Money Myths Broke People Believe

melaniedj • 18 December 2017

According to Dictionary.com, the definition of myth is a widely held but false belief or idea. I would argue that the most common beliefs about money in our culture today are actually money myths.

Get a credit card, it shows you're responsible.

You deserve a new car, even if you finance it.

Student loan debt is inevitable.

These are all MYTHS.

In order to pursue financial freedom, you have to change your way of thinking about money.

Nothing I say is any sort of prosperity gospel or mystical/magical ways of handling money. It is common sense, which is hard to come by, especially in the financial realm!

Don't fall for these common money myths are preached as normal. Normal is BROKE.

Homes

1) A House is Your Biggest Asset

I cringe when I hear people say this.

This is a classic excuse for not saving and investing money. Your house increasing in value is not an excuse to not save for retirement!

Sorry, but your house value will not sustain you into retirement.

What if the housing market crashes again? What if the area you live in becomes less desirable?

There are so many unknowns surrounding the housing market. If your house has increased in value that's great, but don't depend on it for financial security.

2) If You're Married, You Need a House NOW

When Joe and I had only been married one year, we had plenty of people barking in our ear about how we need to find a house AS SOON AS POSSIBLE.

After all, we've been married a whole 10 MINUTES .

Buying a home should not be an age or marital status thing.

The only time you should buy a home is when you are financially ready.

We JUST bought a house, and I have rented my current apartment for two years now.

Renting has allowed us to pay off debt and save for a house.

3) Renting Is A Waste of Money

MYTH.

How many times have you heard someone say that renting is stupid because that monthly rent payment could be going towards a house (an investment), but instead it's cash out the window?

While it's true that the cash isn't going towards anything, having cheap rent allows you to save money and prioritize your spending.

Cars

4) Old Cars Are Not Safe

Classic. The "I need a new car because it's safer" excuse.

In other words "it's all for the kids."

Let's not kid ourselves (no pun intended), it's all about me, me, me.

Now of course if you have a car that has major mechanical issues, that's a different story. However, if that is the case, save up some cash and buy a new-to-me car!

5) A Car Is An Investment

A car is NEVER an investment.

New cars lose 60% of their value in 5 years.

You wouldn't drive down the road throwing hundred dollar bills out the window, would you? That's what buying a new car is like, you just don't feel the pain because you aren't physically throwing bills out the window.

In my opinion, the new car smell isn't worth it unless I can cash-flow the car without my bank account even wincing.

This is why we will buy used for most of our life. If you buy used, the original owner has already taken most of the depreciation on the car.

For the most part, the best deals on cars come from people who are looking to get rid of their car fast.

6) Car Payments are a Part of Life

This is the normal way of thinking in our culture. Unfortunately, normal is broke.

Statistics show that the average buyer signs up for a six year loan at an average interest rate of 9.6%. In 2017, the average car payment for a new car was a whopping $479.

I see a major problem here considering statistics also show that OVER HALF of Americans are living paycheck to paycheck!

Consider this scenario. You buy a car for a total purchase price of $25,000. You put $5,000 cash down, so your total loan is $20,000.

Using the AVERAGE from above (9.6% interest and loan period of six years), your monthly payment will be $458 and you will pay about $4,700 in interest. So, the total cost of the vehicle will be $29,700, and after you finally pay it off, it will only be worth $15,000 max!

OUCH.

Family

7) We Can't Afford Kids

Call me crazy, but I actually think having kids causes you to be more selfless and conscious of how you are spending your money.

It's not all about you anymore, and that forces you to re-evaluate your finances and priorities.

While it is true that kids are expensive, the Bible says that kids are a blessing.

I think it's important to ALWAYS trust that God will provide.

My parents had four kids by the time they were 27, and my mom was a stay-at-home mom and my dad a dairy farmer. When I ask my mom how she did it she will say it wasn't always easy, but God always provides.

