How to Attack Your Student Loan Debt in College

melaniedj • 3 February 2019

For some of you, your student loan debt will be the longest relationship you'll ever be in.

Most of us don't ever look at our student loan balance, we just gladly take the money and sign on the dotted line every year.

We don't even know what we are being charged for. I can guarantee if you look at that bill you'll see $3,867 to walk on the sidewalk, $4,000 a day to be fed, $6,893 to breathe air.

Ok, kidding..... kind of.

Today, over 70% of college graduates will leave with student loan debt. In fact, according to a recent study, nearly 1 in 4 Americans are paying off student loan debt.

On average, a student leaves the university with $37,172 in student loan debt.

The shortest option you are given for a payoff schedule is 10 years.

This means if you graduate with $37,172 of student loan debt, and your interest rate is 4%, your monthly payment to pay off your debt in 10 years will be $376 per month, and you will pay approximately $8k in interest.

What could you do with an extra $376 per month? I can help you out.

If you contribute $376 per month to a good growth mutual fund from age 25 to age 50, with a return of 12% (historical average for S&P 500 over 30 years), you would have $657,666.

Dangggg hope that education was worth it.

Here are the things I did differently than most to set myself up to pay off my student loan debt soon after graduation!

WORK AS MUCH AS YOU CAN

Yes, you should enjoy college, but you shouldn’t let college make you lazy. Get a part time job and always work summers.

Especially in private universities, not a large percentage of the student body holds a job, and many students will give a long list of reasons why.

This does not prepare you for real life.

In real life, you will have a million different things to juggle that require your best effort in addition to maintaining a full time job.

The idea of only focusing on your education and not having any other distractions (a job) is completely counter-productive and as far from reality as you can get.

I worked two jobs while in college, one early in the morning, and then one after school and on weekends. I worked extremely long days every summer too.

If you work while in school, you won’t need to live off of student loan money, and you will be able to start paying down your debt BEFORE you even graduate.

You CAN work while in school, and contrary to popular belief among parents, working while being required to get good grades will actually HELP you when you graduate.

Do odd jobs, clean houses, start a blog!

START PAYING NOW

Throw any extra money that you can at your student loans before you graduate, because all this money will go to principal rather than interest.

I understand that most students need the money they make from any part time job to cover living expenses while in school, but if at all possible, find a way to start paying on your loans now.

I waited until my last semester to start paying on my student loans, but I wish I would've started a lot earlier.

Time is money.

PAY AS MUCH AS YOU CAN EVERY SEMESTER

If you are able, pay more than what is required of you to pay out of pocket at semester.

This way, you can reduce the amount of debt you have when you graduate.

Many times we take a sigh of relief when our required amount to pay out of pocket isn't as much, but that just means that you'll have a bigger debt load when you graduate.

I tried to pay more than my required amount every semester, thus reducing the amount of financial aid I needed.

This is why working during the summer and maintaining a part time job while you are in school is key.

PAY DURING THE GRACE PERIOD

When you graduate, don’t wait until you get your letter notifying you that your loans are due to start paying.

Immediately after graduation, your student loans will enter what is called a grace period. Basically, this is a period of grace where your loans are deferred in order to give you time to find a job.

Most college graduates that I know have a job secured before graduation.

If you are in this boat, then start paying on your loans immediately.

This too will allow you to pay principal rather than interest, which will reduce the amount of interest you pay in total.

PUT A PLAN OF ACTION TOGETHER

A goal without a plan is just a wish.

Before you graduate, set up a plan of attack, using the following questions as your guide-

- How much extra money do you think you’ll be able to throw at your loans a month?

- How long do you estimate it will take you to pay them off if you only make minimum payments?

- When would you (realistically) like to have them paid off? Two years? Five years?

- Sort your loans from smallest to largest. This is the order I recommend paying them off in.

If you can answer the questions above and formulate a plan of attack, you will be wayyyyy ahead of everyone else.

It is important that you DECIDE before graduating that you will not let your debt follow you your entire life.

Take responsibility, then work your ass off to get rid of it as soon as possible.

Related Content:

