31 Simple Money Management Tips Successful People Always Follow

melaniedj • 3 November 2020

At the end of the year, we start to think about our habits, including our money management habits. If you're reading this and thinking next year you need to start doing things better, I'd challenge you to keep reading and start today .

I'm not one for New Years resolutions because I believe when things matter to us we take immediate action.

In other words, if you don't have a good enough reason to motivate yourself to start today, you won't in January either.

As we approach the end of the year, now is a good time to reflect, evaluate, and make change.

MONEY MANAGEMENT TIPS FOR THIS YEAR

These are some of the top money management tips I think everyone should know!

BUDGETING

BUDGETING

1) Get a grip on where your money is going.

First things first, to manage your money better you must know where it is going.

If you do not currently track your spending, this will require a little bit of work. Here is how to evaluate your spending:

- Download & print your last 3-6 months of bank statements.

- Create general expense categories, such as utilities, mortgage, groceries, dining out, entertainment, daycare, fuel, etc.

- Assign every single dollar spent in the last 3-6 months to a category (do each month separately).

- Compute the average amount spent on each category.

- Evaluate.

Are you surprised by your spending? What categories can you trim down?

2) Income- Expenses must be positive. You cannot run your home at a deficit.

Is your total spending in any of the months you evaluated more than your total monthly income? If so, you need to make some changes. You cannot live spending more than you make. It will lead to financial ruin.

3) Plan your spending using a budget to avoid money stress.

A budget is your best defense against overspending. When we plan everything on paper before the month begins, we can spend with confidence, knowing we've done our due diligence.

4) Your budget should be a zero-dollar budget.

After subtracting budgeted income from budgeted expenses, your bottom line should total zero. Every single dollar you plan to receive should be assigned before the month begins.

5) If married, your spouse needs to agree on the budget.

If you are married, it is crucial that you and your spouse agree on how your money should be spent.

Money problems are the number one cause of divorce. If you have a reluctant spouse, change your approach. When we first started getting our finances together, I did not approach my spouse the right way. Your approach matters.

Once you get on the same page, it is important that you:

- Budget together

- Talk about money often

- Establish goals together

- Work towards your goals together

❤️ Related posts:

6) Try to get one month ahead on all your bills.

Imagine being one month ahead on all your bills! This doesn’t mean you pay them early. Rather, this means you always have one months' worth of expenses cushion in your checking account. You always pay your current months bills with last month's income.

7) Budget from your priorities.

Create your budget based on your priorities. This will look different for everyone. Your unique budget will not look the same as anyone else's, because you have different priorities. Budgeting this way takes away the guilt of spending because every dollar is not only planned, but it’s ordered based on what is most important to you.

For example, let’s say you have $800 until you get paid next. Your financial obligations until then include daycare ($250), groceries ($50), utilities ($200), car insurance ($100), and your credit card bill ($325). You also need new tires soon ($500). You know that you won’t be able to cover all these obligations with $800. So, what do you do?

You plan your spending based on the cash you have today in a way that reflects your priorities.

Here is how it might look:

- Priority #1: Groceries for $50. Your family needs to eat. This is the top priority. If you’re frugal, you can feed them for a week or a little more on $50.

- Priority #2: Utilities for $200. The lights need to stay on. You need running water. While you don’t need this to survive, it’s the next priority.

- Priority #3: Daycare for $250. For you and your spouse to provide, your kids need to be safely cared for. This is the next priority.

- Priority #4: Car insurance for $100. Though your insurance company might still cover your vehicle if you’re behind a month or two, it’s a good idea to stay current. If you hit someone without insurance, you’re in legal & financial trouble.

- Priority #5: Pay $200 on your credit card bill. Though you won’t cover the whole bill, food, shelter, transportation, and childcare take priority over debt payments.

This is how you would distribute your money based on your priorities. When people realize they don’t have enough cash to cover their financial obligations, they panic. Instead, plan based on your priorities.

Do this until you get current on everything, and then create a new plan for your new cashflow, goals, and priorities.

8) Have a miscellaneous budget category, but do not abuse it.

Inevitably, there will be expenses every month you don’t plan for. Am I the only one who constantly forgets about weddings, birthdays, and baby showers ? While budgeting will hopefully mitigate many of these surprises, a miscellaneous category should be in the budget to cover unplanned expenses.

9) Make sure there is a “fun money” category.

Whether your debt free or in debt up to your eyeballs, you need to have a fun money budget category. The amount you budget will differ depending on which situation you’re in, but there is a need for it in both situations.

