepared for whatever comes your way!

1. Fully fund an emergency fund

The first order of business is to have 6-12 months of household expenses in an emergency fund. An emergency fund is simply money that you set aside for unexpected costs.

A roof that needs to be replaced, an AC unit that breaks down, a car that needs fixing, etc.

How much you need is dependent on how stable your income is. One one hand, if you are a one income household or self employed, I'd recommend 10-12 months. On the other hand, if you are a two income household with steady jobs, 6 months is probably fine!

If you are having trouble finding ways to save money and beef up your emergency fund before baby comes, these are expenses we cut to save $13k every single year.

Download one of my

free savings plans for a strategic, fun way to stay focused on your savings goal!

2. Save enough to cover your deductible / out-of-pocket max

It's no secret that medical expenses are burdensome for many people. Hopefully I'm not the only mom who goes through a decision making process before bringing my child to the doctor or E.R. because well... I'm sick of medical bills.

Medical bills are the gift that keeps on giving... once you think you're done, there's always a few stragglers!

There's probably a 99% chance that you will meet your deductible for the year once you give birth. Additionally, note that your deductible will not just be the deductible for you, it will be the family deductible.

Depending on your insurance coverage--whether you have a high-deductible or low-deductible health insurance plan--- you might need to save quit a bit of money. Additionally, how long your hospital stay ends up being, the type of health care you receive (hospital vs. midwife), and your zip code (rural vs. city hospital) will also factor into the final cost.

I recommend saving your out of pocket maximum- not just your deductible - in addition to your 3-6 month emergency fund for maximum financial preparedness.

Your out of pocket max refers to the amount you are responsible for above and beyond your deductible. This is typically a percentage of costs above and beyond your deductible that you are responsible for. See blow for a detailed example.

Example

EXAMPLE: Your deductible is $5,000, your out of pocket maximum is $8,000, and your coinsurance percent is 20%. If total hospital bills amount to $13,000, you'll actually be responsible to pay $6,600.

$6,400 = $5,000 deductible + [20% x $8,000 [13,000 total costs - 5,000 deductible]].

Continuing the example, if you're hospital bills are more than $13,000, you will pay more than $6,600, but only up to $8,000.

If you can't afford to save your out of pocket maximum, at least save your deductible, that's a great start!

Depending on your household income, you may qualify for financial assistance from your healthcare provider. Many offer discounts, payments plans, etc.

HSA Plans

If you have a high deductible health insurance policy, you can contribute money pre-tax to your HSA (health savings account). A health insurance plan is considered high deductible if the individual deductible is $1,600 or higher and $3,200 or higher for families.

Using an HSA is a great way to save for out of pocket medical expenses, including some of the big one-time costs.

When choosing health insurance plans, not only do you need to consider the difference in premiums for a low deductible vs. high deductible plan, but also the tax savings associated with a high-deductible plan. Depending on what tax bracket you fall into, this could be significant savings.

3. Figure out how long of maternity leave you can afford

Can you save money for maternity leave in addition to covering your deductible and funding your 3-6 month emergency fund? Analyze your income and expenses and determine how long you can go without a paycheck for, which will be dependent on how much money you have saved!

Here's how to figure out how much you need to save:

(monthly take home pay x months of maternity leave desired) / months left to save

For example, say you take home $3,500 per month but only need $2,000 of your paycheck to cover your bills. You have 8 months left before your due date and you want to take a 3 month maternity leave. To calculate how much you need to save for maternity leave:

($2,000 x 3 months) / 8 months = $750 a month you need to save

Note I used $2,000 because that is the amount needed to cover necessities, which is all you need to cover during this time.

4. Save for maternity leave

Once you figure out how much you need to save per month, it's time to get aggressive and save. You want to get this done as fast as possible; get aggressive and stick to a tight budget! Find a way to make some extra money in addition to your day job. Sell stuff, cut expenses out, pick up a few extra shifts. Keep track of your savings as you go!

5. Start budgeting for additional expenses

Now it's time to figure out how much you need to budget for your new budget category every month- BABY! You won't know the actual costs until baby is here, but you can give your best guess/estimate and adjust later

SUPPLIES

Baby expenses/supplies should be a separate line item in your monthly budget.

This is a non-exhaustive list of some things you may need:

- Disposable diapers / cloth diapers

- Wipes

- Changing table

- Diaper bag

- Baby clothes

- Nursing bra/clothes

- Burp cloths

- Diaper rash cream

- White noise machine

- Swaddles

- Bath/tub

- Pacifiers

- Thermometer

- High chair (not needed immediately)

Hopefully you'll get many of these items gifted to you or second hand. It's likely that the biggest costs you'll have on a monthly basis are diapers and wipes.