I don't have kids yet, but that's my two cents.

8) You and Your Spouse Should Have Separate Accounts

In my opinion, it is not wise to have separate bank accounts.

How can you make sure you are on the same page and have the same goals in mind if you can't even combine your checking accounts?

Additionally, it can create trust issues about regarding how the other person is spending their money.

Transparency is key in this situation, and what better way to go about it than combining your accounts? If you fail to do so, it can create trouble that could be easily avoided. Considering 50% of modern marriages fail and the most cited reason is money issues, why wouldn't you put this safeguard in place?

Related:

9) He/She is a Saver/Spender & They Need to Be More Like Me

Oh boy did this take me a long time to learn.

I'm a saver, Joe is a spender.

Early in our marriage, I thought that he needed to change and think more like me. The more I nagged and pressured him, the more he would push back.

I finally (thankfully) realized that it is OKAY that he is a spender. As long as we agree on the same goals and how we will get there, I can handle it if he splurges here and there (as long as your splurging isn't getting in the way of you paying off debt or saving/investing).

Retirement

10) I Can Depend On Social Security

Breaking News: The government is not going to be your white horse.

In case you haven't noticed, the government isn't known for it's ability to handle money.

There is only one reliable source of income for retirement- your personal savings and investments. Especially considering there is no clear path to fixing social security (besides cutting benefits or increasing taxes), those who are banking on it for their retirement could be greatly disappointed.

Related:

11) I Can Worry About it Later

You can't afford to worry about it later.

The only time I would suggest temporarily stopping investing would be if you are paying down debt (except your home mortgage). Get the debt paid off fast, then start investing again.

Don't put it off.

You'll thank yourself later!

12) My 401k & House Will Be Sufficient

Simply saving having a retirement plan where your employer matches contributions will not be enough to sustain you into retirement either.

Don't get me wrong, you should take advantage of the retirement plan your work offers, and a great way to start is to invest in a ROTH IRA. I like the ROTH IRA because the money grows tax-free and your withdrawals are tax-free.

However, just a retirement account is not enough. Be sure to diversify your portfolio, I would suggest talking to an adviser and investing in mutual funds.

Related:

Beliefs

13) Debt is a Tool

The average amount of credit card debt per household is $10,555. The most cited reason for having this type of debt was overspending on unnecessary purchases, BEATING OUT medical expenses and household necessities.

So, despite what a lot of people tell you- that it's good to have a credit card for "emergencies"- statistics show that just about anything qualifies as an emergency ( here are some major reasons you shouldn't have a credit card).

Debt is not a tool to be our saving grace in times of trouble. The Bible warns us that the borrower is slave to the lender.

Debt should be avoided at all costs!

Related:

14) I Can Never Get Ahead

As Dave Ramsey says, poor is an attitude. Broke is just somewhere you are passing through.

I think a lot of people are misled about what broke actually means, they instantly think of someone who struggles to put food on the table, struggles to buy necessities, etc. However, someone can be broke and very easily be able to do all the things mentioned above.

If you have a ton of debt, you are broke, and you need to pay it off as fast as you can (see how to attack debt with intensity).Once this is done, you will have room to save and invest.

If you disciplined in your saving and investing, YOU CAN GET AHEAD.

15) I Can't Afford to Give

When you choose to handle money God's way, difficult things become easier.

You become a cheerful giver both in the good times, AND the bad.

I've been asked a few times if you should continue to tithe when you are focusing on paying off debt. My answer would be yes. Giving softens our hearts and helps us release the urge to depend on money and let it control our life.

Even when we were on a tight, tight budget, we still tithed faithfully. You'd be surprised how God blesses you in other ways that allows you to save, invest, or pay off debt quicker.

Related: Giving Until it Hurts

Always be cheerful in your giving. If you can't manage a little bit of money, God sure won't let you manage a lot.

Share this post!

