10 Mistakes to Avoid if You Want to Get Out of Debt Fast

melaniedj • 20 January 2019

Do you struggle with paying off debt? Have you found yourself thinking there’s no way we could every pay off that much? Are you sick of starting to pay off debt only to lose motivation weeks later?

There could be some fatal mistakes you’re making while paying off debt, without even realizing it.

You’re sick of monthly payments. It gets old running out of money at the end of the month. The way you’re managing money now isn’t working and hasn’t been working for a while.

Take heart, because I have some awesome tips for you to help you on your debt payoff journey.

We were able to pay off $20k in 12 months while living on one income part of the time and fresh out of college. Believe me when I say if we can do it, anyone can.

I truly believe that getting out of debt is the most important step you can take to building wealth and taking control of our money.

The first step to taking control of your money is to stop borrowing.

Once you decide to stop borrowing money, be aware of these common mistakes people tend to make on their debt payoff journey.

These are what I have found to be the most detrimental to your debt payoff journey.

If you find yourself doing any of the things below. STOP. Don't try and justify it. Take it from someone who has paid off over $20k- if you do these things it will make it REALLY difficult to pay off your debt quickly.

Mistakes to Avoid While Getting Out of Debt

NO EMERGENCY FUND

Before beginning to pay off debt, you should have an adequate emergency fund.

This way, if an unexpected expense comes up, you have the ability to pay for it, rebuild your emergency fund, and then continue with your debt snowball.

The issue is many people act dumbfounded when an unexpected expense comes up. Your car broke down? The dishwasher quit working? You’re having a baby and have a large hospital bill?

I hate to be the one to tell you but… these things WILL happen for the rest of your life. Instead of acting surprised when they happen, prepare for them so that they don’t cause financial stress.

Don’t victimize yourself by saying “I can’t believe ______ happened!” These experiences happen to everyone. They will happen to you. Be prepared!

NOT CUTTING EXPENSES

You can’t get out of debt while trying to keep the same lifestyle that got you there.

A lot of people want to get out of debt, not a lot of people are willing to make the necessary sacrifices to do so.

If you are trying to pay off debt, your biggest tool is your income. If you can find a way to free up your income and throw extra money at your debt every month, you will succeed.

That is the key- learning to live WELL below your means so that you can have extra money to throw at your debt every month.

This requires scaling back on gifts, outings with the family, eating out, and other entertainment. You’re going to have to be a cheap date for a while.

Some small expenses may not seem like much and thus not worth cutting out, but small expenses add up over time!

Eating out for lunch everyday might not seem like a big deal, because maybe it only cost you $5-$10 per meal. If you add up $5 over the course of a year, you’ll have spent $1,300 alone on eating out for lunch everyday.

The meal plan service I use costs $5 per meal for a whole family, and I usually have leftovers!

Keep in mind small progress is still progress.

Related Content:

LIVING WITHOUT A BUDGET

If you don’t tell your money where to go every month, eventually it will tell you.

What is more stressful than running out of money every month?

When you don’t track your spending, you are setting yourself up for financial stress and money fights if you are married.

Living on a budget allows you to have piece of mind that if you stick to your plan, you will not run out of money at the end of the month.

In fact, with budgeting, you will be a month AHEAD of your expenses.