BIG-TICKET ITEMS

If this is your first baby, you may have a few of the big-ticket items purchased for you and given to you at your baby shower. The following baby items can run on the expensive side, and it is a good idea to save up for them sooner rather than later:

- Infant car seat

- Baby monitor

- Quality crib

- Durable stroller

- Breast pump*

- Rocking chair

- Baby carrier (depending on quality)

* Your insurance provider is required under the Affordable Care Act to cover the cost of a breast pump. However, some require a prescription from your provider in order to take advantage of this benefit. Additionally, every insurance company has different stipulations, so be sure to go to their website and read before purchasing a new pump!

Having had 3 kids in 3 years, I've learned to focus on value over price. Obviously, we all have a maximum budget we can spend even if we want to buy the best value, it might not be an option with our budget. I aim to make my big-ticket items one-time purchases.

I've purchased items on the cheap end, just to have to replace them after a year because they wore out so fast. If it's in the budget, it's worth it to buy the higher quality, more expensive baby gear.

CHILDCARE

Daycare is one of the major expenses you'll have to budget for if you plan on returning to work after having your baby. Be sure to include this in your newly updated budget!

Also evaluate how much you'll actually be taking home and making per hour after paying for childcare costs. According to Baby Center, while costs vary widely depending on location, type of care, etc., you can expect costs to be on average $1,000-$1,200 per month.

CHECKUPS

Do you need to budget separately for routine checkups and/or other medical costs?

Since we have a high deductible HSA plan, we pay anywhere from $200-$300 per doctor visit. We contribute to our HSA every month to make sure this is covered!

INSURANCE PREMIUMS

Chances are your insurance premiums are going to go up if you're a first-time parent. This is a great time to look into all your options for insurance and re-evaluate.

You may want to consider changing plans (a child is a qualifying event meaning you can change your plan without waiting for open enrollment).

Would it work best for your entire family to be on one plan? What if the baby and your spouse are on their own?

The most important things to consider are your deductible and your premiums. Sometimes one plan might seem better than another, but the premiums are so high that you pay more in premiums than the deductible of the other option.

Confusing, I know! My point is take time to look into your insurance options!