When we deprive ourselves, we often end up binge spending and blowing the budget! Then we feel intense guilt and buyer's remorse and are tempted to throw the towel in on the whole budget thing.

Plan against this temptation, have a fun money or blow money budget category. Use this category to spend money on whatever you’d like without guilt.

The fun money budget category is especially important if you’re married. Have a separate fun money category for each of you that can be spent on whatever you’d like.

One rule- you are not allowed to criticize your spouse for what they use their money for. If they stay within the agreed upon amount, let them do as they please. This will prevent A LOT of money fights.

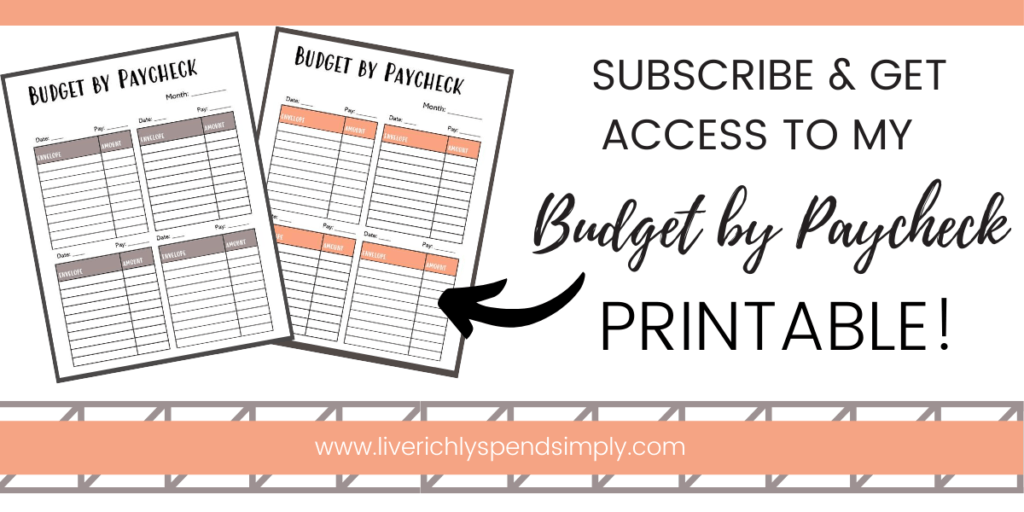

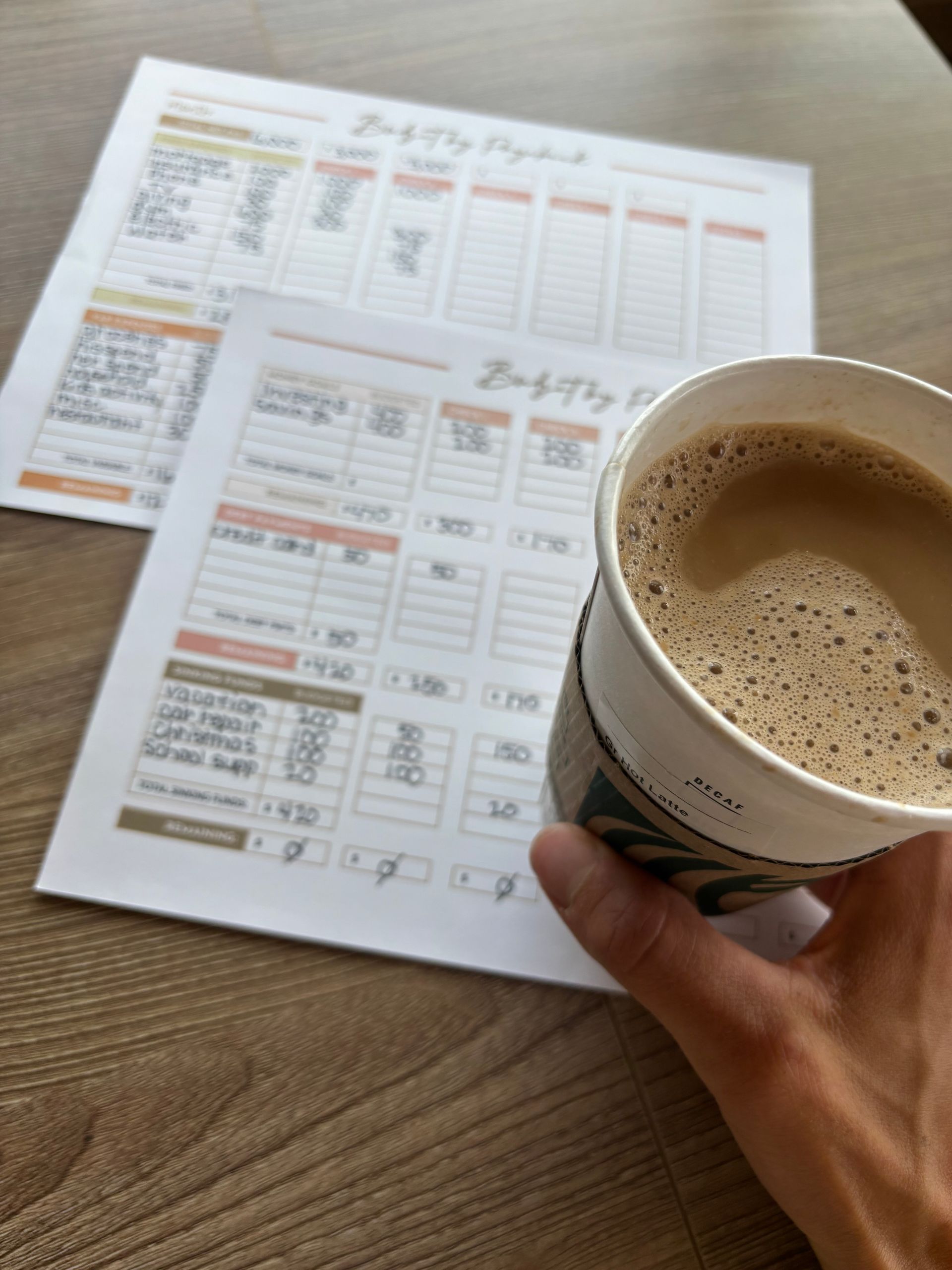

10) Make a budget & bill schedule using the budget by paycheck method.

Often people get hung up on how to align their budget with reality. They make their monthly budget, but when the money comes in and bills come due, they aren’t sure how to reconcile that in their budget.

For example, let’s say a husband and wife are making their budget. Together, they take home $6,000 per month. The wife is paid weekly, on average taking home $500 per week. The husband is paid on the 20 th every month, earning a salary of $4,000.

When they create their budget, they plan spending totaling $6,000. However, since they are cash strapped the first half of the month, they aren’t sure how to decide what budget categories to “fill” first.

There are a few ways to handle this. First, download my free budget by paycheck template to get started.

HOW TO ALLOCATE YOUR SPENDING & INCOME

The first way is to get one month ahead on their bills. This will take some time. To achieve this, anytime the wife earns more than expected (budgeted), or they are under on a budget category, they should apply that money to their “get one month ahead” fund.

Once they save one month's worth of expenses, they should always keep that in their checking account as a buffer.

This way, they are always living on the prior month's income, and it takes the “cash strapped ” feeling away.

The key is to not spend your buffer amount on things that aren’t in the budget. Leave it in your checking account as a true buffer between the first half and second half of the month cash flows.

The second way is to create a bill pay schedule. Let's say a few of the larger expenses aren’t due until the last day of the month or first week of the next month (utilities, rent/mortgage, insurance, etc.). Though the bill might come earlier, it isn't’ due often until a few weeks later.

The couple could decide to pay the larger bills that aren’t due until the first week of the following month with his income on the 20 th . With her income, they completely “fill” the fun money, date night, groceries, etc. budget categories.

In other words, they create a bill pay schedule alongside their budget.

11) Use cash for budget categories you tend to overspend on.

Research shows that when consumers use cash instead of a debit or credit card, they spend less. For budget categories you struggle to stick to, use cash envelopes! Categories that are great for cash envelopes include groceries, fun money, gifts, haircare, etc.

Download and print my free cash envelope templates to get started!