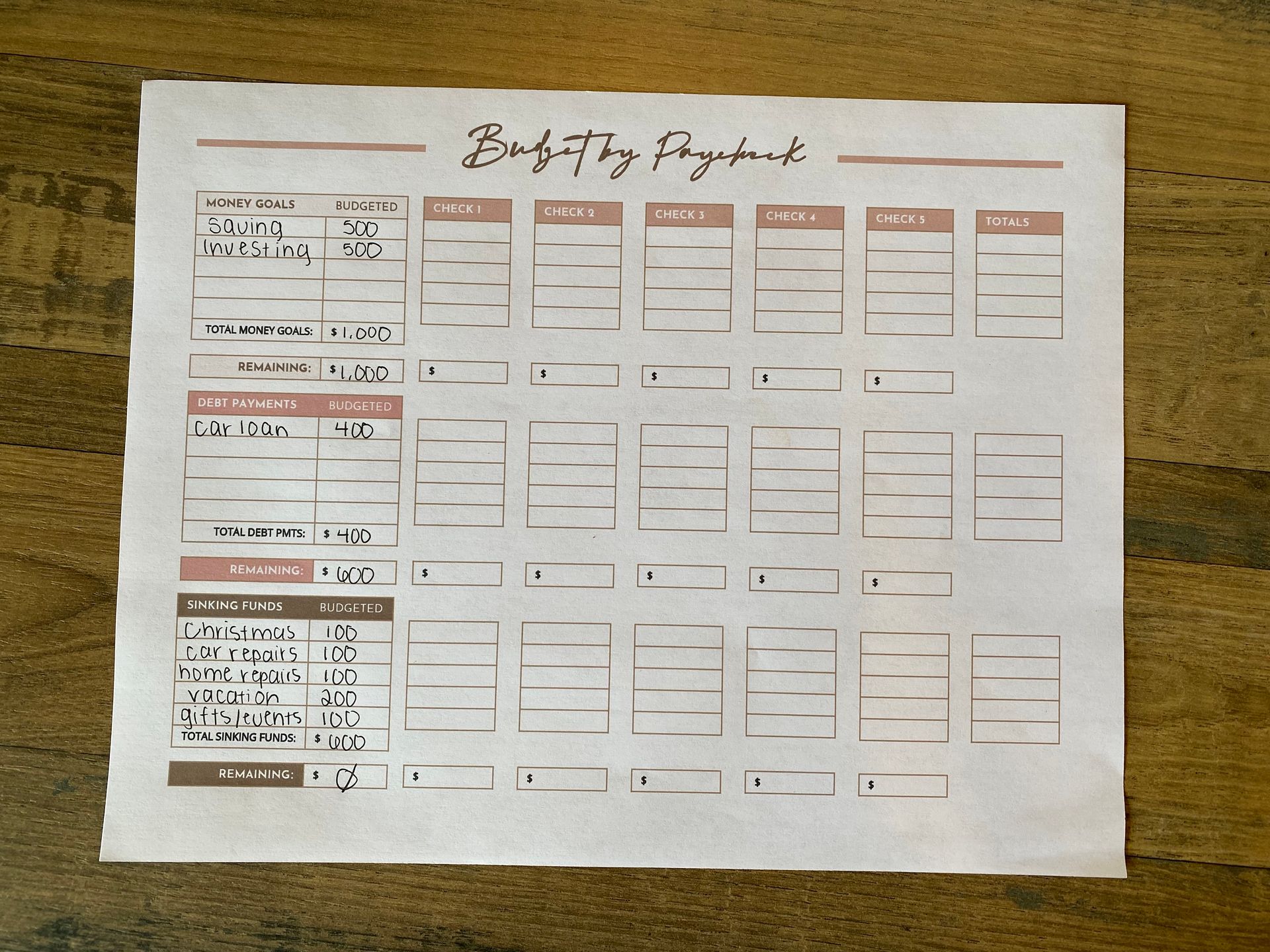

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.