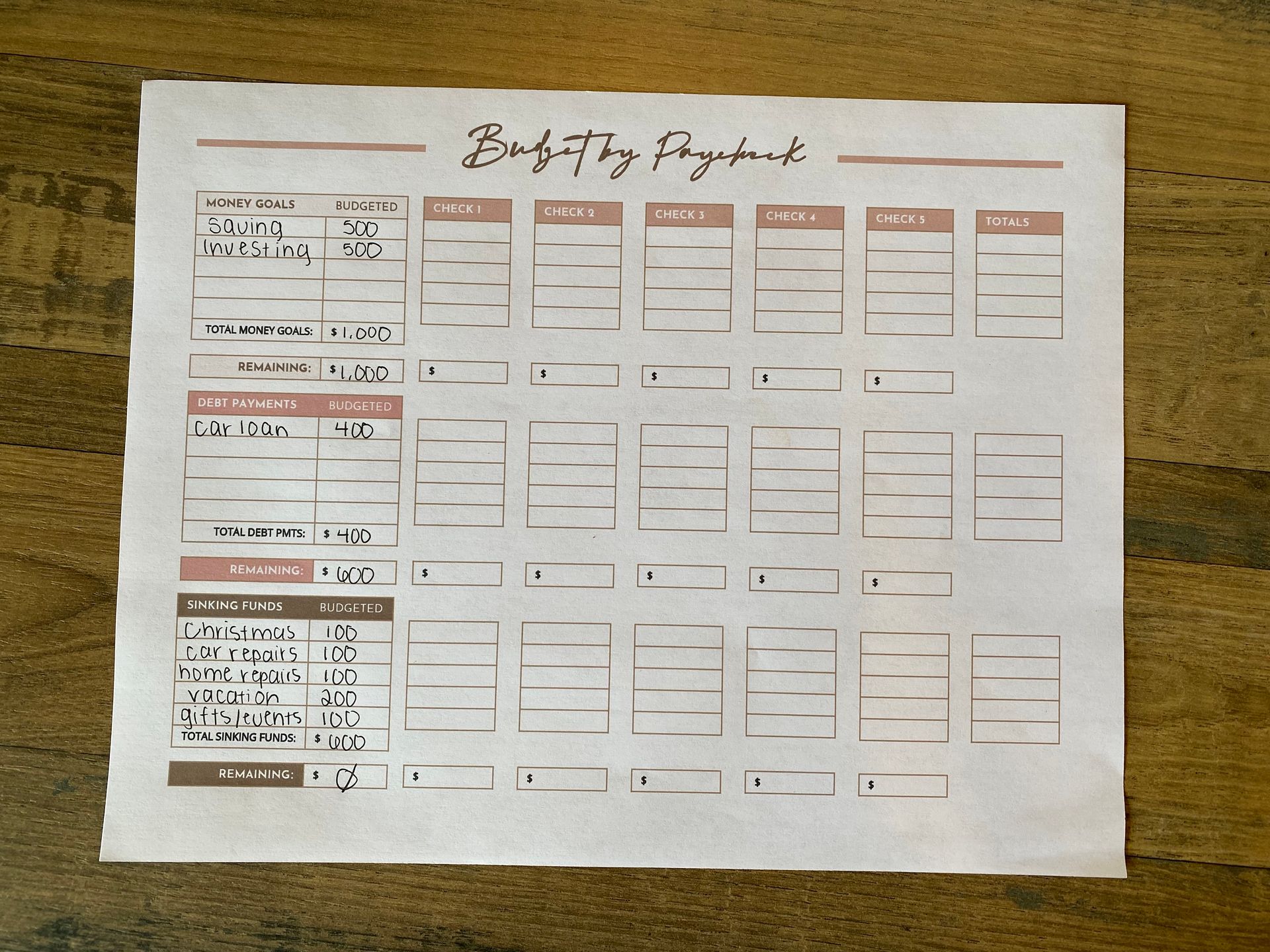

6. Have regular budget checkups

Keep track of your progress and do regular budget check ins to make sure you are hitting your savings goals.

I'll say this again, if you aren't on a budget now, you need to be.

I highly recommend having a written monthly budget.

If you don't write it out, chances are you won't ever look at it, stick to it, or track it.

7. Relax

Talking about money can be extremely anxiety inducing, especially if you're looking at my steps outlined above thinking there's no way I can do that.

I would encourage you to relax and know that no matter what, it will work out! There's help available if you are struggling financially and my steps outlined above aren't meant to induce anxiety but rather give you peace. Remember that!

OTHER PLANNING POINTERS

When You're in Debt

If you're in debt and working on your debt snowball, I recommend pausing your snowball until after baby is born.

Any extra money you were throwing at your debt should now instead be used to beef up your emergency fund and maternity leave savings.

You need to save up as much as you can. Once everyone is home and healthy, you can resume your debt snowball!

If you need assistance

If you know that with your income you will not be able to cover your deductible, talk to your hospital about getting financial assistance.

Most hospitals and medical centers offer a discount or will reduce your bill if you can show proof of income/hardship.

Or, if you haven't made good financial choices up to this point and have a higher income but no savings, you might quality for an interest-free payment plan.

Cost savings on baby supplies

There are many ways to save money on baby supplies.

Here are some quick tips to save on baby supplies:

- Sign up for free formula samples. If you're formula feeding, sign up for free samples from all the formula companies you can! This way when trying out different formulas, you don't have to buy a whole can and risk wasting it.

- Create a baby registry on Amazon for 20% off. For a certain period of time, if you buy on Amazon, you'll get 20% off everything on your registry. I loaded my registry with things so that I would get the 20% discount.

- Try different diapers and formulas until you find a generic brand that works. While the first store brand you try might not work great, keep trying! I've found that Sam's Club and Costco's Kirkland diapers are great quality. Check their websites often to find the best deals on diapers.

- Make your own baby food. Instead of buying a jar at the store, buy fruit/veggies and blend it yourself!

- Search facebook marketplace for deals on gently used baby items. This is a great option if you live in or near a big city, because it increases the likelihood you'll find a high quality, high-dollar item that is gently used at a steep discount!

- If you're a regular thrift store junkie, keep an eye out for baby supplies. Many times, families that are coming out of the baby stage will donate a big chunk of it just to get it out of their storage. This is an easy way to save a lot of money; you can often get these items at half the cost of brand new.

Keep in mind that baby's first year is relatively inexpensive compared to the total cost of raising a child.

Staying home after baby

In deciding whether to stay home or not after baby, follow this step by step process to help you analyze if you're able to live on one income. When our son was about 9 months old and we found out we were pregnant with our second child, we decided that we wanted me to stay home. So my husband and I sat down together to make a mock budget. If you want to stay home but you're not sure if you can do it, you need to create a budget. It's very important that you live on a budget and both you and your spouse are committed to sticking to it!

Most Importantly...

It's great to financially plan for a baby, but don't let the stress take away from the joy of being an expectant mother! Yes, babies can be expensive and that can cause stress. But as someone who has stressed over the cost of having children, I wish I had spent less time worrying and trusted the Lord's providence.

Instead of seeing a child as a financial burden, pray that the Lord would give you a biblical perspective on children. They are a blessing and an inheritance according to Scripture, and so we should rejoice anytime He blesses us with a child!

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.