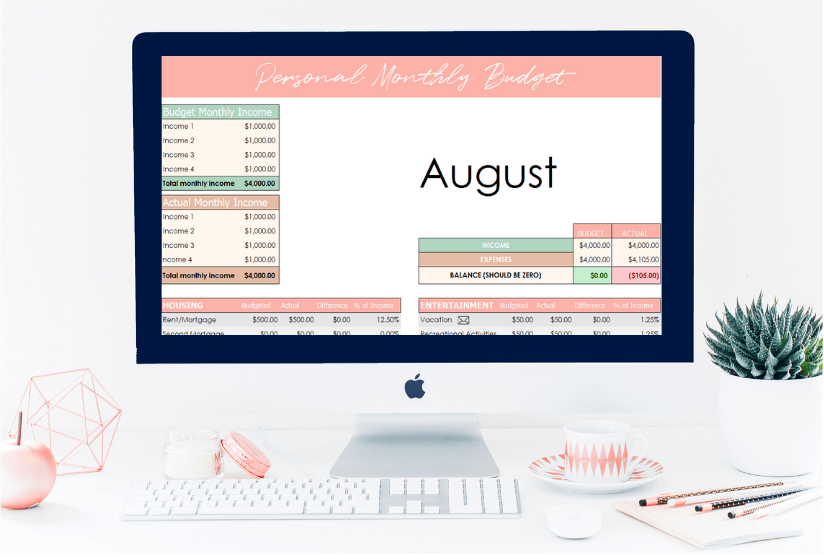

12) Use an excel budget to save time budgeting.

If you’re an excel user, an excel budget is a fantastic way to save time budgeting. Additionally, the formulas make creating a bill pay schedule with a paycheck-by-paycheck budget super quick! I keep our paycheck budget in excel, you can use my exact template too!

13) Download & use Every Dollar app for mobile budgeting.

Dave Ramey’s Every Dollar app is a free budgeting tool you can use to track your spending. Upgrade to Ramsey Plus to connect the app to your bank account. Personally, I create a paycheck budget in excel, and then I use the free app to track my spending.

14) Cut up your credit cards.

Cutting up your credit cards means no more minimum payments to add to the budget! It’s no secret I don’t have warm feelings towards credit cards! In fact, we do not have any credit cards! We’ve found that living a 100% cash-flowed lifestyle keeps things simple and keeps us away from temptation.

SAVING

15) Set aside 3-6 months' worth of expenses in an Emergency fund.

A fully funded emergency fund for financial hardships gives you security. Of course, we know our security and comfort should not be in money. Rather, it should be in God alone. We trust that He will provide, but it is our job to steward wisely what he has given us, including planning for the future.

An emergency fund is 3-6 months of household expenses set aside for emergencies such as a job layoff, major household repair, etc.

The riskier your life is, the closer to 6 months of expenses you should have saved.

16) Save year-round for expenses that catch you off guard.

Do certain expenses always seem to sneak up on you? Christmas? School registration fees? Semi-annual insurance premiums?

When you aren’t prepared, these gotcha expenses always seem to hit at the worst possible time.

Before we were budgeting consistently, it seemed like these expenses came up right after the car broke down, the heater needed to be fixed, and our yearly insurance premium was due.

Here’s how you can start saving for irregular expenses year-round by using sinking funds!

HOW TO USE SINKING FUNDS

- List every irregular/seasonal expense you can think of. Include expenses like school dues, medical needs, annual/semi-annual insurance premiums, home repairs, car repairs, etc.

- Review prior years bank statements to help.

- Determine how much you’ll need & when you’ll need it.

- Calculate how much you need to budget every month.

- Add it to your monthly budget and track your sinking fund balances!

17) Save up and pay cash for large purchases.

Similarly, use sinking funds to save up for large purchases over time. Set realistic, specific, attainable goals. If your vehicle is old and has lots of miles on it, start saving for a new one now. It could take 3-5 years, and that’s okay! The point is to avoid using debt to fund your purchases and cash-flow them instead.

18) Keep savings funds separate from your regular checking.

At a minimum, keep your sinking funds and savings in one separate account from your checking account. This way, you’re not tempted to use the funds for something else. Alternatively, you can set up separate savings accounts for each sinking fund.

19) Pay extra on your mortgage when you can.

Can you imagine what life would be like without a mortgage payment? After your consumer debt is paid off and you’re consistently investing, use any extra cash to pay down your mortgage. You can take years off your mortgage by simply paying a little extra every month. Small amounts add up over time. So, whether it’s $100 or $500 extra per month, make it a habit!

20) Only use your emergency fund on actual emergencies.

When you really want something bad enough you can make anything an emergency .

The toddler spilled juice on the sofa again, so we need a new one.

We have had the same TV since we first got married, we need a bigger one.

While these are inconveniences, they are not emergencies. New furniture or a new TV should be cash-flowed by saving up over time, not using the emergency fund.

An emergency fund is for true emergencies, such as job loss, a large car or house repair needed, and things of that nature.