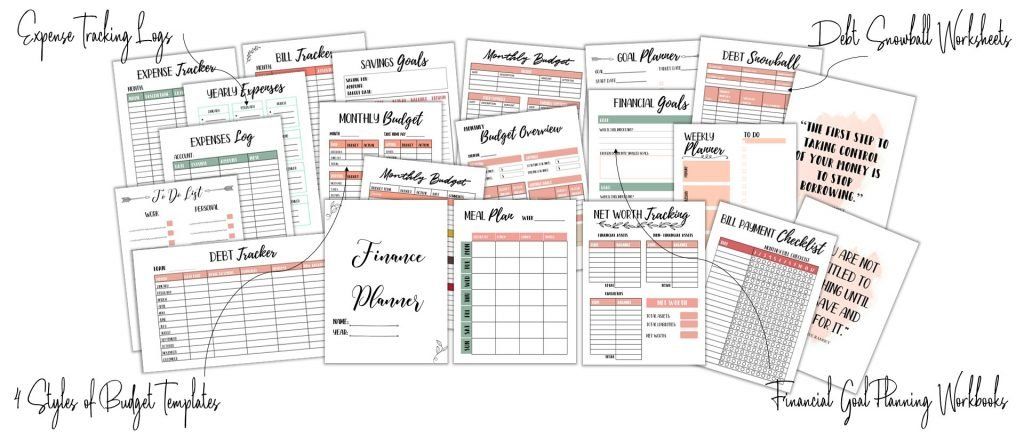

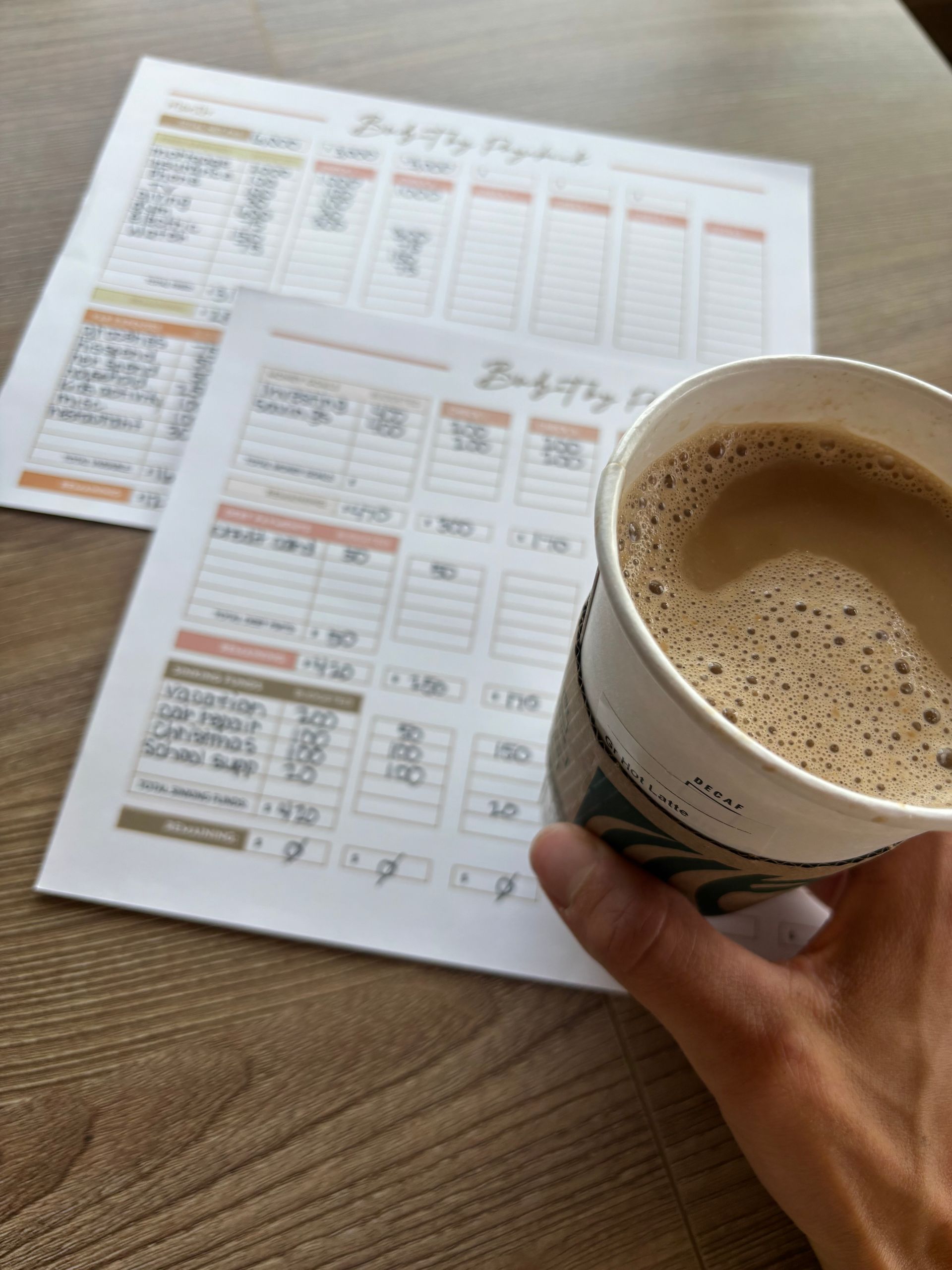

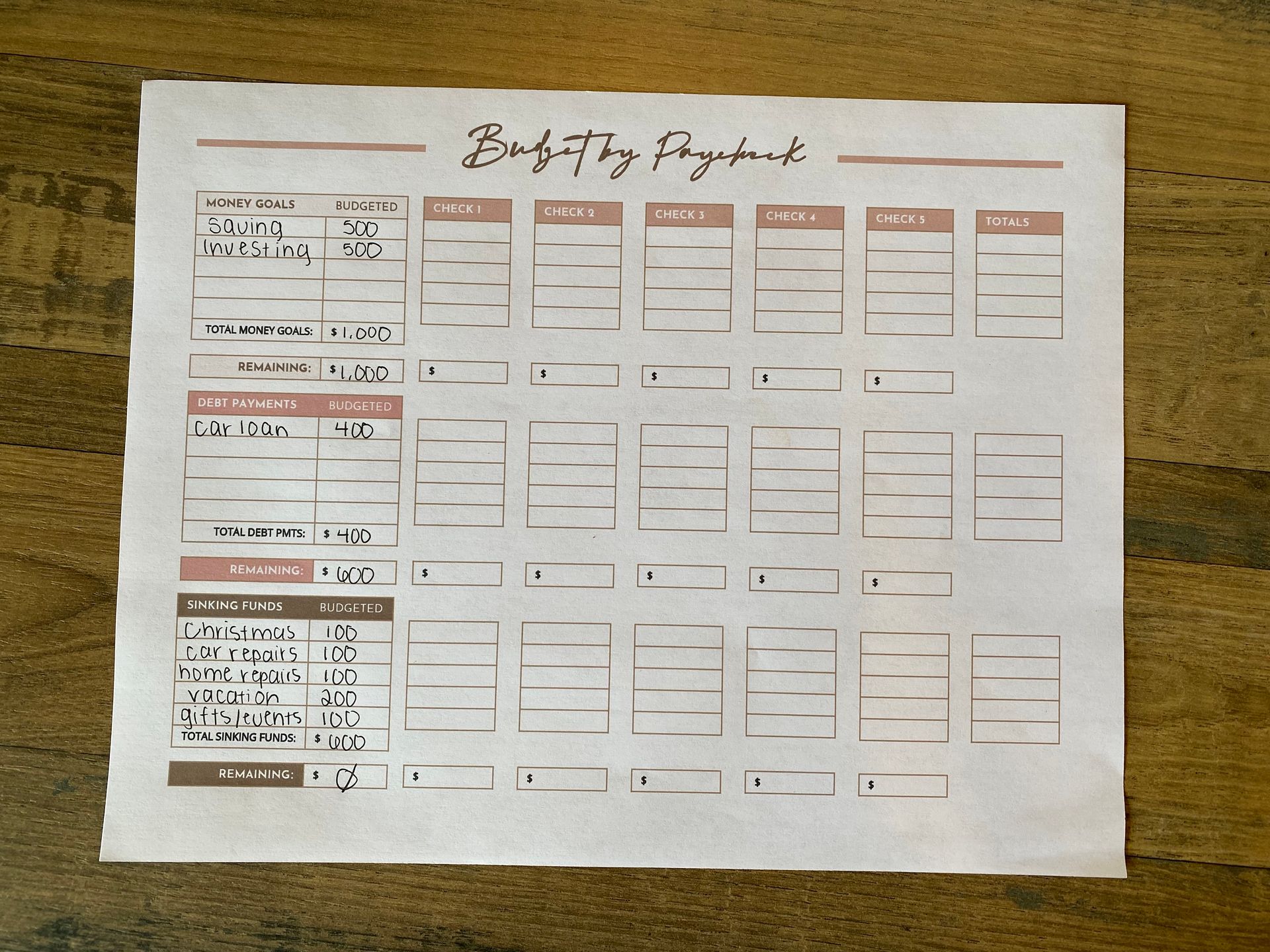

If you want to get on a budget but either don’t know where to start or you feel like you don’t have enough time to put it together, my budget bundle and household financial planning guide will relieve that burden.