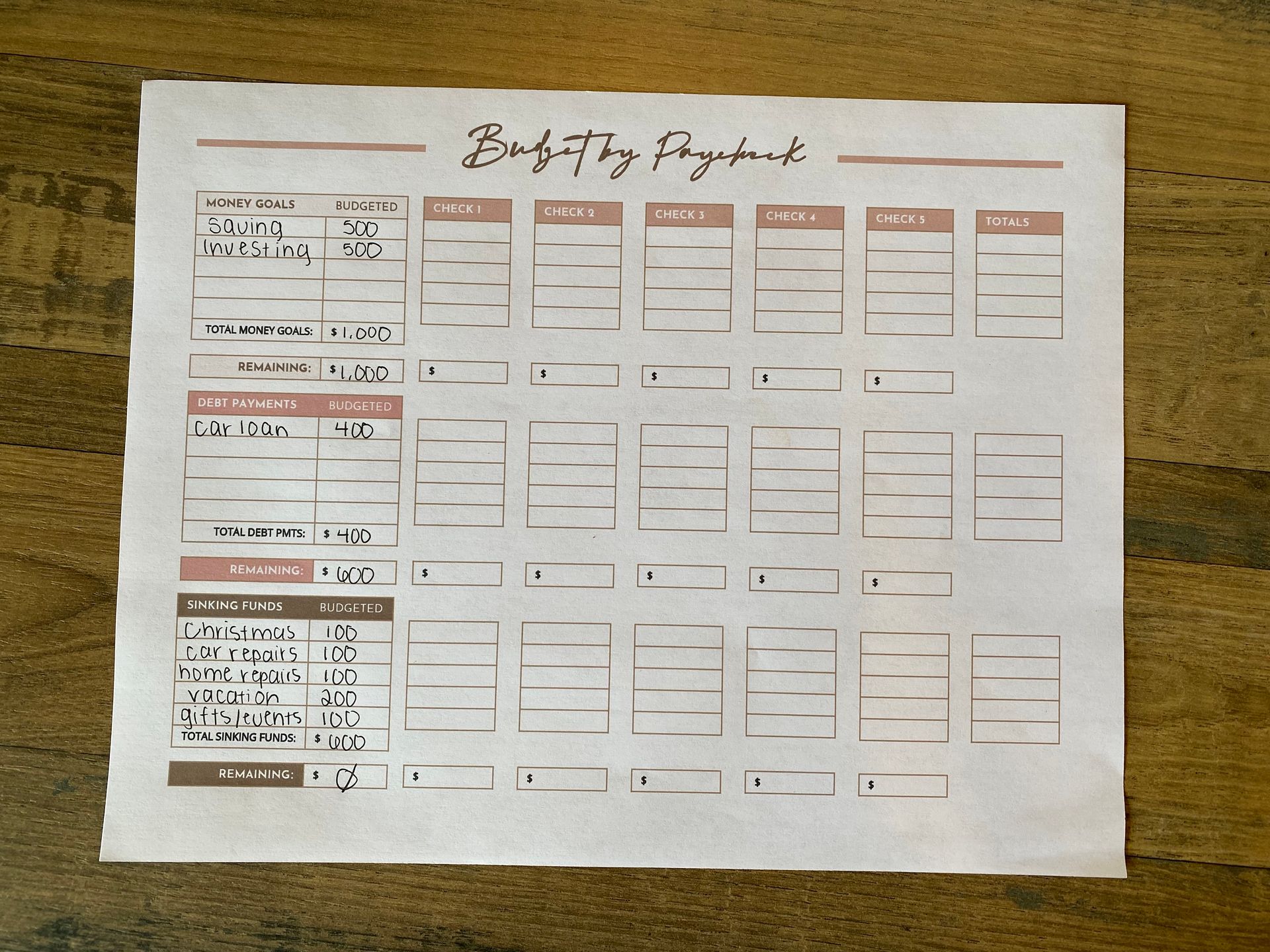

GET ON A BUDGET

If you get on a budget before graduation, you will be leaps and bounds ahead of your peers after graduation.

Especially if you can’t actually make payments on your loans while in school, if you can at least set up a budget that you can follow after graduation you will be on the right track!

A budget honestly changed our financial course.

When I graduated and got married soon after, we kept a budget, but we were not consistent and didn’t track it well.

After we decided to get on a budget, we realized that what we thought we were spending vs what we were actually spending were completely different spectrums!

When it comes to budgeting, ignorance is most definitely not bliss.

Get on a budget; you’ll thank yourself later.

I will help you set up a budget, learn how to track your budget, and beat budgeting bloopers!

DON’T TAKE OUT LOANS FOR ANYTHING BESIDES TUITION

First of all, if you are reading this BEFORE going to school, don’t take out loans, period. Choose a less expensive school.

However, if you are finding yourself in my shoes just a few short years ago, about to graduate with a mound of debt, then listen up.

In some cases, you are able to use your student loan proceeds to live off of, avoid this at all costs!

I didn’t have this option available to me, but I know this is available for some.

Do not go into debt to pay rent, buy food, or go out to the bars with friends.

At the time it doesn’t seem like that big of a deal, but that’s because that is the danger of debt. You don’t have to pay for it now, so it’s out of sight and out of mind.

Related Content:

TIME IS MONEY

Just remember, time is money.

The longer you wait to start attacking your student loan debt, the longer it will take to pay off, and the less motivated you will become.

As time passes, many seem to think of their student loan debt as a fact of life, and they don't see any way out, and thus they allow it to stick with them their entire life.

I'm here to tell you it is NOT just a "fact of life" and if you decide to let it stick around, it will hinder your ability to build wealth.

Get mad at your debt, and if you are in college, the time to start is NOW.

START YOUR DEBT SNOWBALL

- The exact printable worksheet we used to pay off over $20k of student loan debt in 12 months

- Editable & fillable PDF printable worksheet - type directly into PDF

- Visualize your progress and stay motivated on your debt free journey

Share this post!

Learn how we budget on one income as a family of 6 using the paycheck budget method. See our simple system, categories, routine, and free budget template.

Building a house and homeschooling 4 kids? Here is how we afford a semi-organic, real-food diet on one income without burning out. Budget & grocery list included!

Learn how to budget biweekly paychecks on one income with a simple system that helps overwhelmed moms manage two paychecks a month with confidence.

Struggling to make one income stretch? This step-by-step paycheck budget method helps families stop living paycheck to paycheck and finally feel in control.

These budget notebook ideas will inspire your creativity and help you organize and reach your financial goals! Here's what you need in your budget binder to take control of your personal finances.

Organize your personal finances by utilizing a budget calendar- lay out your paychecks, bills, social events, etc., so you know exactly what you need to budget for in the month ahead!

Whether you have credit card debt, student loans, a car loan, or mortgage debt, use these debt free coloring pages as your debt payoff tracker; keeping you focused and motivated to become debt free!

The ultimate guide to creating a successful family budget. If you're sick of financial stress and feeling squeezed at the end of every month, start budget planning and taking control of your personal finances.