21) Keep a savings tracker in your planner.

I have a case of major mom-brain, and thus I consult my planner ALL DAY LONG.

I like to keep ALL my personal, financial, and business documents in one place. Every month, I simply print my new budget documents, hole-punch, and stick in my planner.

To keep track of your savings balances and sinking fund balances, get a planner template!

22) If you are going to pay for kids' college, start saving now.

If you plan to put your kids through college, it is a great idea to start saving now! Personally, we will not be paying for our kids' college, for a variety of reasons. However, many parents DO plan to pay for their kids' college, which is an awesome gift to your children! If you are wondering if it is time to start saving, it is. From the second you find out your expecting, it is time to start saving! College is a HUGE expense, I highly recommend consulting a financial advisor to see what college savings plans are available in your state.

INVESTING

23) Invest at least 15% of your gross (before-tax) household income.

To live close to the same lifestyle you do now in retirement, you should be saving at least 15% of your gross (pre-tax) income. To achieve the same lifestyle, you should estimate living off 80% of what you do right now. While this is a good goal, most people want to achieve a higher quality of life in retirement than what they have now. Because of this, investing 15% instead of the widely recommended 10% of income will help you achieve that goal!

24) Automate your investing contributions.

The best way to ensure you hit your retirement savings goals every month is to automate your contributions. By automating your contributions, you hold yourself accountable.

25) Open an IRA in addition to your 401(k).

An IRA (Individual Retirement Account) often has more investing options than an employer-sponsored retirement account, otherwise known as a 401(k). We follow Dave Ramsey’s recommendation to invest up to the employer match in our 401(k), and then invest the remaining amount to get you to 15% in an IRA.

26) Invest in mutual funds instead of single stocks.

Investing in single stocks is playing Russian roulette with your money. A better financial plan is to invest your money into historically high performing mutual funds. By doing this, you’ll see steady, consistent growth over time. Investing in mutual funds allows you to diversify your risk by investing in groups of stocks rather than single stocks.

27) Pay off all your debt BEFORE investing.

When we focus on one thing at a time, we are more effective . Before getting knee deep in investing, pay off all your consumer debt. Making the monthly contribution to your investment account will be a lot easier without any monthly payments draining your income.

We used the debt snowball method to pay off over $20k of student loan debt in 12 months! If you are currently in debt, start your debt snowball and pave the road to financial freedom.

28) Save for large purchases AFTER investing.

Don’t sacrifice your future for what you want today. In other words, learn to delay your gratification. Make sacrifices now, so that you can enjoy your life (and money) later. This means saving up for wants and needs happens with money that is left over after investing. Do not get into the habit of pausing investing to satisfy your material desires. It’s a hard habit to break. Stay the course, practice self-discipline.

29) Do not chase short-term gains or get rich quick schemes.

It sounds cliché, but if i t sounds too good to be true, it is. Warren Buffet puts it this way, if you aren’t willing to own a stock for 10 years, do not even think about owning it for 10 minutes.

30) Use a financial advisor.

Although I know quite a bit about investing, we use a trusted financial advisor to manage our portfolio. He ensures we have dotted all our I’s and crossed all our T’s. What I do not know, he explains. A good financial advisor is a great teacher. Do not invest in anything you do not understand. If your advisor does not take the time to help you understand where your money is going, do not give it to them to manage.

31) Learn about investing. Become self-educated.

Although I was an accounting major in college, most of what I learned about investing came from personal study. I have always been intrigued with personal finance, so I sought out to learn as much as I could. Spend time learning how to manage the money you work so hard to earn. It is not rocket science. Read, read, read. Then read some more.

⭐️ More on investing & retirement:

- What You Need to Know About Retirement Planning

- 7 Things You Should NEVER Do in Times of Financial Hardship

- The Best Investing Tips Millennials Need to Know

- How to Invest When it Feels Like You Have No Money

- The 7 Baby Steps to Stop Living Paycheck to Paycheck

- 10 Habits to Start in Your 20's to Retire a Millionaire

- The 7 Most Important Money Habits You MUST Know

- 7 Things Millionaires Do Differently With Their Money

- 7 Surprising I Wish I Knew Earlier About Money

- 5 Key Life Skills Millennials Need to Learn

- Roth IRA vs Traditional IRA: How to Know What's Best for You

- 5 Retirement Plans for Self Employed That You Probably Didn't Know About

- How to Develop Healthy Money Habits This Year

- Stocks Vs. Mutual Funds

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.