I created this in hopes that it will inspire you, motivate you, but most importantly help you reach financial peace.

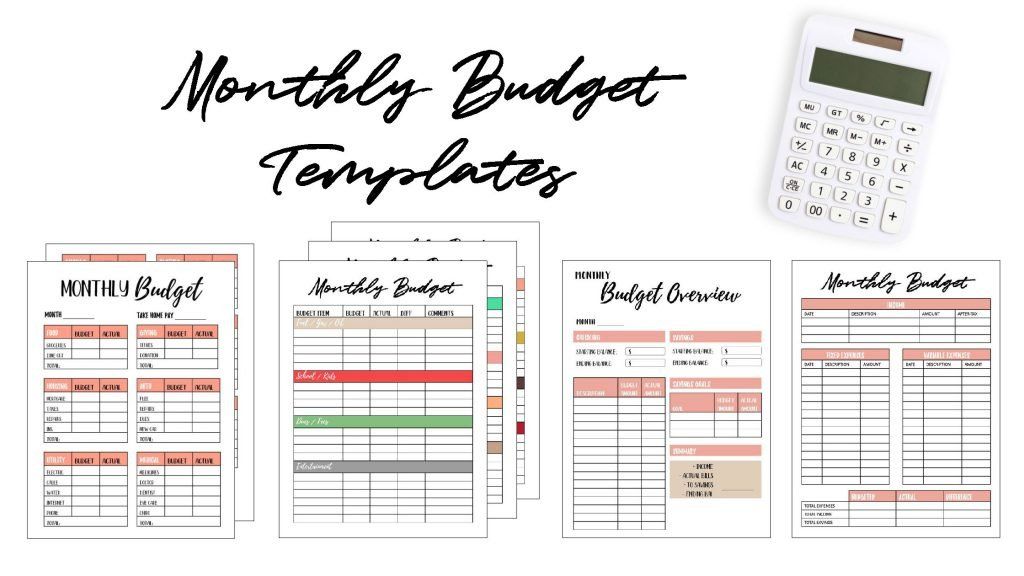

The budget bundle includes four different styles of monthly budget templates!

There is also 45+ pages of personal finance resources... learn more about it here!

Remember, your life is the sum total of ALL the decisions you make- big and small.

Living on a budget is one small decision and step in the right direction you can take to one day reach financial freedom.

Related Content:

CONTINUING TO USE CREDIT CARDS

Cut up your damn credit cards. I don’t care if you pay them off every month. I don’t care how many freaking “points” or air miles you earn per purchase.

The truth is there is no such thing as credit card rewards.

Do you REALLY think that an industry that has some of the top marketing and research teams in the country and invests MILLIONS of dollars into researching consumer behavior is actually GIVING you something for free?

C’mon. I know you’re smarter than that.

Let me clear up some common myths about credit cards and equip you with some truths.

CREDIT CARD MYTHS

MYTH: A credit card is great for an emergency.

TRUTH: Saving your freaking money is great for an emergency. Before you know it Christmas will be an emergency, your date night dinner will be an emergency, the kids school clothes will become an emergency.

MYTH: Credit cards are necessary to build my credit score. It shows I’m responsible and mature with money.

TRUTH: All a credit score does indicates is how much you’ve interacted with debt. You can buy a house, car, and rent an apartment without a credit score.

MYTH: Credit cards are more convenient.

TRUTH: Why, because the money doesn’t come out of your checking account right away? So they’re convenient because you can’t afford whatever you’re buying in the first place?

MYTH: You can’t do certain things without a credit card, like stay at a hotel, rent a car, and travel.

TRUTH: My husband and I have done all the things mentioned above and we don’t have any credit cards. You know what works really great in the place of a credit card? DEBIT CARDS.

The number one thing most people struggle with while getting out of debt is getting rid of their credit cards.

It is scary and problematic that credit cards have been so heavily marketed to us that we literally believe that we can’t survive without them. They’re our security blanket.

Once you break up with your credit cards, you will see your finances in a completely different light.

You’ll pay more attention, spend less, and care more.

Related Content:

TAKING ON MORE DEBT

This should go without saying, but if you are paying off debt, do NOT get into more debt.

I understand there is temptation everywhere to go into debt.

If you follow the typical path that most Americans do, it will consist of going to school for four to six years, accumulating tens of thousands (or even hundreds) of student loan debt, buying yourself a graduation present which includes a car on payments, maxing out your credit cards while just getting on your feet, and hoping by some act of God you are able to pay it all off one day.

Not to mention going through life without any real financial plan.

There is a reason the Bible warns against debt - "the rich rule over the poor, and the borrower is slave to the lender" Proverbs 22:7.

When you take on debt, you become a slave to the lender. It's a vicious cycle.

Y ou take on more debt, you have to work more to pay off that debt, you become increasingly unhappy because you're burnt out from the cycle, your marriage suffers, your relationship suffers, etc.

Don't fall for it. Break the cycle. Leave a legacy!

PAYING OFF IN NO PARTICULAR ORDER

Paying off your debts from smallest to largest is the most effective. Momentum is key.

Most people think that the best way to pay off debt in the order of largest to smallest, or from highest interest rate to lowest interest rate.

The reason I recommend paying off debt from smallest to largest is because it helps you gain momentum. When someone decides to pay off debt, they usually start off with a bang. However, a few weeks in, it can be easy to become discouraged because that hill you had to climb now seems like a mountain.

When you start with the smallest debt you are more likely to stay motivated.

I suggest using a debt snowball worksheet and pinning it somewhere you see it often, this will help you stay motivated!

The worksheets pictured above come with the Ultimate Budget Bundle.

To be effective, you must have a plan.

NOT THROWING ALL EXTRA MONEY AT YOUR DEBT

I call these the “ish” people. They are serious about paying off debt…. Ish. If you want to get rid of your debt you need to quit with the damn ish.

Paying off debt “ish” will get you absolutely nowhere. If you half ass it, you will get half ass results.

The problem is there are many people who will try to tell you to take it easy, cool down on the whole debt payoff thing, and just enjoy life.

Yes, I can 100% get on board with the just enjoy life part- but no the take it easy part. There is a time and place for taking it easy, and in the midst of paying off debt is not the time.

You know what will be really enjoyable?

When you are able to pay off your debt 10 years earlier than the estimated payoff date!

Any extra money you have during the debt payoff process should be thrown at it. We threw Christmas money, birthday money, bonuses, you name it, we threw it at our debt.

Related Content:

SAYING YES TO THINGS YOU SHOULDN’T

In pursuing any goal, what is most important is not what you are willing to do, but what you are willing to give up.

The same goes for getting out of debt. What are you willing to give up? If you really want to pay off debt fast, you have to be willing to give up A LOT.

If you can delay your gratification and pleasure for a greater result, then you are financially mature.

NOT KEEPING TRACK

Your debt payoff goals must be specific and measurable otherwise they are just dreams.

Set realistic but challenging goals for yourself. Set weekly, monthly, and yearly goals.

When we were paying off my student loans, I would keep a visual on our fridge and every time we would make a big payment, I would fill it in to show our progress. I’m a visual person, so this worked really well. I loved to look and see our progress!

LISTENING TO OTHERS

DO NOT take advice from people who don’t have a plan.

If your broke friends are making fun of you, you’re doing something right.

Whenever finances are discussed, it seems to be prime real estate for others to insert their opinions/objections/thoughts about your financial decisions into the conversation.

Most of the time, people will say certain things to make themselves feel more secure about their financial decisions. They’ll defend credit cards. You’ll probably be told that car payments are justified because its an investment.

If you want to become financially free, emulate rich people habits. Conversely, if you want to stay broke, develop broke people habits.

Stop listening to your broke friends trying to justify their own dumb money decisions.

KEY TAKEAWAY

If you struggle on your debt payoff journey, that is OKAY. We all have. It is NORMAL. I promise you will have times where you feel discouraged, defeated, and just want to give up.

My one word of advice is... don't! Do not quit on yourself. See it through.

If you don't quit and persevere, some day you will have a great debt payoff story to tell!

Keep these mistakes in mind on your journey to debt freedom.

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.